Arthashastra 2.0 | Chronicles of a Modern India

Arthashastra 2.0 | Chronicles of a Modern India

Series-I : The India Stack , Part - I : A Series on the Developments in the India's Financial Services

There was a very interesting video of our External Affairs Minister, Mr. Jaishankar, that had gone viral on the internet recently. He exclaimed - how when it came to the Vaccine Certificate, India has gone digital, and a developed nation like the US is still relying on a piece of paper. India has taken a giant leap when it comes to adopting technology, and Indian Fintech is at the heart of it.

India’s Fintech Ecosystem has developed at such a rapid pace that it carrying the momentum to transform our economy. It is built on the robust, state-of-the-art digital infrastructure, cutely called - the India Stack. Built upon the biometric-enabled Aadhar system, India Stack is the wormhole pushing India towards the digital ecosystem of financial inclusion and innovation.

Backed by government initiatives and support, today, India Stack serves the people of India right from identity to payments to banking and various other services. India’s Financial Services have enabled cashless transactions via the UPI infrastructure, while e-KYC and digital signatures have made loan approvals almost instantaneous and paperless.

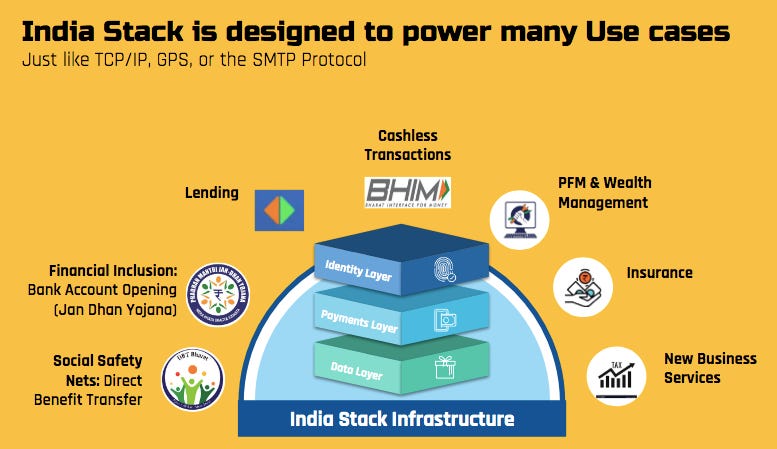

The India Stack

Source: TWUnroll

The government continues to revolutionalize the fintech ecosystem through the introduction of government-supported schemes like:

Aadhaar e-KYC, E-Sign

NPCI’s UPI Payment

IMPS- Immediate Payment Service(IMPS) is an instant e-fund transfer interbank via mobiles.

AEPS- Aadhar Enable Payment service

Jan-Dhan- Pradhan Mantri Jandhan Yojna(PMJY) is a national scheme launched by the government of India to provide easy access to financial services.

TReDS- Trade Receivables Discounting System (TReDS) is a scheme for setting up and operating the institutional mechanism for facilitating the financing of trade receivables of MSMEs from corporate and other buyers, including Government Departments and PSUs, through multiple financiers.

Government e-Marketplace- GeM is a one-stop portal that facilitates online procurement of goods and services required by government departments, PSUs etc.

Psbloansin59minutes- Public sector bank loans in 50 minutes is a new-age digital lending platform.

Lending enablement framework (OCEN in progress)- Open Credit Enablement Network(OCEN) is a framework of APIs (Application Programming Interface) for communication between lenders, loan service providers and accounts aggregators.

In this newsletter, we will be discussing a few of the key developments that have been happening in the Indian Fintech Space, which is currently the third largest fintech ecosystem in the world.

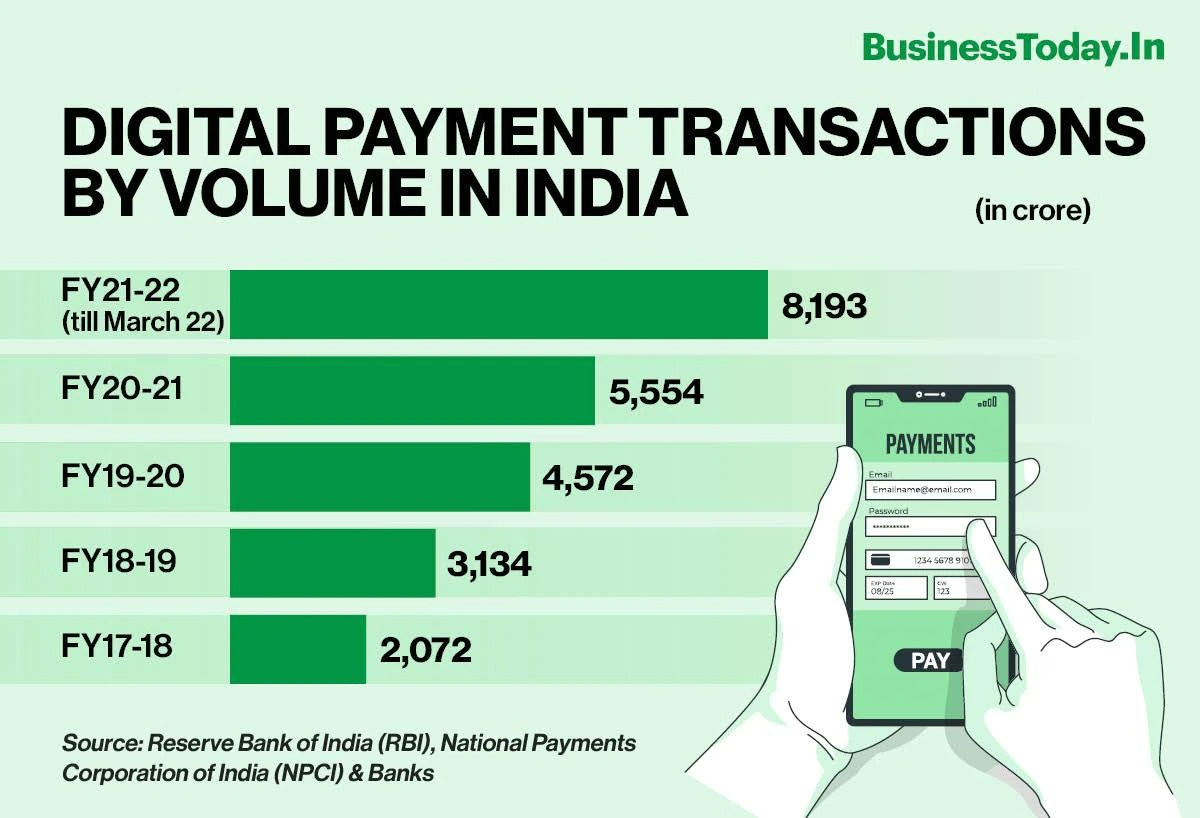

The era of Fintech in India started in 2016 at the time of the demonetization of the currency notes. Initially, a majority of people were reluctant to use digital modes of payments and other transactions. However, gradually they felt that digital transactions provide convenience, safety, and flexibility. And the pandemic has only accelerated the revolution that is the Unified Payment Interface (UPI).

UPI - The Story of India’s Financial Revolution

Source: Razorpay

UPI is managed and developed by the National payments corporation of India NPCI. It allows individuals to run their bank accounts through a single application (such as Google Pay, Paytm, and Bharat pay) and carry out transactions with other banks. It has around 600 million users in India against 300 million households. This means that, on average, there are nearly two users of UPI in each household and has had a 100% compounded growth rate over the last five years.

Some of the features of UPI that each one of us at some point might have experienced are:

Immediate money transfer through mobile anytime.

QR code facility

Avoiding cash on delivery hassle, running to ATM or bank for money

Merchant payment with the help of a single application

Can run multiples bank accounts through a single application

Easily solve the queries and complaints

Big tech companies like Google, Amazon, and Whatsapp now put their hat in the mix as well in the payments solution provider in India through Wallet and UPI.

Moving on is the rapid growth of API banking in India. It has changed the ways in which banks and other fintech operate. The recent developments in API Banking have the potential to revolutionise our country's traditional banking services.

But first, What are APIs?

Source: Appinventiv

Imagine you are at a restaurant. There’s a Menu, there’s a Kitchen, and then there’s a waiter who acts like a like between you and the chef. The waiter passes on your order to the Chef, who prepares it and then delivers it to you on the table. In the exact same way, API performs the role between two applications or entities on the internet.

And technically speaking, a software intermediary that allows two applications to talk to each other.

API or Open Banking

Source: Tekedia

Interestingly, the Indian banks have been adopting APIs aggressively in the last 5 years. Application Programming Interface(API) Banking uses APIs for communication between bank and client servers, making data transfers and secure integration between the customer’s bank and the bank’s system. This has ensured a seamless experience for the financial service providers.

API or Open Banking in India started with Yes Bank and RBL Bank in 2017. All other banks like ICICI Bank, Axis Bank, Kotak Bank, and Smaller Players like SBM, AU SFB, and Equitas SFB have now established comprehensive API banking platforms.

We have also aggressively seen multiple startups in Ed-Tech, Agri-Tech, e-Commerce, and mobility focusing on embedded finance. Embedded Finance, or EmFi, is a concept that typically allows non-financial entities to integrate financial services/ products into their own platform through the use of APIs.

Many players like Ola, Udaan and Stellapps have already established the business model and are working with Banks and NBFCs to scale the business. This is helping startups improve user experience, gain access to customer data, provide value to customers, and simultaneously increase their revenues.

APIs have acted as banks’, Small & Medium Enterprises’ and Start-Ups’ gateway to digital transformation. With the help of this technology, these entities can easily gain customer insights and provide an abundance of services and value propositions to their customers.

As India is revelling in the digitalization era, its population is slowly getting enamoured with the idea of digital banking.

The Emergence of NeoBanks

Source: India TV News

A Neobank is a digital bank that only provides online services. In broad terms, a Neobank is a digitally expanded financial services firm that does not have any physical branches and instead operates online. They generally provide online services like payments, debit cards, money transfers, lending etc.

While traditional banks continue to tackle bringing their legacy-based infrastructure into the digital era, Neobanks leverage their modern digital platforms to analyze customer data and make data-driven decisions.

There are several Neobanks in India which have started to make their presence felt, such as NiyoX, Jupiter, and Fi. They have started acquiring customers at a decent pace and are likely to grow faster than most banks in India. Retail Neobanks will move from primarily ‘Youth and Mass focused’ to more differentiated segments.

A Neo bank provides an experience fitting the best of both worlds—a conventional bank's trust and security while at the same time a fintech’s agility, creativity, and seamless user experience.

“Banking is necessary, but banks are not,” said Bill Gates way back in 1994. Are we about to witness this in the years to come?

Well, folks. Never bet against India!

Conclusion:

India, with the help of its tech-driven ecosystem, has managed to succeed in building an inclusive digital economy from the bottom up. Synergies across public-private institutions have contributed to fostering a vibrant financial services sector in India.

The India Stack is a vast ecosystem that provides a level playing for the existing and new fintech companies, big and small tech firms, to compete while being mindful of having necessary regulations in place. This has ensured that stability and public trust remain paramount.

India's banking, wealth management, insurance, and other financial products are in the middle of a technological revolution. In this series on Arthashastra 2.0, we will tell you about the major developments in the financial space in India.

On the back of RBI floating a discussion paper asking for suggestions for charges on digital payment modes, there had recently been a huge buzz around. What was it all about? What’s next for UPI? All of this will be covered in the next edition of the current Arthashastra 2.0 series.