Concentration | Diversification | Portfolio Management

In the tussle of return expectations and risk management, how much do you think about concentration and diversification in your equity portfolio?

If Christopher Nolan is my favourite Hollywood filmmaker, Vishal Bharadwaj is my favourite Bollywood filmmaker.

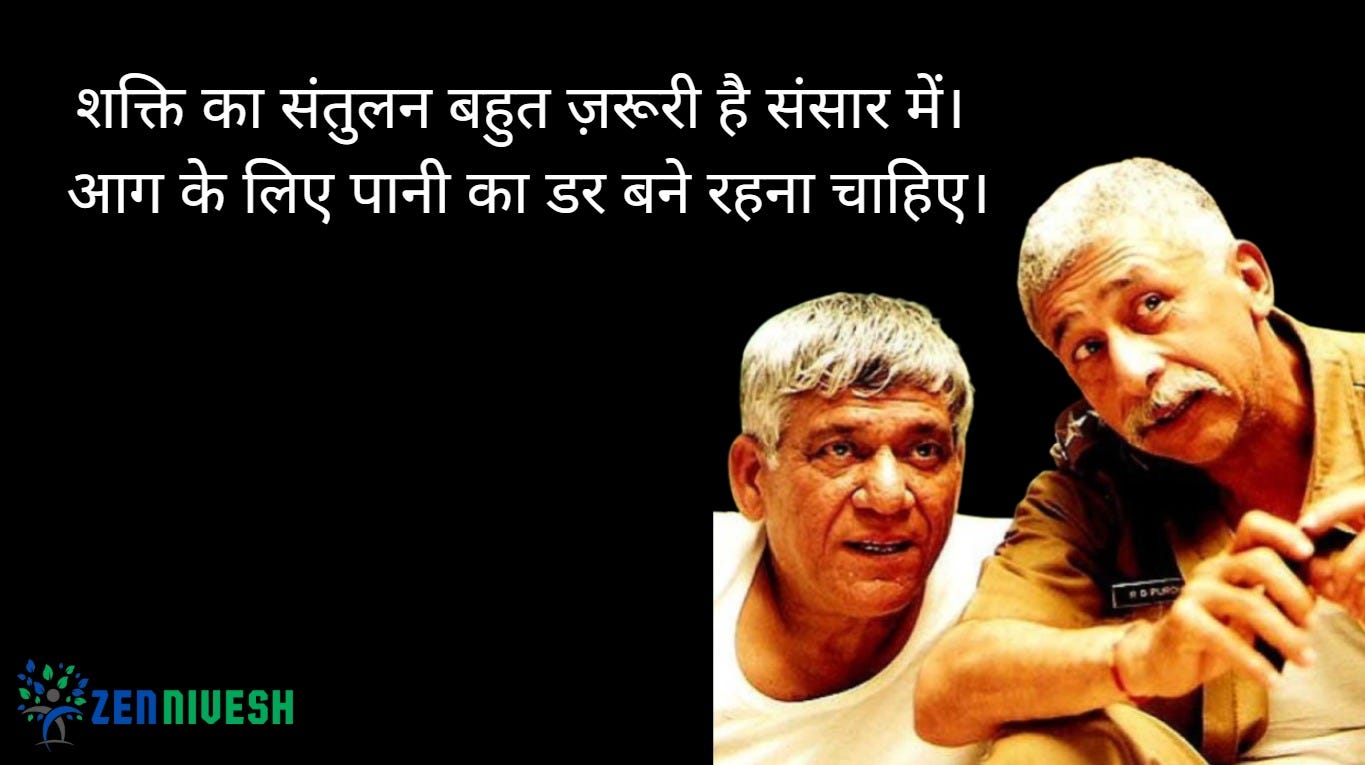

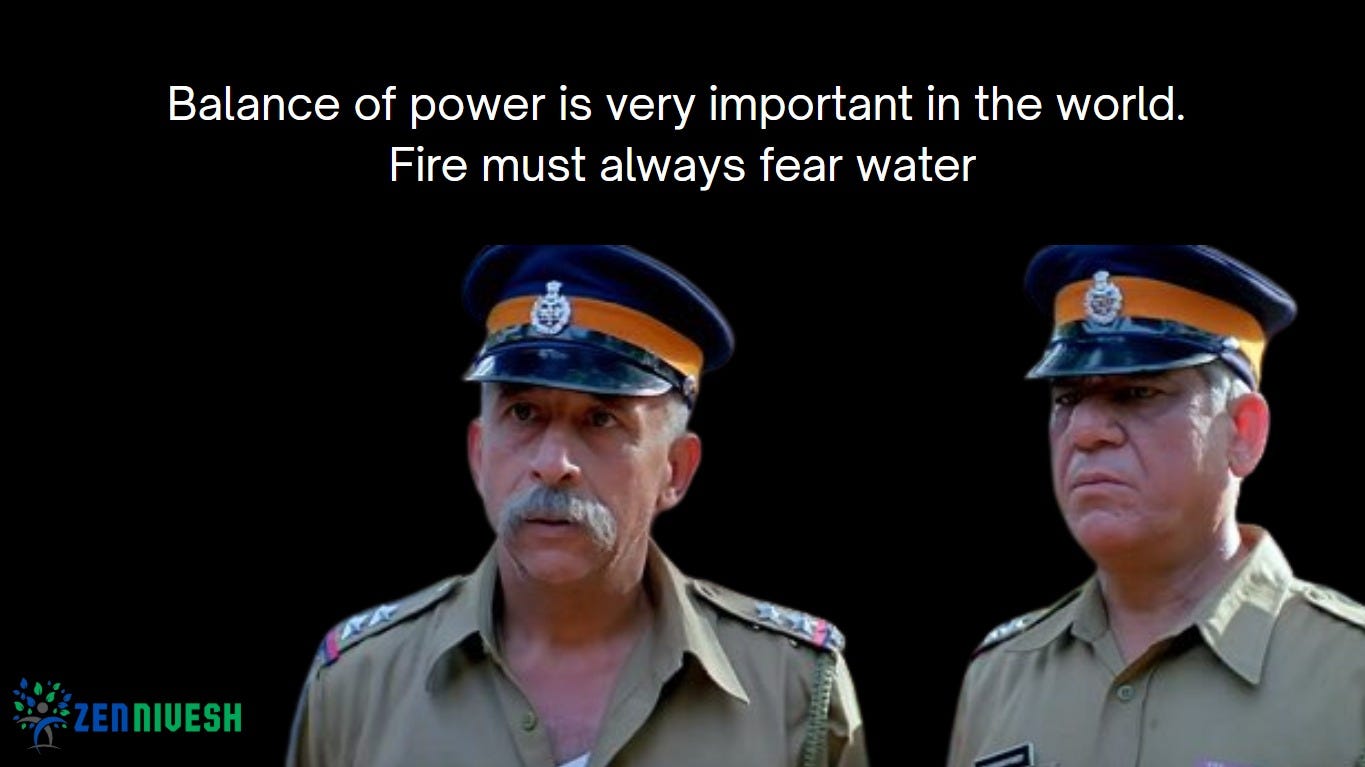

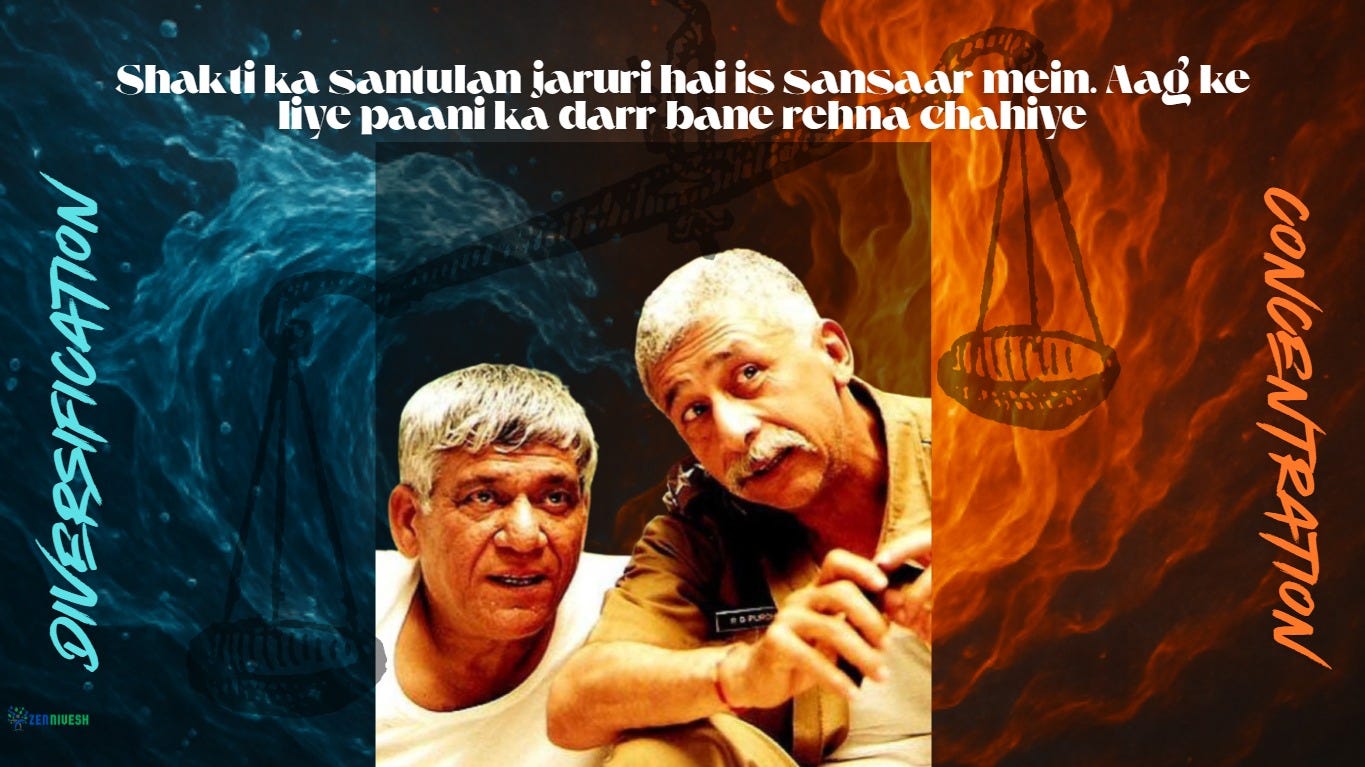

Check this out from his 2003 movie, Maqbool (based on Shakespeare’s classic, Macbeth).

This is one of my all-time favourite quotes from his movies. OK, if you don’t understand Hindi, let me translate it for you.

Now, you might be wondering how this quote or scene from the movie is relevant to portfolio allocation strategies in the stock market.

Just bear with me for the next three to four minutes. And you will get the drift if you haven’t yet. 🙂

Investors often look at the survivors or the outliers and wrongly believe it to be easily replicable.

Let me give you two examples.

Raj, who has always maintained a 4-stock portfolio, has grown his equity investments at 25% CAGR over 20 years.

Rahul, with a 100+ stocks in his portfolio, has compounded his capital at 25% CAGR over 20 years.

One is a super-concentrated investor. The other is a super diversified investor. However, the performance of both is exceptional over the long term. Any investor who has a liking for a concentrated portfolio will get inspired by Raj and will believe that he will be able to replicate Raj’s success. On the contrary, proponents of wide diversification will get inspired by Rahul. They would also believe in replicating Rahul’s success.

However, what both gangs do not pay attention to is the average outperformance of many investors following the same strategy over long periods. They just look at the winners or the survivors.

The cold, hard fact in this tussle between concentrated and diversified is this:

Having a super concentrated portfolio exposes you to the risk of ruin.

Having a super diversified portfolio exposes you to the risk of subpar returns.

I am not going to advocate for which one is better for you. Each one of us is different. So, I won’t make that mistake of prescribing you the best strategy. My best and your best can be poles apart and yet be right for both of us individually. However, I will share a few things from two very good investment books that may help you with the right reasons.

First up is this.

Mr. Pulak Prasad, in his book, “What I Learned About Investing from Darwin”, emphasizes the importance of minimizing errors of commission, investing in poor-quality companies, even if it means accepting more errors of omission, such as missing out on potentially profitable opportunities.

Errors of Commission and Omission

Error of Commission (Type I Error): Occurs when an investor makes a bad investment, mistakenly believing it to be good.

Error of Omission (Type II Error): Happens when an investor overlooks a good investment, erroneously thinking it's bad.

Prasad argues that these two types of errors are inversely related; reducing one often increases the other. He advocates for prioritizing the minimization of Type I errors, even at the expense of committing more Type II errors.

As an investor, it is your job to find out what kinds of errors you can live with. And then invest based on that. You cannot have the cake and eat it too.

So, either you become a concentrated investor and miss out on the advantages of diversification, or become a diversified investor and miss out on the advantages of concentration in the portfolio.

Another investment classic has a few pages dedicated to the same topic of concentration vs diversification.

In this book, Philip Fisher explains how the right strategy of diversification can become a wrong strategy if taken too far.

He writes and I quote:

“Usually, a very long list of securities is not a sign of the brilliant investor, but of one who is unsure of himself….. An investor should realize that some mistakes are going to be made and he should have sufficient diversification so that an occasional mistake will not prove crippling. However, beyond this point, he should take extreme care to own not the ost, but the best. In the field of common stocks, a little bit of a great many can never be more than a poor substitute for a few of the outstanding.”

If I have to summarize the above in just one word, I would say BALANCE.

Again, there is no one-size-fits-all balance for all investors. Balance of yours and mine might not be the same. And that’s fine. We shouldn’t mock each other. Rather, we should respect and learn from each of us.

I hope you now understand the meaning of the movie quote I introduced at the start. :)

Happy Investing!

| A guest post by

|

EDWIN CASTRO CHARITY HOME changed I and my family’s lives for good. Thank you so much for the work you do! I love your charity because it’s efficient, dedicated, honest, and it’s spiritually motivated, but doesn’t force one set of beliefs upon the recipients of your assistance.' I will continue to tell the world about your good work.