Deciphering The Digital Rupee

Disruption on the Cards?

We did a post recently where we pondered out loud about the possibility of physical cash going extinct. Will we talk about physical cash, like we talk about dinosaurs in the coming future?

Well, this is what we plan to explore along with our readers in this new edition of our Arthashastra 2.0 series, where we celebrate and chronicle the economic developments that are happening in our country.

I think it is a well established fact that India is a leader in digital payments. The scale and pace of blossoming that is happening in the fintech space in India is truly mind boggling.

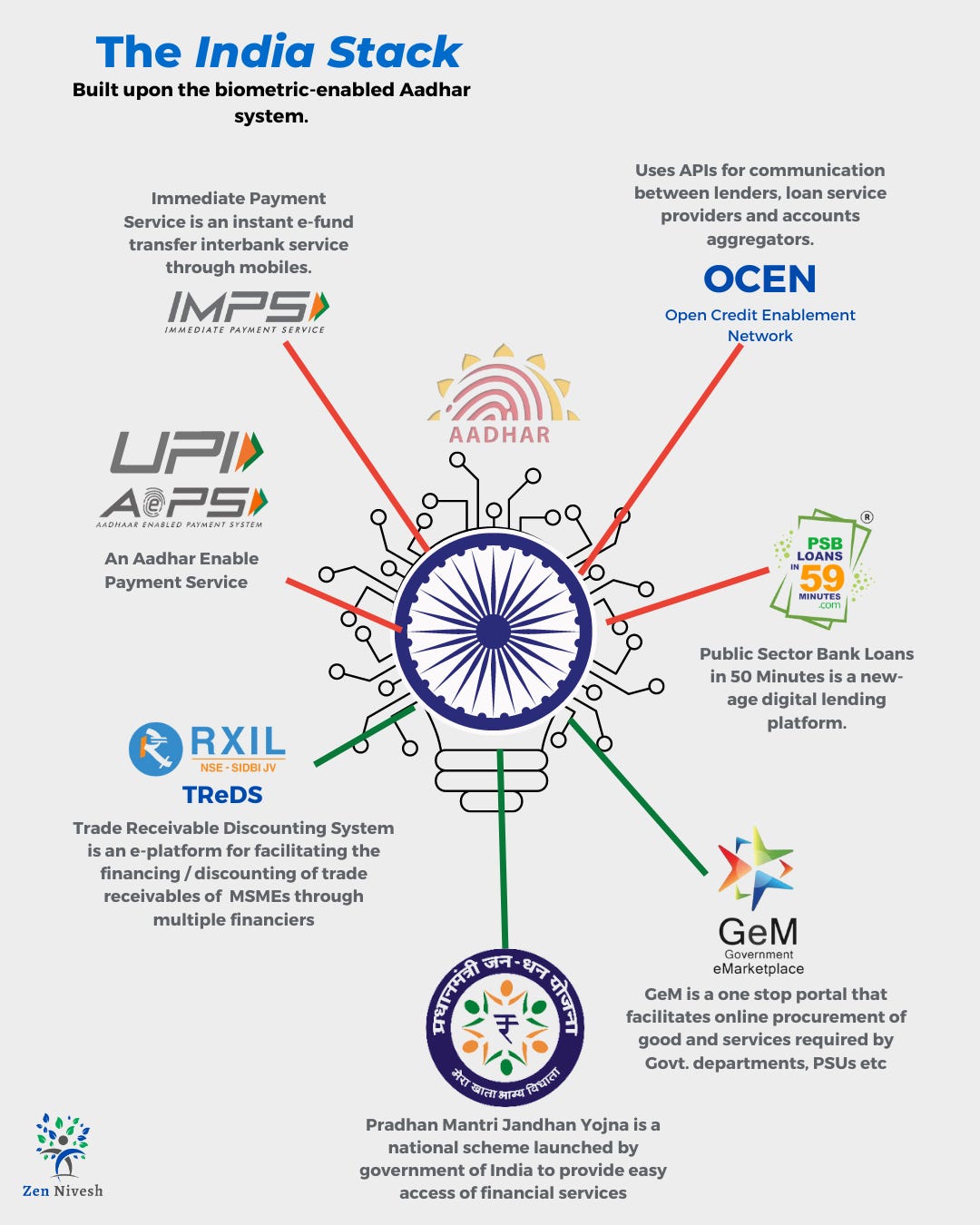

NPCI’s UPI has led the way and the Aadhar run India Stack is the motherboard which has powered its growth. But RBI is working on releasing one more innovation out in the open which might accelerate the process of sucking out physical cash from the economy.

You’ve read it right.

All About the Digital Rupee or CBDC (yes, we want to sound cool)

As we informed you in our previous post, RBI has come up with its own version of a digital currency, called the Central bank Digital Currency or CBDC.

CBDC is a legal tender, just like physical cash, issued by the central bank, just like physical cash and appears as a liability on the RBI’s balance sheet, just like physical cash. And aila, it can also be exchanged not only with digital currency, but also with physical cash! Plus, there was also UPI which is working perfectly fine!

So what’s the fuss about? Is RBI creating a solution looking for a problem? Or is CBDC touted to make a difference in how things function? Let us probe.

But before that. Let’s set the stage.

What Was the Need? Things are Working Just Fine, No?

We know that 90% of the countries in the world are working on CBDCs and the viability of launching it in their respective countries? What prompted this sudden change of heart from the central banks world over to take some time out from bashing crypto currencies like Bitcoin, Ethereum and the shitcoins and bringing their own version of it out?

Well, we’ll not go much into where the cryptos are right now and irk the hodlers (just a pun guys) by reminding them of the times when the cryptocurrencies were legit hot, stablecoins (crypto but essentially pegged with fiat currency) were growing in popularity and cryptos felt like truly disrupting the global financial systems.

The threat of a parallel economy was imminent.

This was the time when the world leaders and central banks formed a huddle (not literally) and became serious. Of course, who will want to cede their territory and power without a fight, right? Especially to a faceless, decentralized system created by the crypto currencies.

Cryptocurrencies were created to decentralize the power of a central bank or financial intermediaries post the blow up of the 2008 financial crisis. They operated over blockchain, had the control over the production of the new coins and the transactions were masked and safeguarded over the network. However, they did mean to solve a legitimate problem post 2008 but it couldn't help any nefarious activity happening on its network like all sorts of ‘bad’ transactions over the dark web and stuff. Plus, the reports of terror financing via cryptos were also on the rise. And let’s not talk about the determination of value of a crypto currency, because that’s a different ball game altogether. Let’s just say that the prices of cryptocurrencies are not stable enough to allow them to be used as a substitute of a fiat currency.

How are They Different From the Problem They Wish to Solve?

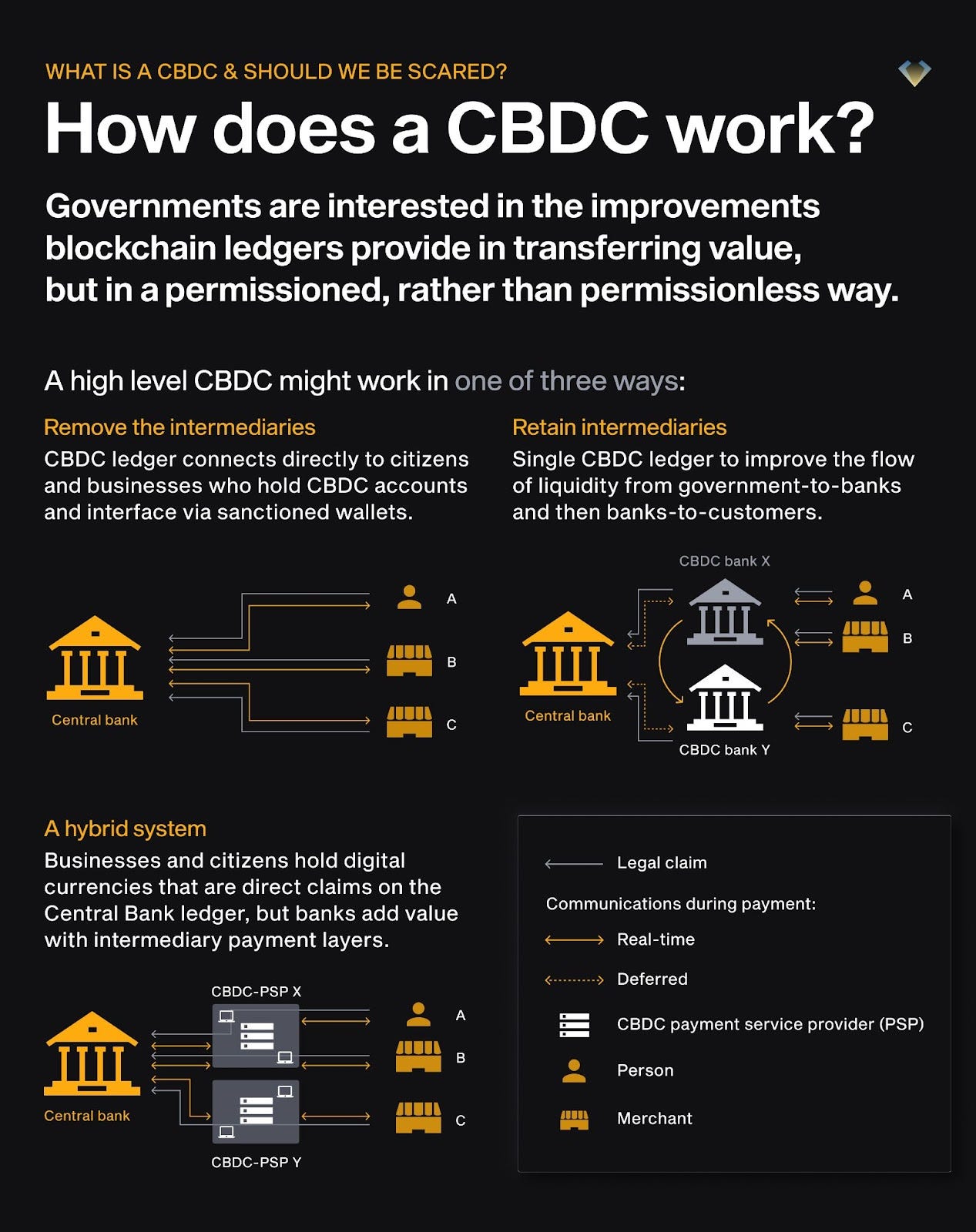

Enter CBDC. On the pretext of all the above points, the central banks thought that let’s strike when the iron is hot. CBDCs would operate over blockchain as well but they have the backing of the central bank and thus are centralized. Friends, Blockchain may sound complicated but let’s try to make it rather simple to understand by understanding what its utility is.

Blockchain is nothing but a ledger and a ledger is basically a place where records are kept. But we need to share the information in the ledger to relevant parties, no? Then it is also important that the records are kept safe, right? This is exactly what blockchain does! It ensures that the information which is recorded on its network cannot be changed, hacked or cheated on.

To achieve this, what blockchain does is - it duplicates and distributes the information by putting them in blocks with Z-security (just to help you visualize) across the network of computers. The security is so strong that if any block of information is changed or any attempt is made to change, it becomes apparent on the network! Essentially, the blockchain is a distributed digital ledger that records the transactions and ownership of digital assets.

And the central bankers were open enough to the idea of adopting this disruptive technology. They quietly worked on building their own version of a crypto minus the new world order objectives - in order to maintain the current world order.

And here comes the important difference between stable CBDC and highly volatile cryptocurrencies. Unlike cryptocurrencies, CBDC uses private, permissioned blockchain networks, in which case the recorded transaction details will only be available to the sender, receiver, and bank, not to the public. This means that data on this network cannot be accessed by everyone, and for this reason, it is considered a regulated or centralized security. This ensures that the privacy over the network is ensured. Well, they claim it to be.

What Will Change? Is India Ready for the Change?

Well, all this is well and good, from a consumer’s point of view, UPI is serving the purpose. Payments are instant, transactions are digital and recorded in real time on your Paytm’s payment history. What’s going to change?

This is a legitimate question.

For the consumer and a retailer? Not much, probably. But this will probably change how things work at the back office.

The tech has made things very fast, and probably so fast, that the financial system at the moment found it difficult to keep up. We might scan the QR code, enter a couple of numbers, scan our finger print and voila the shopkeeper says, “Aa gaya!”. You say “Thank You, bhaiya!” Job done.

But at the back-end, things are not so instant. Banks have to maintain a ledger of all the transactions happening countrywide and settle with each other as well as the RBI during night. Folks, it's enough to know that the settlement process is cumbersome. We might not know it but maintaining the current financial system can get very complicated.

And managing physical cash is expensive for the government - in every sense (printing, distribution and storage et al). Demonetization was just the beginning. Government wants less physical cash floating around and changing hands within our country because they have no idea what is happening with that money (Basically - Black money). And of course taxes and death are the only things which are certain! Plus, the cross border payments at the moment are very heavy on costs and not so instant. SWIFT sanctions on Russia will have made the rest of the world notice. Alternative global payments networks have become a talking point between trade partners.

So CBDC solves this problem for the government, however they have very clearly said that they brought CBDC to complement the current system of physical cash + UPI. They don't want CBDCs to be disruptive, but what is their end game? And is India ready for it?

We know that RBI has launched their pilot and how 9 banks have been onboarded. There were also certain images of the e- rupee stickers on some walls with a QR code at select cities. People having bank accounts with participating banks will be allowed to download the digital rupee wallet - just like a Paytm wallet- which would allow both person to person(P2P) or person to merchant (P2M)transactions, just like paper money or UPI transactions. The only difference between UPI and e-rupee is that with UPI, the banks act as intermediaries whereas CBDCs are transferred from one wallet to another with no role of banks in between.

Moreover it will be akin to the times when we used to keep cash in our physical wallets and spend only what was needed. The only difference would be the physical wallet would be your mobile powered digital wallet.

Conclusion

Although, as of now only a select few wallets have been fuelled with CBDCs and the RBI plans to slowly scale its operations after evaluating the trials results. Mass withdrawals, incentives for deposits and as is the case with today’s tech - anonymity is the issue that RBI must seek answers for. Otherwise, we would like to reiterate (probably it is because we like the sentence too much) - RBI is only creating a solution looking for a problem.