From Slices to Shares

How to make sense of ESOPs, dilution, and shareholder value | Issue #14

As the title suggests, let me start with a pizza story.

Four friends go to a restaurant. They ordered 1 pizza (8 slices) like this one.

They plan to divide it equally, 2 slices each for all four of them. I wouldn’t be satisfied with just two slices. But let’s not digress.

So far, clean and fair. 4 friends. 2 slices each. 8 slices in total.

Just as they’re about to start eating, a 5th friend shows up. He hasn’t paid for the pizza, but he’s a close buddy, and the group wants him included.

Now, if they cut the same pizza into 5 equal portions, each friend gets 1.6 slices instead of 2.

That’s dilution. Everyone’s share becomes a bit smaller.

Dosti leading to dilution.

I will be honest. If I had been one of the four friends, I would not just be sad. I will be like this.

Any self-respecting pizza lover will feel like that. Everyone may not scream out in the open like Gabbar or me, but I know. And I know you know, too.

Now, what if I told you this?

The pizza = company’s total ownership (shares).

The 4 friends = current shareholders.

The 5th friend = employees who get ESOPs.

When the company issues ESOPs, it’s like inviting the employee to the table without increasing the size of the pizza. The existing shareholders’ slices get a little smaller.

Current shareholders know this. The company knows this. And the employee who got the chance to join the table also knows this. So, why does it happen? There is a straightforward reason for the same.

The idea is that by adding this new friend (employee), the whole group enjoys the outing more. Maybe he orders drinks, cracks jokes, or makes the experience richer.

In real corporate and investing situations, it works like this.

Employees are given stock options (the right to buy shares in the future, usually at a discount).

When they exercise, new shares are issued, and existing shareholders’ ownership % is reduced (their slices shrink).

The hope is that these motivated employees will grow the “pizza” (make the company bigger and more valuable), so that even a smaller slice is worth much more.

ESOPs = inviting new friends to share your pizza.

Yes, your own slice gets smaller, but if that friend helps you order more pizzas later, everyone ends up with more food than before.

And if you have now understood the concept of ESOPs, it will be easy for you to understand the issue of warrants, preferential allotment, QIPs, and right issue. But I will focus only on ESOPs in this post.

Let’s consider two examples where ESOP issuance occurred, but the dilution was negligible.

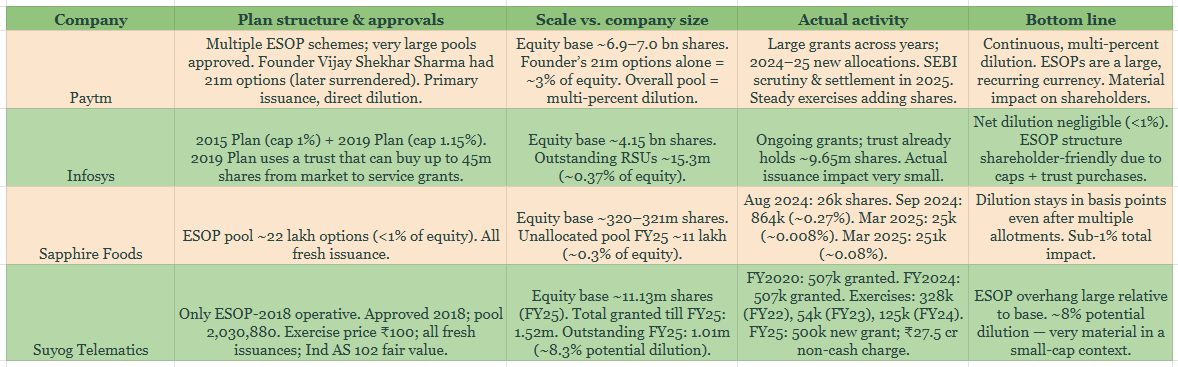

Infosys: Negligible dilution, capped and mitigated

Plan structure & approvals

2015 Stock Incentive Compensation Plan and Expanded Stock Ownership Program 2019.

Hard caps: 1% (2015) and 1.15% (2019) of issued capital.

The 2019 Plan uses a controlled trust that can buy up to 45 million shares from the market, limiting fresh issuance.

Scale vs. company size

Equity base: ~4.15 billion shares (FY25).

Outstanding RSUs at FY25: ~15.3 million units.

If all vested/exercised: ~0.37% of equity.

Actual activity

Ongoing grants across employee levels.

Controlled trust already holds ~9.65 million shares to service exercises.

Actual net dilution impact kept very small.

Bottom line (Infosys)

Between hard plan caps and the trust-route settlement mechanism, Infosys has designed its ESOP programs to be shareholder-friendly. Net dilution remains well below 1%, even with continuous grants.

Sapphire Foods — Small pool, bite-sized issuance

Plan structure & approvals

Operates an ESOP scheme with a total pool of ~22 lakh options.

All are primary issuance.

Pool size deliberately kept at sub-1% of equity.

Scale vs. company size

Equity base: ~320–321 million shares.

Unallocated pool in FY25: ~11 lakh options, ~0.3% of equity.

Maximum potential dilution comfortably below 1%.

Actual activity

Aug 2024: ~26,000 shares allotted.

Sep 2024: ~864,000 shares allotted (~0.27% dilution).

Mar 2025: ~25,000 shares allotted (~0.008% dilution).

Mar 2025: ~251,000 shares allotted (~0.08% dilution).

Bottom line (Sapphire Foods)

Even when multiple tranches are exercised in the same year, the aggregate dilution is in basis points. This is a textbook example of a mid-cap company running ESOPs without meaningful shareholder impact.

In these two cases, we have seen that despite ESOP issuance, the dilution has been insignificant. So, it doesn’t hurt the existing shareholders. It’s just like the four friends had to share the first pizza with the 5th guy, but the 5th guy made the whole experience richer by being a good conversationalist and ordering cold drinks from his side. Hence, the dilution of pizza slices does not hurt.

Now let’s look at a couple of cases where the dilution hurts. The new guy comes, takes a part of your pizza slice, but does not provide any meaningful value. At least not at that moment. That’s called significant dilution. Let us check the following two instances.

Paytm (One97 Communications): Large ESOP overhang

Plan structure & approvals

Multiple ESOP schemes over the years, with very large pools approved.

Founder Vijay Shekhar Sharma had 21 million options under grant, later surrendered in 2025.

Plans rely on primary issuance, leading to direct dilution.

Scale vs. company size

Equity base: ~6.9–7.0 billion shares.

Founder’s 21 million options alone = ~3% of equity.

Across all pools, potential dilution runs into multiple percentage points.

Actual activity

Several large grants across years, including 2024–25 allocations to senior management.

SEBI scrutiny and settlement in 2025 over ESOP-related matters.

Exercises steadily add to share count.

Bottom line (Paytm)

With a multi-percent ESOP overhang and continuous new grants, dilution is structurally significant. While the company positions ESOPs as key to retaining talent, shareholders face ongoing dilution that is non-trivial.

Suyog Telematics: Material dilution in a small-cap

Plan structure & approvals

Only one operative scheme: Suyog Stock Option Scheme 2018 (ESOP-2018).

Approved in Sep 2018, pool size 2,030,880 options.

Exercise price fixed at ₹100.

All fresh issuances, fair value accounting (Ind AS 102).

Scale vs. company size

Equity base: ~11.13 million shares (FY25).

Total granted till FY25: ~1.52 million options.

Outstanding at FY25: ~1.01 million.

Potential dilution: ~8.3% if all exercised.

Actual activity

FY2020: 507,720 options granted.

FY2024: 507,720 options granted.

FY2022: 328,000 exercised; FY2023: 54,400 exercised; FY2024: 125,320 exercised.

FY25: ~500,000 new options granted; non-cash ESOP charge ~₹27.5 cr booked.

Bottom line (Suyog)

For a company with just ~11 million shares, an ESOP overhang of ~1 million is very large. The ~8% potential dilution is highly material for shareholders and must be tracked closely.

I have used exchange filings of the above four companies to come up with these back-of-the-envelope calculations. I do not claim to be 100% accurate in these calculations. The purpose is to make you understand the concept of ESOP and dilution. As they say, it is better to be roughly right than precisely wrong. 🙂

The title of the blog is

From Slices to Shares

How to make sense of ESOPs, dilution, and shareholder value

I have covered slices, shares, ESOPS, and dilution. But I have not covered anything on shareholder value yet.

Let me end this blog with a real story where there are slices, new share issues, dilution, and yet, amazing wealth creation for the old shareholders who stayed put over the long run.

Conclusion: Share, slices, dilution, and wealth creation. All stitched together.

The Backdrop

Info Edge (India) Ltd, the parent of Naukri.com, was an early investor in Zomato, starting way back in 2010. They initially invested just a few crore rupees, picking up a large early stake when Zomato was a small food discovery startup.

The Dilution Story

Over the years, Zomato raised multiple funding rounds from global investors like Sequoia, Temasek, Tiger Global, Ant Financial, Fidelity, etc. Each new round meant Info Edge’s % shareholding got diluted (from ~57% in 2010 to ~15% by the time of IPO in 2021). In traditional thinking, going from majority ownership to a minority stake looks like a “loss of control” and dilution of value.

The Wealth Creation

But here’s what happened:

Even though Info Edge’s stake fell from 57% to ~15%, the absolute value of that smaller stake ballooned. At IPO in July 2021, Zomato was valued at ₹1 lakh crore+. Info Edge’s ~15% stake alone was worth ₹15,000–18,000 crore.

Compare this with their initial investment of ~₹30–40 crore. That’s a 400x+ return despite massive dilution.

The Lesson for ESOP / Dilution Understanding

Dilution looks bad if you only see your shrinking % stake (2 slices becoming 1.6 slices).

But if the pizza itself grows from a roadside 8-inch to a giant 48-inch pie, your slices may actually be worth 6x more than your original 2 slices.

That’s exactly what happened with Info Edge’s Zomato investment.

Continuous dilution wasn’t a problem because the value creation per share was far larger than the loss of percentage stake.

This is why investors (and founders too) should focus on growing the absolute size of the pie, not just protecting their slice.

However, one should be careful of the opposite story. When a picture is worth a thousand words, I will share just three of them for you to understand the context.

I have a simple task for you.

Find out the name of the company, and compare the following three things:

Current Market Cap

Reserves in the Balance Sheet

Funds raised in its lifetime.

Waiting for your reply in the comments. :)

Thanks for reading.

| A guest post by

|

Jain Irrigation Systems Ltd’s key financial figures as of 2025:

• The company’s current market value (market capitalization) is about 3,500 to 3,800 crore rupees. This means how much the whole company is worth according to the stock market right now.

• The company’s reserves (saved money and profits kept in the balance sheet) are around 5,400 to 5,500 crore rupees. This shows how much money the company has saved over the years from its earnings.

• Over its lifetime, Jain Irrigation has raised more than 2,000 crore rupees through different fundraisings and investments by investors. This money helped the company grow and reduce its debt.

In simple terms, the company is currently valued at about 3,500 crore rupees by investors, has saved over 5,400 crore rupees in reserves, and has raised a total of over 2,000 crore rupees in funds since it started. The reserves are more than the market value, showing it has strong retained earnings, while the funds raised show its ability to get capital support for growth and managing debt.

Jain Irrigation:

Market Cap: USD 432 MM

Reserves: USD 30MM