Paytm: A Deep Dive!

Roaring IPO | Rags to Riches | Regulatory Shocks | Regular Reinvention | Research Lab #50

Yay!

We hit the half-century.

In about 13 months, this is our 50th Zen Nivesh blog on a business/industry deep-dive.

As we celebrate this big occasion, I thought let’s cover a big company. :)

Let’s get started straightaway.

Unpopular Opinion:

Vivid scenes are overrated. Business pivots are underrated.

Let me share a few vivid scenes.

Scene 1: Elation is the emotion

Scene 2: The Rags to Riches Story of a Start-up Founder hailing from a tiny village

Scene 3: Laughter and Joy

Scene 4: Overconfidence

We remember businesses through vivid snapshots. A failed acquisition. A regulatory issue. A bad quarter. A temporary collapse. And then we freeze that image in our minds for years. What we often miss is that businesses evolve through multiple pivots across decades. Quietly. Painfully. Slowly. Long before the headlines acknowledge it. It is similar to a bright young student who spends years mastering chemistry, only to realize that the world is moving elsewhere gradually. Opportunities are shrinking. Demand is fading. Relevance is shifting. And now comes the hard part, starting again from scratch, learning history and geography, because that is where the future seems to be unfolding. Business pivots work the same way. They are rarely dramatic overnight transformations. They are long, uncertain journeys of unlearning, rebuilding, surviving, and adapting while the world still remembers you for who you used to be. I am going to talk about one such story today.

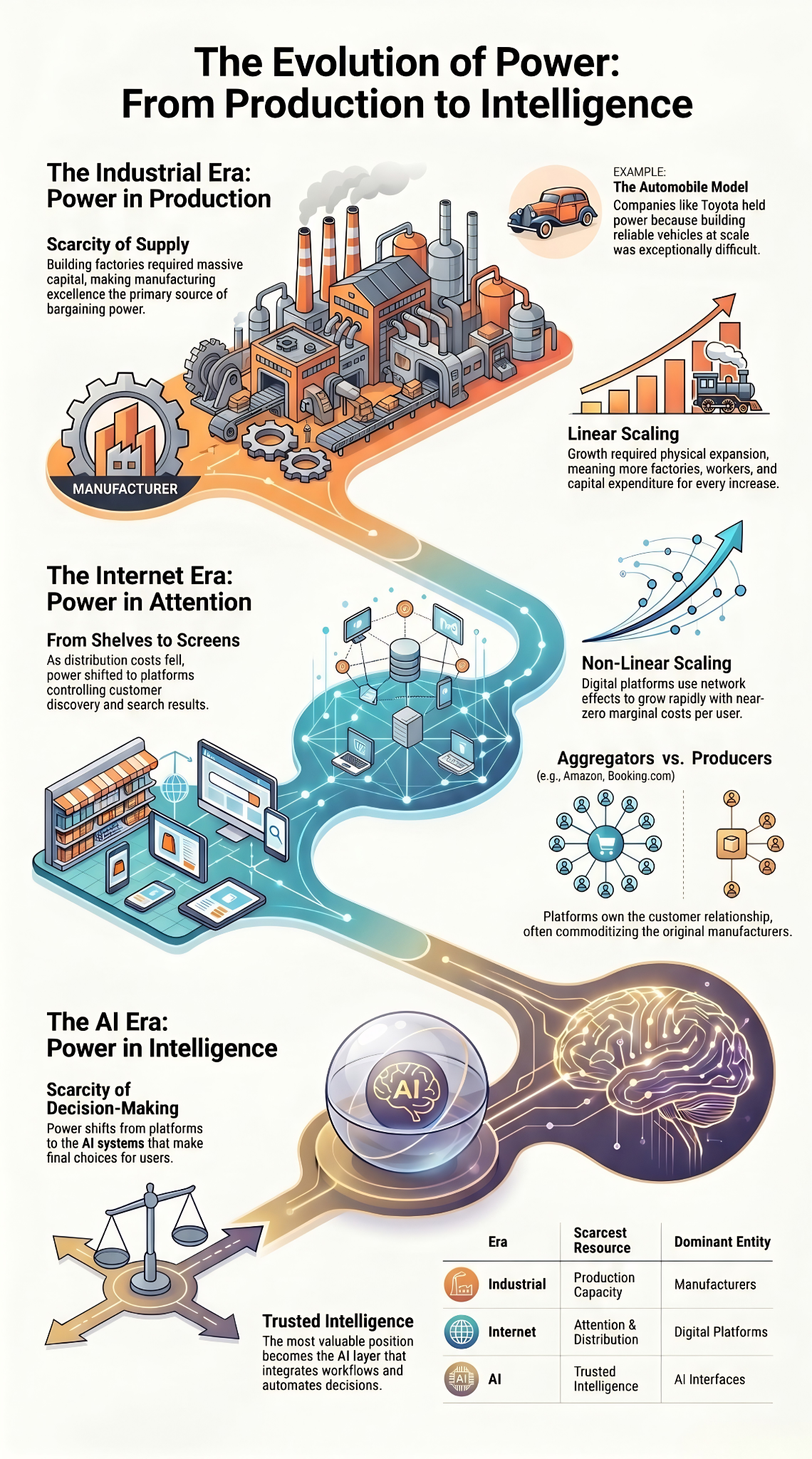

The Shift of Power Across Business Eras

One of the best ways to understand business history is to track where power sits in the value chain across different eras. In the industrial age, manufacturing held power because production was scarce, difficult, and capital-intensive. Companies like Toyota, Honda, and Maruti Suzuki dominated because building reliable products at scale was the key bottleneck. The internet changed this by making distribution cheap and products abundant, shifting scarcity from supply to attention. As a result, digital distributors like Amazon, Flipkart, Booking.com, Swiggy, Zomato, YouTube, and Instagram became more powerful than many producers because they controlled discovery, traffic, algorithms, payments, and customer relationships. Manufacturers increasingly operated inside ecosystems they did not control. Digital businesses also scaled non-linearly through network effects, making platforms disproportionately powerful. Yet some manufacturers like Apple, NVIDIA, and TSMC retained power because they controlled ecosystems, technology, intellectual property, or highly specialized production. Now the AI era may trigger another shift, where power moves toward whoever controls trusted intelligence, recommendations, workflows, and decision-making itself. History repeatedly shows that the biggest businesses of every era usually control the scarcest resource of that era: manufacturing in the industrial age, attention in the internet age, and perhaps trusted intelligence in the AI age.

The Indian Digital Payments Ecosystem

The Indian digital payments ecosystem is better understood through the layer controlling customer behaviour and transaction flow. Earlier, banks owned the customer relationship through branches, accounts, and payment infrastructure. But with smartphones and the internet, platforms like Paytm, PhonePe, and Google Pay moved closer to consumers, making the payment experience associated more with the app than the bank underneath. Banks still hold deposits and settle transactions, but payment apps increasingly control engagement, merchant discovery, transaction frequency, and user habits. What made India’s payments story unique was that these “digital” businesses scaled through one of the country’s largest physical merchant onboarding exercises. QR codes across kirana stores, tea stalls, pharmacies, and roadside shops became a new distribution network, built merchant by merchant across the country. Once merchants entered an ecosystem, platforms gained transaction data, behavioural insights, and cross-selling opportunities across loans, insurance, wealth products, advertising, and software tools. This is why competition became intense despite UPI being an interoperable infrastructure, because the real battle shifted to consumer attention and merchant relationships layered on top of common rails. Successful internet businesses rarely remain purely digital. Just as Amazon built warehouses and logistics, Indian payment companies built large offline merchant networks. The internet era did not eliminate physical distribution; it redefined it. In India, especially, the strongest digital businesses combine software scale with deep real-world distribution built shop by shop across the country.

The Competitive Landscape of UPI

The UPI landscape today is nothing but digital distribution power at scale. While UPI is a public infrastructure built by the National Payments Corporation of India, the real battle sits at the app layer, where companies compete for consumer habits, transaction frequency, and merchant relationships. PhonePe and Google Pay together control nearly 80% of India’s UPI transaction volume, with PhonePe alone processing close to 10 billion monthly transactions and building one of the deepest merchant networks in the country through QR penetration across towns, kirana stores, pharmacies, and street vendors. Paytm, despite a lower market share today, still retains one of India’s strongest offline merchant ecosystems built during the post-demonetisation era. Smaller players like Amazon Pay, CRED, Navi, and Supermoney are trying to build niche positions, but the gap with the top players remains massive. Interestingly, UPI is no longer just a payments business because payments themselves generate little direct revenue. The real value lies in owning consumer behaviour, transaction data, and merchant relationships, which can later be monetised through loans, insurance, wealth products, commerce, and advertising. Much like the broader internet economy, banks increasingly operate invisibly in the background while the payment app becomes the primary customer interface. And unlike pure software businesses, the strongest UPI companies combined digital habit formation with massive physical distribution, turning QR stickers into one of the largest retail distribution networks India has ever seen. The app may look simple on the surface. But beneath it sits one of the largest distribution networks India has ever built.

This piece is not about the 80% of the market. It is about a player who has a single-digit market share. Is it a tiny fish in front of the two sharks? Or maybe not. Let’s find out.

PayTM or One97 Communications, since its inception, has witnessed multiple pivots. Let’s go through each one of them chronologically.

1. One97 phase, before Paytm existed

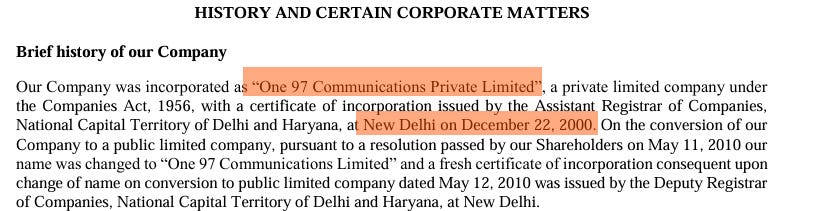

Many do not know this. Paytm did not begin as a payments company. It began inside One97 Communications, incorporated in 2000, as a mobile value-added services business.

This was the pre-smartphone, pre-UPI, pre-cheap data India. The opportunity was not digital payments. The opportunity was telecom distribution. Mobile users needed ringtones, jokes, cricket alerts, astrology, caller tunes, recharge support, and small mobile content products. One97 built itself around this telecom layer. Paytm’s first real capability was not banking or finance. It was serving a very large number of small-ticket mobile users through telecom rails.

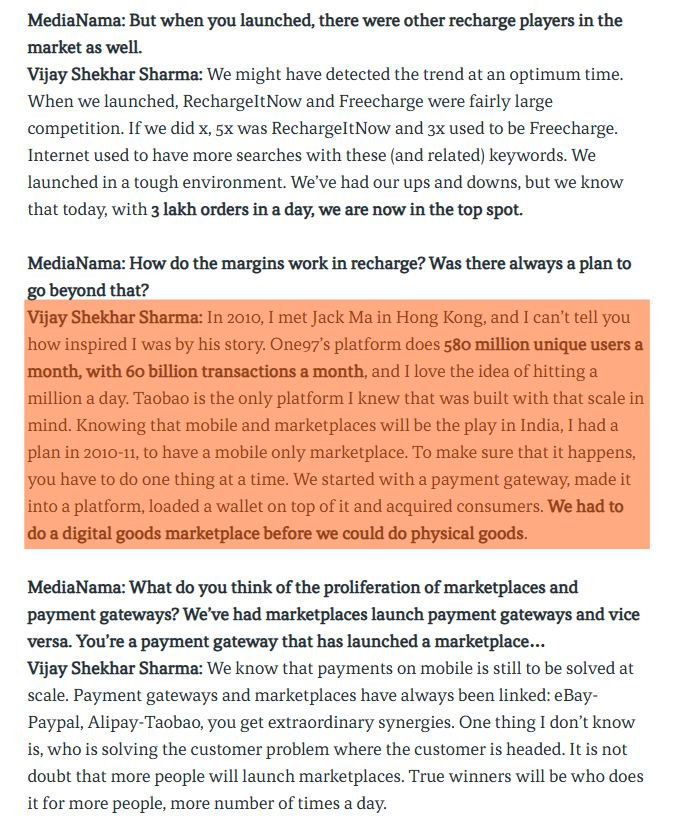

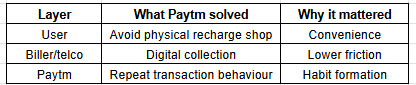

The first version of Paytm, launched in 2010, was a natural extension of that world. India was a prepaid telecom market. Most users recharged phones frequently, often with cash through local retailers. Paytm digitised that behaviour. It started with prepaid mobile and DTH recharge, then expanded into bill payments. In simple terms, Paytm’s first consumer promise was: “Instead of going to a shop for a recharge, do it on your phone.”

2. Recharge app phase, utility before finance

The recharge business was useful because it created frequency. A user may not shop online every day, but prepaid recharge, bill payment, DTH recharge, and utility payments create repeated use cases. This gave Paytm three early assets: user habit, payment data, and trust in small-value transactions. At this stage, Paytm was not yet a full fintech ecosystem. It was closer to a digital utility counter. The business model depended on payment convenience, commissions from recharge and biller ecosystems, and the ability to bring users back into the app again and again. It was still a transaction business, not yet a financial services platform.

The logic was simple. This was the seed of Paytm’s later super app ambition.

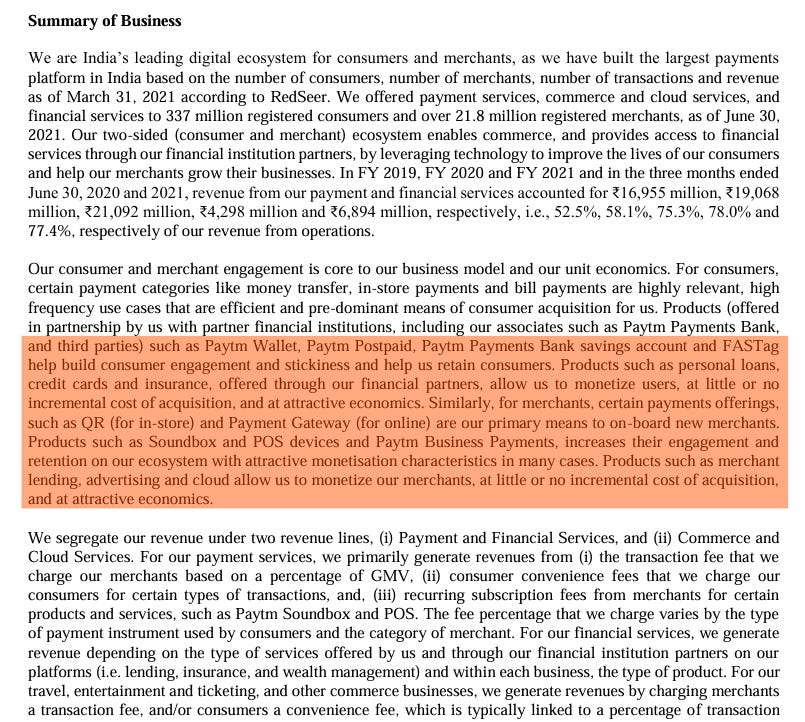

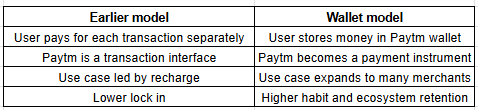

3. Wallet phase, Paytm moves from transaction to stored value

The real business model shift happened when Paytm moved from recharge to wallet. A recharge app helps users complete a transaction.

A wallet keeps money inside the ecosystem. This changed Paytm from being a pass-through platform into a semi-closed payment instrument. The wallet allowed users to load money once and spend multiple times. That improved transaction speed and reduced repeated payment friction. It also helped Paytm build use cases beyond recharge, including bill payments, online merchants, ticketing, travel, and later offline QR payments.

This was the first big platform transition. The wallet also gave Paytm a strong brand recall before UPI became dominant. For many users, “Paytm karo” became shorthand for digital payment.

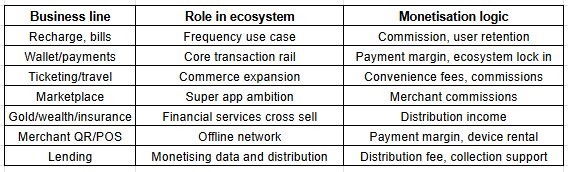

4. Expansion phase, Paytm tries to become a consumer internet platform

After wallet adoption, Paytm expanded aggressively. It added movie tickets, travel, events, gift cards, utility payments, commerce, gaming, gold, wealth, insurance, credit cards, and other financial services. This was the period where Paytm behaved less like a narrow payments company and more like a consumer internet super app.

The logic was understandable. Payments are high-frequency but low-margin. Once a user trusts a wallet, the company can cross-sell higher-value products. So Paytm tried to convert payment users into commerce users, commerce users into financial services users, and merchants into business customers. However, this expansion also made the business harder to understand. Paytm was simultaneously a recharge app, wallet, marketplace, ticketing platform, merchant acquirer, bank-linked payments player, wealth distributor, credit distributor, and advertising platform. The opportunity was large, but the business model became complex.

Paytm was trying to use payments as the entry point into multiple profit pools.

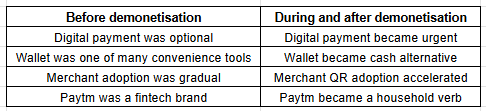

5. Demonetisation phase, Paytm gets its biggest adoption shock

The November 2016 demonetisation event was a major inflection point.

Cash availability suddenly collapsed. Merchants and consumers needed an immediate alternative. Paytm already had a wallet, brand, app, and QR-based merchant payment push. So the company became one of the most visible beneficiaries of demonetisation. This period did not create Paytm from scratch, but it compressed adoption. Behaviours that might have taken years were forced into weeks. Small merchants who may not have cared about digital payments earlier suddenly had a reason to display a Paytm QR code.

This was a classic adoption shock. But demonetisation also created a later challenge. Rapid adoption can build scale faster than compliance, operations, KYC discipline, and risk systems mature. That became important in the payments bank story later.

6. Merchant QR phase, Paytm moves offline

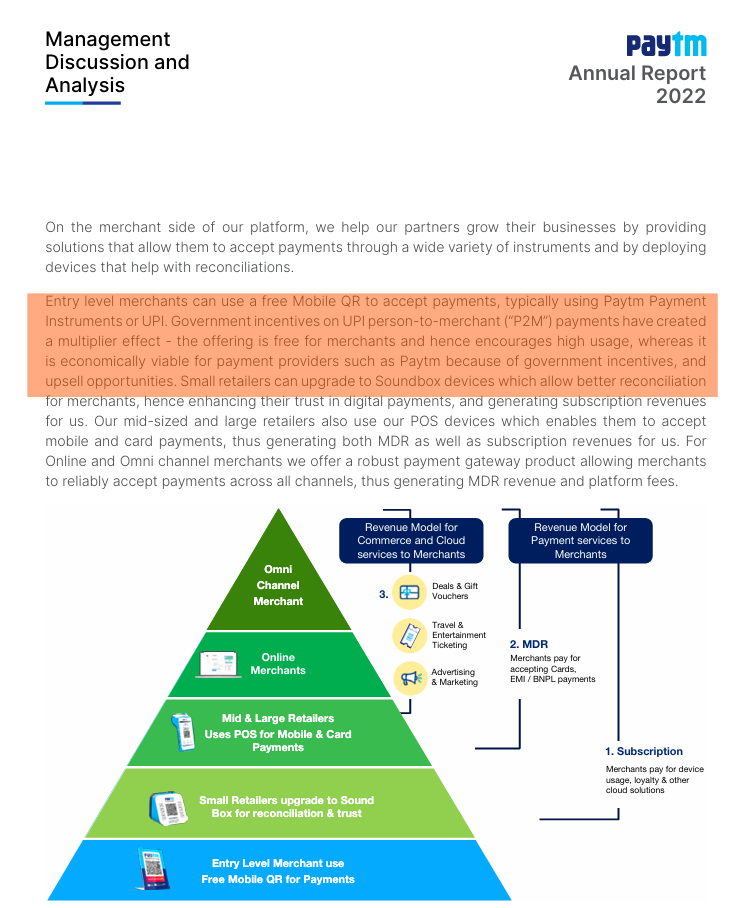

Paytm’s next major shift was from consumer wallet to merchant acceptance network. This is extremely important. A wallet app is useful only if users can spend the balance. Paytm needed acceptance points. QR codes solved this cheaply. Instead of deploying expensive card machines, Paytm could give merchants a QR code. The merchant did not need major hardware. The customer scanned and paid. For small merchants, this was simpler than card acceptance. For Paytm, every merchant QR increased the usefulness of its consumer app. This created a two-sided network. The strategic value was not only payment revenue. Merchant acquisition created a base for future products: Soundbox, POS, working capital loans, advertising, business app, insurance, and other merchant services.

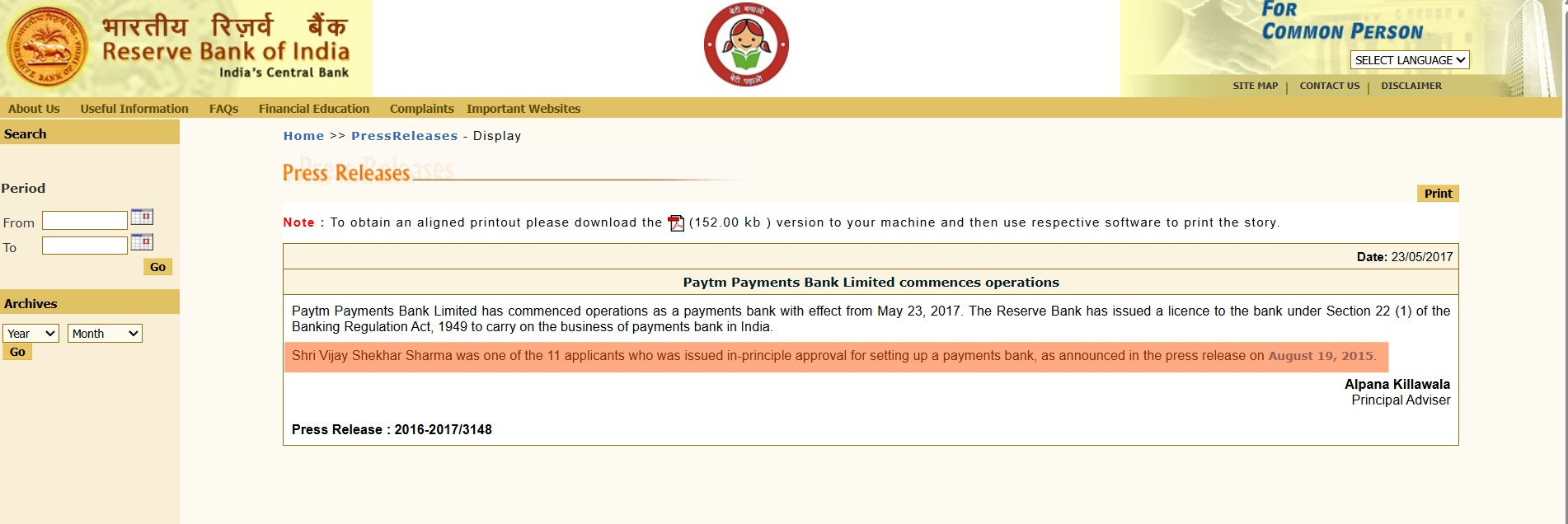

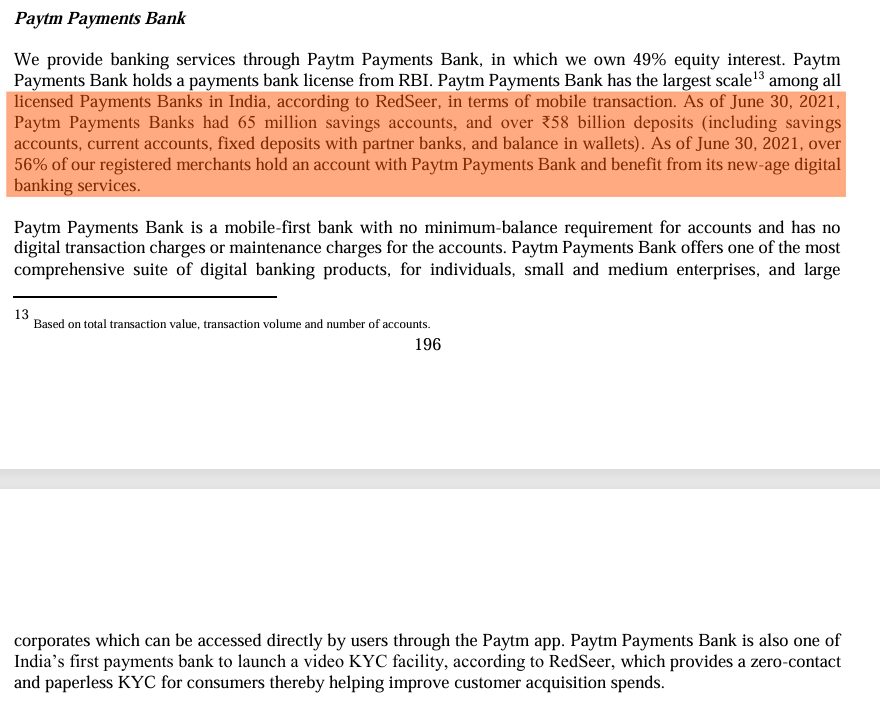

7. Payments Bank phase, Paytm enters the regulated banking infrastructure

The payments bank idea was meant to deepen Paytm’s financial infrastructure. RBI gave in-principle approval in 2015, and Paytm Payments Bank started operations in 2017.

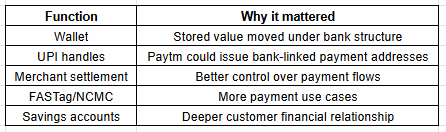

A payments bank can accept deposits, issue debit cards, enable payments, and support banking access, but it cannot lend like a normal bank. This was a critical distinction. Paytm Payments Bank could help Paytm own more of the payment stack, but it could not become a full lending institution. It was useful for wallets, savings accounts, FASTag, UPI handles, NCMC cards, merchant settlement, and banking access. But the economics of a payments bank are structurally limited because it cannot lend customer deposits.

The payments bank gave Paytm more control. But it also increased regulatory responsibility. Once Paytm had an associate bank, compliance expectations were much higher than for a pure technology platform.

8. UPI phase, wallet loses some structural advantage

UPI changed the industry. Earlier, wallets were useful because they made small digital payments easy. UPI made direct bank-to-bank payments easy.

This reduced the structural need for wallets. For Paytm, UPI was both a threat and an opportunity. It was a threat because wallet balances were no longer necessary for many transactions. A user could pay directly from any bank account. It was an opportunity because Paytm could still own the front end, the QR, the merchant relationship, and the payment experience.

So Paytm’s model shifted again:

This is why Paytm had to go deeper into merchant devices and financial services. Pure UPI payments had limited direct economics.

9. Soundbox phase, monetisation improves

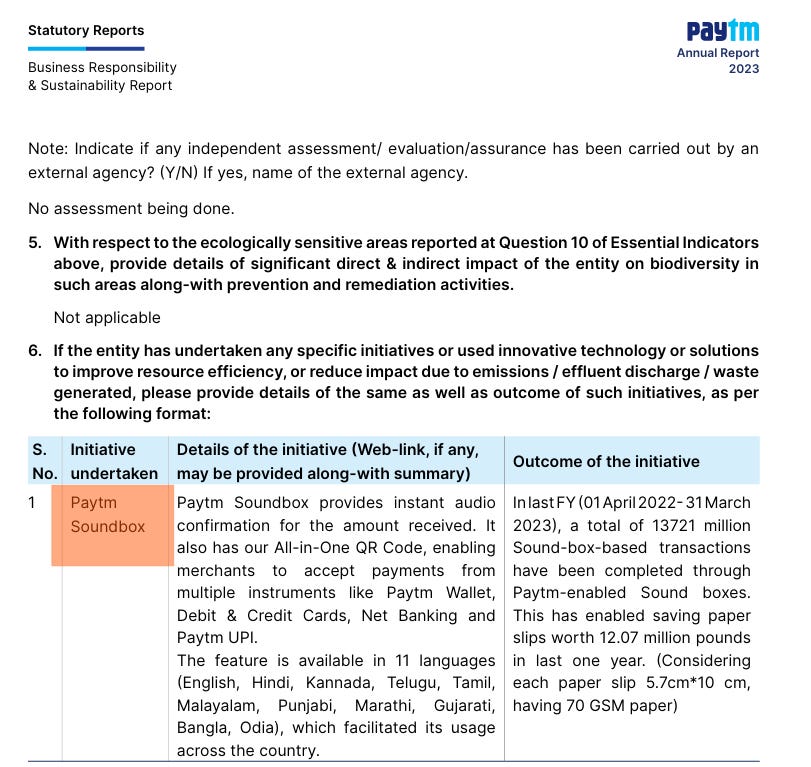

Soundbox was one of Paytm’s most important business model innovations. A QR code alone is useful, but it creates a trust problem for merchants. The merchant has to check whether payment was actually received. In a busy shop, this is painful. Soundbox solves that by giving instant audio confirmation.For the merchant, Soundbox is not a fancy device. It is a trust device. It says, “Payment received.” That reduces fraud anxiety and operational friction. For Paytm, Soundbox changed the economics of merchant payments.

Payments themselves can be low margin, especially UPI. But a device can be rented monthly. Paytm’s investor materials describe revenue from payment services as coming from payment processing margin and merchant subscription revenue, and specifically mention Soundbox as a pioneering device that helped merchant acquiring. This is the key model shift. Soundbox made Paytm less dependent on payment MDR alone. It also made the merchant relationship more physical and sticky.

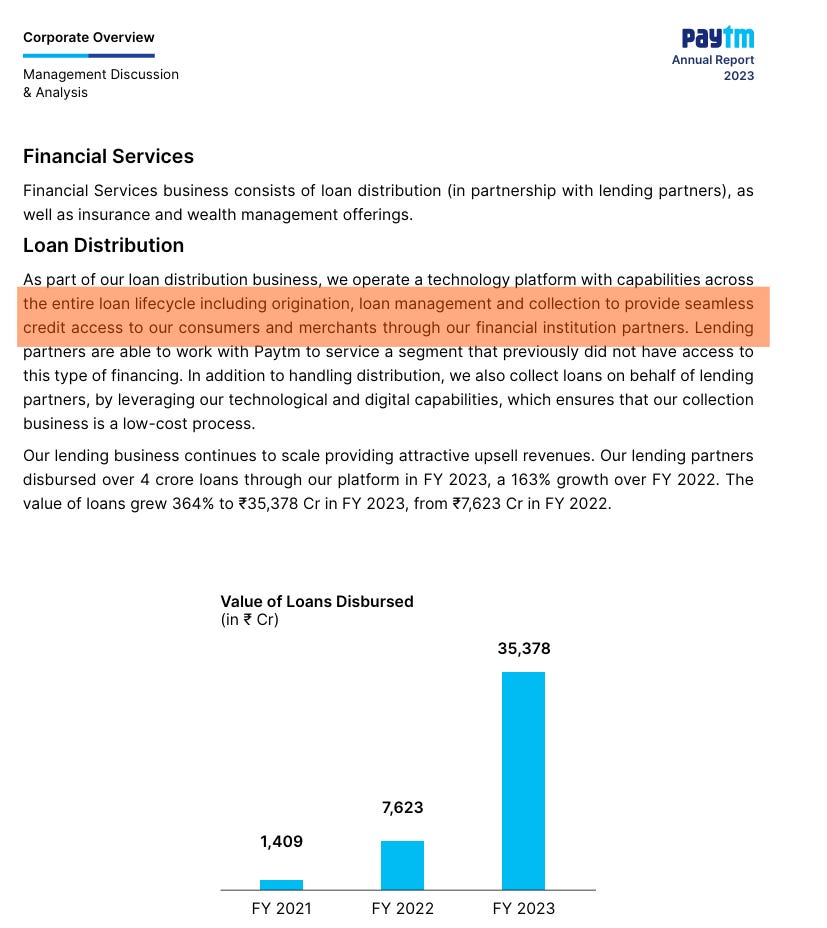

10. Lending distribution phase, Paytm monetises data and access without becoming a lender

Because Paytm Payments Bank could not lend, Paytm built lending through partnerships. The idea was to use its consumer and merchant data, transaction history, and distribution reach to help lending partners originate loans. This is an important distinction. Paytm was not primarily trying to become a balance sheet lender. It positioned itself as a loan distributor and technology platform. In FY24 commentary, Paytm said credit growth would be led by a “distribution only disbursement model.” For merchants, the pitch was simple: if Paytm can see your daily transactions, settlement flows, and business activity, it can help a lending partner underwrite a small business loan. For Paytm, lending distribution was attractive because it could generate higher margin revenue than payments alone.

The lending model looked like this:

This model depends heavily on partner confidence, compliance, collection quality, and regulator comfort.

11. IPO phase, public market asks for clearer economics

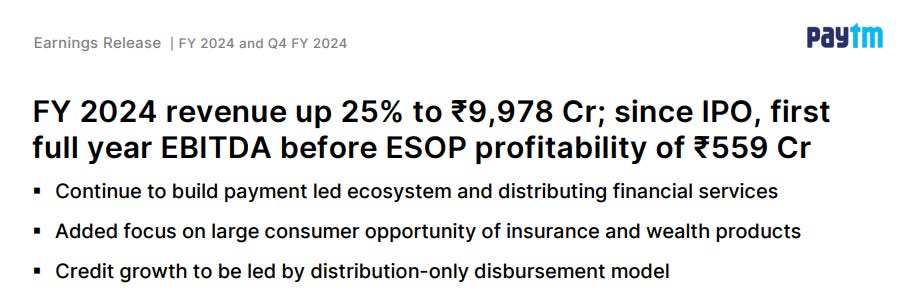

Paytm listed in November 2021. By then, it was a large fintech ecosystem but still loss making. The IPO forced public investors to ask a basic question: what is Paytm actually? Was it a payments company? A lending platform? A merchant technology company? A super app? A financial services distributor? A commerce company? The answer was: all of the above, but the market wanted proof of sustainable monetisation. Over time, Paytm’s public market narrative moved toward a cleaner structure: Payments as acquisition and engagement engine. Merchant subscriptions as recurring revenue. Financial services distribution as profit pool. Marketing services as additional monetisation. Operating leverage through scale. By FY24, Paytm reported 25 percent operating revenue growth, driven by GMV growth, device additions, and financial services distribution. It also reported net payment margin growth of 50 percent to ₹2,955 crore due to payment processing margin and merchant subscription revenue.

12. Regulatory pressure phase, Paytm Payments Bank becomes the weak link

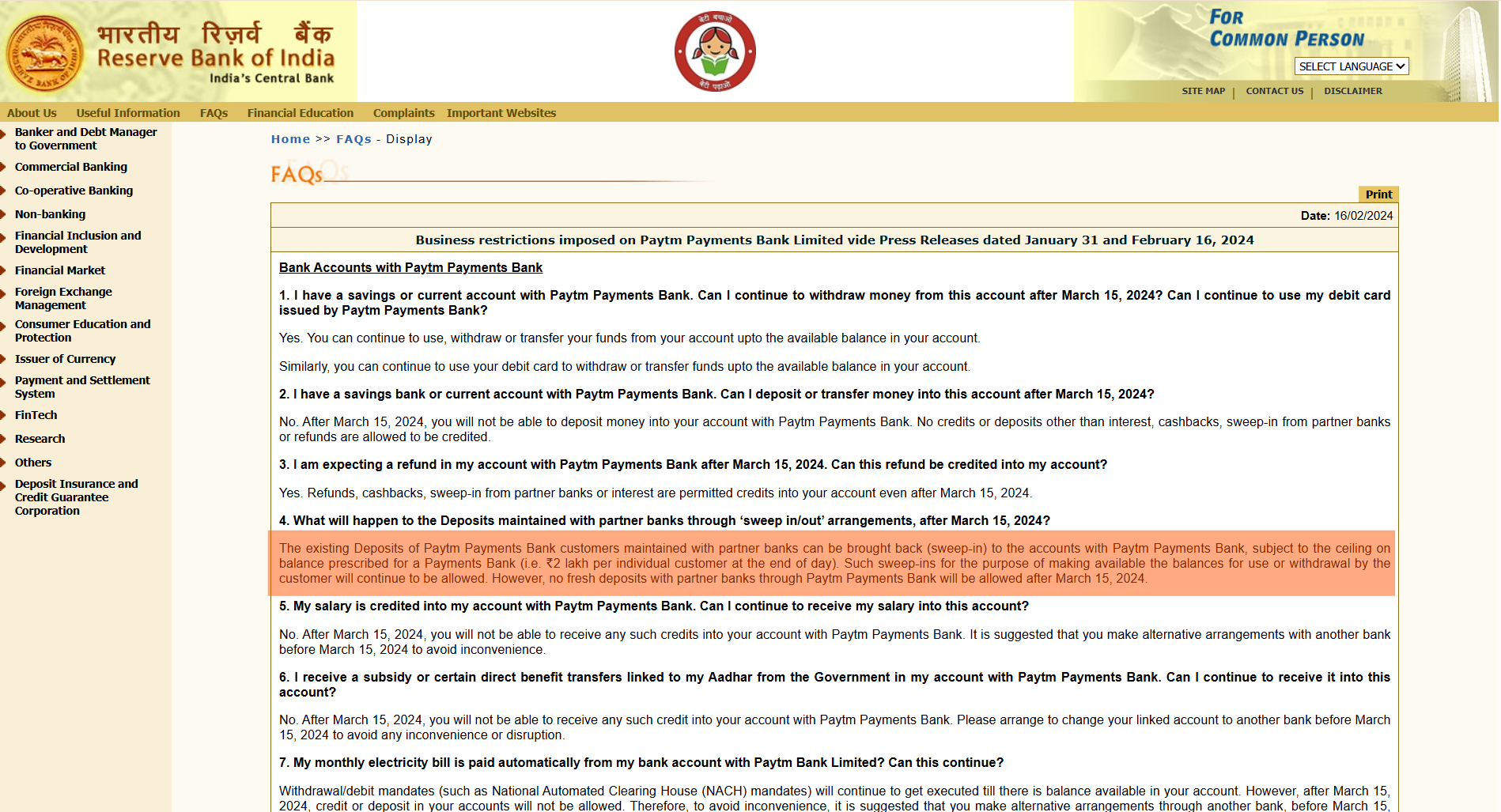

The regulatory issues around Paytm Payments Bank did not begin with licence cancellation. RBI first directed the bank to stop onboarding new customers from March 11, 2022. Later, on January 31, 2024 and February 16, 2024, further restrictions were imposed. RBI noted that business restrictions disallowed further deposits, credits, and top ups into customer accounts, wallets, and other instruments.

The February 2024 RBI FAQ made the practical effect very clear. Existing users could withdraw or use available balances, but after March 15, 2024, they could not deposit money into Paytm Payments Bank accounts, could not top up wallets, and merchants linked to Paytm Payments Bank accounts or wallets had to shift settlement arrangements elsewhere.

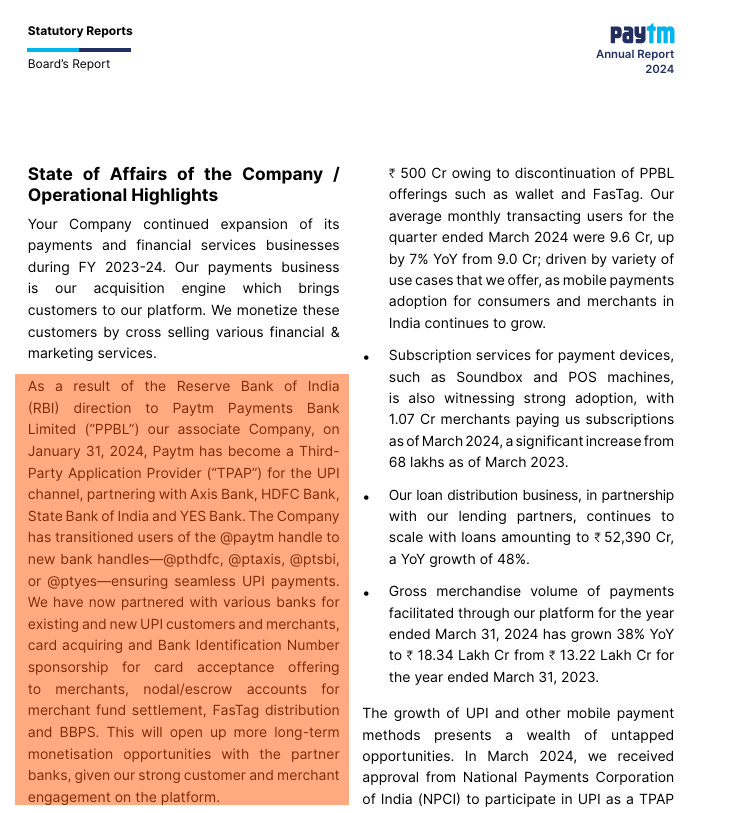

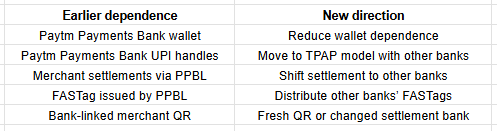

This was a severe business restriction. It did not shut down Paytm, the app, but it damaged the bank-linked part of the Paytm ecosystem. Paytm had no option but to move UPI, merchant settlement, nodal/escrow, FASTag distribution, BBPS arrangements to other banking partners and rebuild around other banks, including nodal/escrow accounts for merchant settlement, FASTag distribution of other banks, BBPS, and continue a payment-led ecosystem with financial services distribution.

13. Unbundling phase, Paytm separates the app from the bank

After the 2024 restrictions, Paytm had to rapidly reduce its dependence on Paytm Payments Bank. This was not just cosmetic. It had to rewire several operational rails. The important rails looked like this.

RBI’s FAQ specifically clarified that merchants using Paytm QR, Soundbox, or POS linked to another bank account could continue using that arrangement after March 15, 2024. But merchants linked to Paytm Payments Bank accounts or wallets could not receive credits after the deadline, except for permitted items like refunds or interest. This was the operational heart of the unbundling. Paytm had to preserve the merchant front end while replacing the banking back-end.

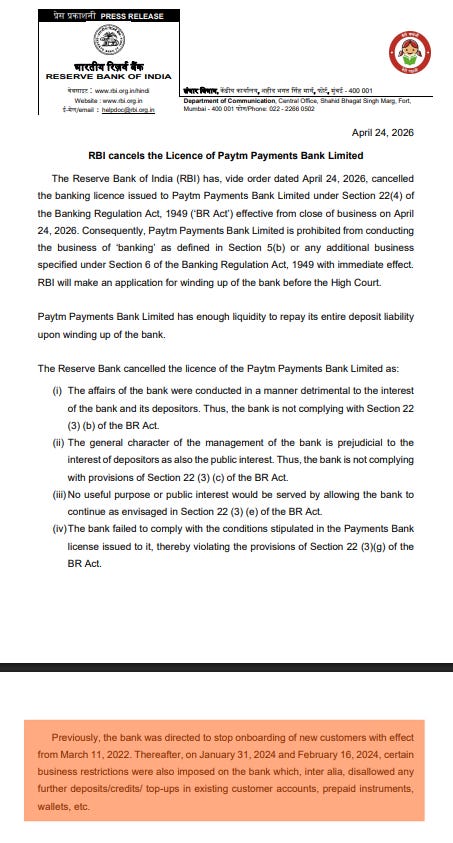

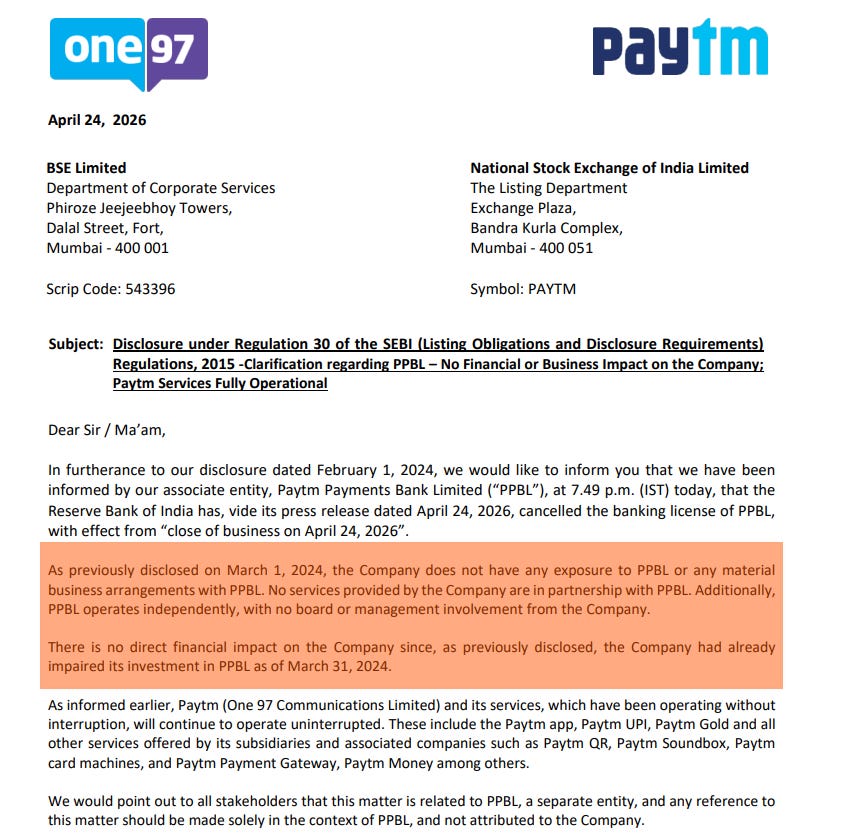

14. Licence cancellation phase, the final regulatory closure

On April 24, 2026, the RBI cancelled the banking licence of Paytm Payments Bank. The official RBI release said the bank had previously been barred from onboarding new customers from March 11, 2022, and later faced business restrictions in January and February 2024. The cancellation meant the bank was prohibited from carrying on banking business.

For business analysis, the cancellation is symbolically very important but operationally less disruptive than the January 2024 restrictions. The real business shock happened when deposits, wallet top ups, and bank-linked flows were stopped. The 2026 cancellation was the regulatory end state of a bank that had already become largely unusable for growth. Here’s what Paytm management had to say:

If I have to summarize all 14 phases into one neat template, this is how I would probably put it.

Paytm started as a telecom VAS company because that was where India’s mobile consumer activity was. It became a recharge app because prepaid mobile recharge was a high-frequency digital use case. It became a wallet because stored value improved convenience and lock-in. It became a demonetisation winner because it already had the wallet, brand, and QR rails when cash suddenly became scarce. It became a merchant QR network because payments needed offline acceptance. It created a payments bank to own more of the financial infrastructure, but that increased regulatory complexity. It built Soundbox because pure payments were low margin, and merchants needed trust. It built lending distribution because payment data and merchant relationships could be monetised better through credit. Finally, after RBI action on Paytm Payments Bank, Paytm had to unbundle its technology platform from its banking associate and rebuild around third-party banking partners.

Paytm of Today

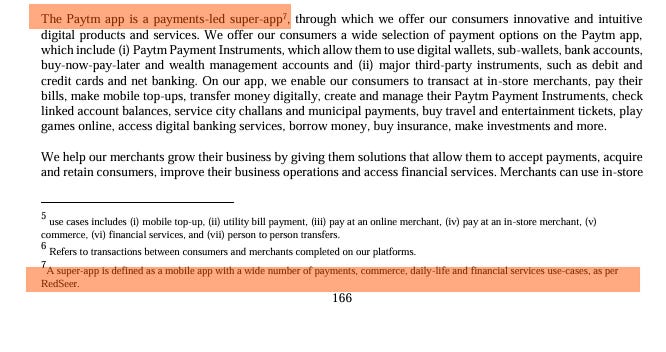

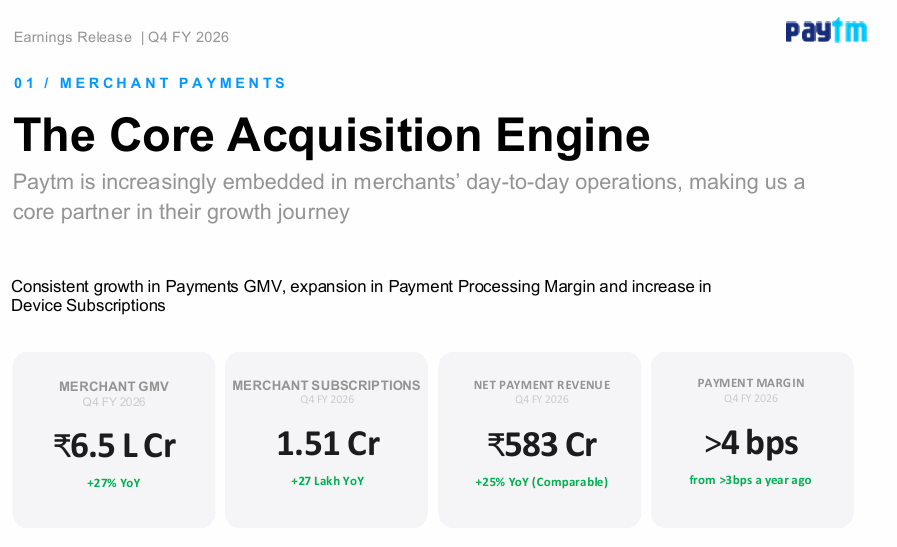

Paytm today is positioning itself not as a payments app or a UPI company, but as a profitable merchant distribution platform built on top of India’s payments infrastructure.

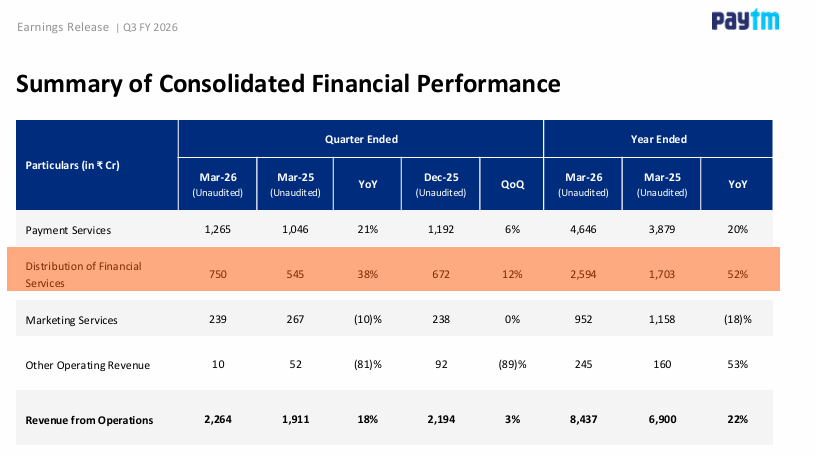

Management believes the business has now crossed from a “scale-first” phase into a phase of “profitable compounding,” reflected in FY26 EBITDA improving from a loss of ₹1,506 crore to a profit of ₹502 crore and PAT turning positive at ₹552 crore. The company’s strategy is now centered around four engines, merchant payments as the acquisition layer, merchant loan distribution as the monetization layer, consumer lifecycle monetization, and AI-led operating leverage. The merchant ecosystem has become the core moat, with 1.51 crore subscription merchants and merchant GMV of ₹6.5 lakh crore, while improving payment margins above 4 bps suggest Paytm is increasingly benefiting from higher-quality monetizable flows such as credit card-on-UPI and EMI-based transactions. Financial services distribution, especially merchant lending, is emerging as the highest-quality growth engine, with FY26 distribution revenue growing 52% YoY to ₹2,593 crore, while management repeatedly emphasizes that Paytm wants to remain an asset-light “distribution-only” platform rather than take balance-sheet risk itself. AI is now becoming central to the operating model through fraud prevention, onboarding, collections, personalization, and productivity tools, helping contribute to profit growth faster than indirect costs. The current Paytm model is, payments acquire merchants and consumers, merchant relationships create distribution infrastructure, financial services monetize the ecosystem, and AI expands operating leverage.

Say: Do Ratio: Improving, But Not Clean

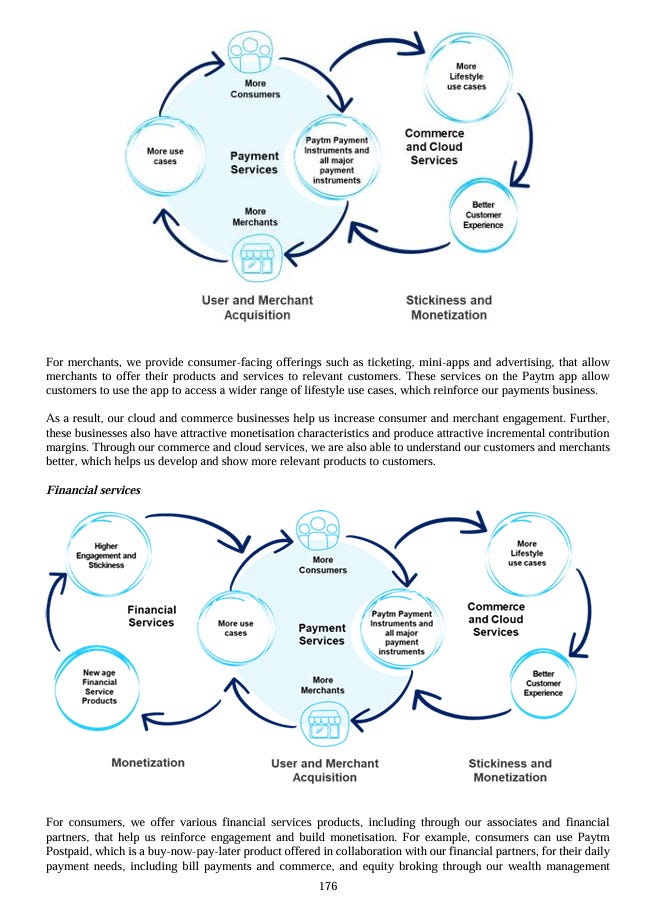

Paytm’s story becomes easier to understand when viewed through the lens of what management kept saying versus what the business eventually became. Despite the volatility, valuation collapse, and regulatory shocks, the core architecture management originally described has actually survived, though in a far simpler and more disciplined form. Before listing, Paytm never positioned itself as just a payments company. Management consistently described it as a two-sided ecosystem with consumers on one side using recharge, wallet, UPI, FASTag, and commerce, and merchants on the other side using QR codes, Soundbox, payment gateway, POS devices, and financial products. The central thesis was always that payments were merely the acquisition layer, while monetization would eventually come through merchant subscriptions, lending distribution, and financial services. In hindsight, this foundational thinking was largely correct.

During the IPO phase, Paytm was attempting to build multiple businesses simultaneously, including payments, wallet, commerce, cloud services, mini apps, ticketing, banking, lending distribution, and broader financial services. The DRHP itself reflected this ecosystem breadth. However, while investors could clearly see scale and user engagement, there were growing questions around monetization clarity, profitability, and the sustainability of the business model. Reuters described Paytm as a “payments-centred financial super-app” at the time of listing, while several IPO analyses and case studies highlighted the lack of a clear profitability narrative despite the company’s massive scale.

One of the strongest parts of Paytm’s journey has been merchant monetization. Initially, QR codes acted largely as merchant acquisition infrastructure. But once UPI commoditized basic payment flows, Paytm realized it needed a stronger monetization layer. That layer became Soundbox and merchant subscriptions. Over time, Soundbox evolved from a payment confirmation device into what management now calls a “small business operating system.” Subscription merchants reached 1.51 crore by Q4FY26, merchant GMV touched ₹6.5 lakh crore, and payment processing margins improved from roughly 3 basis points to above 4 basis points, helped by higher contribution from EMI products and credit card-on-UPI transactions. Merchant lending is another area where execution has broadly matched the original thesis. Paytm always believed merchant payment data could eventually support loan distribution. Today, management openly positions merchant loans as a high-margin, scalable business, while emphasizing that Paytm itself does not take balance-sheet risk. Banks and NBFCs underwrite the loans, while Paytm acts as the distribution and technology layer. The biggest negative in the whole journey remains Paytm Payments Bank. Originally, PPBL was meant to become the banking spine of the ecosystem. Instead, RBI restrictions forced Paytm to unbundle the business. Ironically, this simplification may have improved the quality of the company. Paytm moved from trying to own a regulated banking infrastructure to becoming an asset-light distribution and software layer sitting above financial institutions. Another important improvement has been disclosure quality and KPI discipline. Earlier, Paytm's communication focused heavily on vanity metrics such as registered users and adjusted profitability. Over time, management shifted toward monetizable KPIs such as subscription merchants, contribution margins, and operating leverage.

That operating leverage is finally visible. FY26 revenue reached ₹8,437 crore, EBITDA turned positive at ₹502 crore, and PAT stood at ₹552 crore, compared to EBITDA losses of more than ₹1,500 crore a year earlier. The language from management has also changed. The earlier Paytm spoke about blitzscaling. The current Paytm speaks about disciplined compounding, AI-led operating leverage, and profitability discipline.

To summarize, Paytm today is this. Payments acquire merchants. Devices retain them. Financial services monetize them. And AI expands operating leverage.

The management deserves credit for surviving the PPBL shock and rebuilding Paytm into a profitable platform business. But the PPBL episode also remains a reminder that aggressive ecosystem building without equally strong governance and regulatory execution can become extremely costly.

Payments: Merchants | Devices: Retention | Financial Services: Monetization | Monetization through Financial Services: An uncertain, unevolved frontier

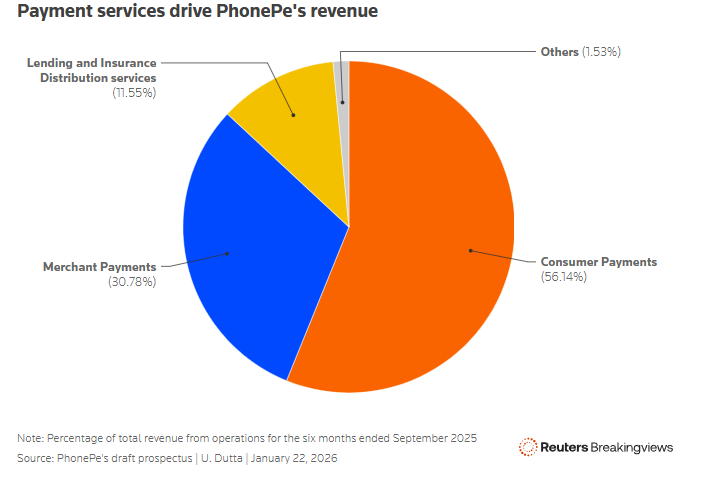

Unlike the early years of UPI, where investors feared that payments would remain a zero-monetization business forever, the evolution of PhonePe and Google Pay has shown that payments is not the end product, but the customer acquisition layer for financial services distribution. The real value lies in owning user behaviour, transaction frequency, merchant relationships, and data. Once these platforms achieved scale and habit formation, they slowly started cross-selling higher-margin financial products such as personal loans, merchant loans, insurance, credit products, wealth offerings, and co-branded financial services. PhonePe today has meaningfully expanded beyond payments into insurance distribution, mutual funds, lending partnerships, and merchant financial services.

Google Pay has similarly deepened its financial ecosystem through lending partnerships, bill payments, merchant commerce, and consumer financial products. Importantly, both companies spent years prioritizing distribution scale and ecosystem depth before meaningful monetization became visible. This is a critical point because digital financial businesses often look optically weak during the land-grab phase while the underlying behavioural moat quietly strengthens underneath.

This becomes highly relevant while evaluating Paytm today. Despite the regulatory setbacks and temporary disruption in merchant sentiment, Paytm still retains one of the largest merchant distribution networks and consumer payment ecosystems in India. The broader industry evidence from PhonePe and Google Pay suggests that once transaction behaviour and merchant relationships become deeply embedded, monetization through financial services tends to improve structurally over time. In that context, the market may currently be underestimating the long-term earnings potential embedded within Paytm’s distribution layer.

Distribution Vs Trust

Distribution and trust are not necessarily the same thing. Platforms like Paytm, PhonePe, and Google Pay may control transaction behaviour and customer attention, but long-term financial products such as loans, insurance, and investments ultimately depend far more on trust than convenience. Let’s look at how a financial product is being sold on these Apps.

The customer typically enters Paytm or PhonePe through a high-frequency payment use case such as UPI, recharge, bill payment, FASTag, QR payment, wallet, or merchant payment. Over time, this creates transaction history, behavioural data, and app engagement. Based on spending patterns, transaction frequency, merchant activity, credit profile, location, or stated interests, the platform starts showing relevant financial products such as personal loans, merchant loans, insurance, mutual funds, gold, credit cards, or Postpaid. Once the customer clicks on a product, the app acts as a distributor or marketplace by presenting one or more partner offerings. The customer then completes KYC, consent, bureau checks, bank verification, mandate setup, or other regulatory requirements, depending on the product category. The actual product is usually issued or underwritten by a partner institution, such as a bank or NBFC for loans, an insurer for insurance, an AMC for mutual funds, or a broking partner for investments. Paytm or PhonePe earns distribution income through commissions, sourcing fees, servicing fees, trail income, brokerage, or subscription fees. Even after the sale, the servicing layer often remains inside the same app, allowing customers to repay EMIs, track investments, renew policies, redeem mutual funds, or manage financial products directly through the platform.

A customer may comfortably use a payments app daily for UPI transactions, but that does not automatically mean they will trust the same platform with their savings, insurance claims, or large-ticket financial decisions. In many cases, the real trust may still sit with the underlying bank, insurer, AMC, or broker, while the payments app merely controls the interface and distribution layer. Payments’ behaviour is habit-driven, and switching costs are low, whereas financial trust compounds slowly through governance, balance-sheet strength, claims experience, and regulatory credibility. The key risk, therefore, is that payments platforms may eventually become high-volume distributors with limited pricing power, while the deeper and more durable economics continue to accrue to the regulated financial institutions that actually own customer trust.

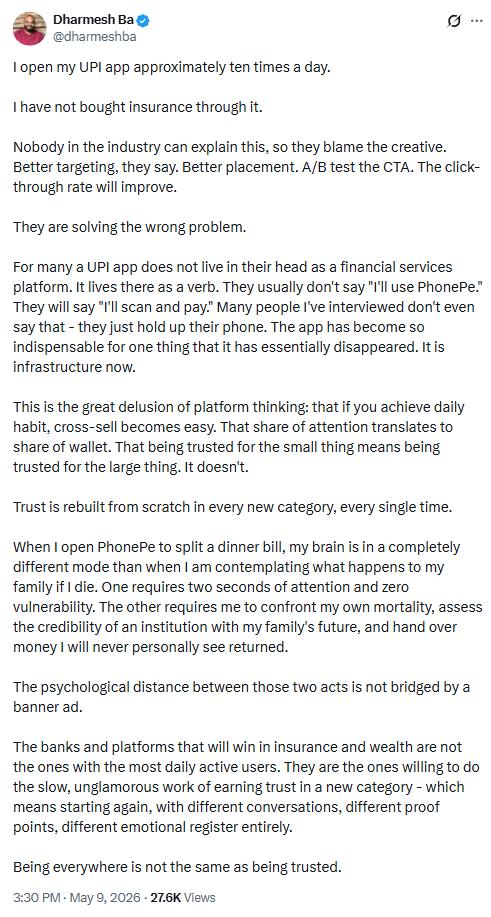

This tweet below made me think harder.

I do not know Dharmesh personally. I have been reading his India Notes Newsletter for the past few months. Highly recommend them to you. I have immensely benefited from them.

Time will tell who is right. Paytm and Phone Pay? Or Dharmesh?

Final Thoughts

At the beginning of this note, we discussed how power shifts across business eras. In the industrial age, manufacturing held power because production was scarce, difficult, and capital-intensive. The internet changed that equation by making products abundant and shifting scarcity toward attention, discovery, and distribution. That is precisely why platforms like Paytm, PhonePe, Amazon, Swiggy, or Urban Company can scale so rapidly once they become embedded in consumer behaviour.

But there is an important nuance here. Distribution and trust are not always the same thing.

Take the example of Urban Company. A new hairstylist joins the platform and immediately benefits from the distribution engine. The platform brings discovery, customer flow, payments, scheduling, and trust transfer. Over time, however, the hairstylist starts building direct relationships with customers. Eventually, many aspire to open their own salon or operate independently. The platform continues to attract fresh supply, while experienced professionals slowly graduate outside the ecosystem. In a way, the system still works for everyone. Customers get convenience. New service providers get steady work. The platform earns its share. But over long periods, truly skilled professionals tend to accumulate their own pricing power because specialized trust compounds differently from distribution.

The same idea applies to plumbers as well. A specialized resource/skill may become structurally more valuable in the coming decades because demand rises faster than quality supply. A good plumber is not just a transactional worker. He becomes a trusted problem solver. Once customers trust his quality of work, reliability, and judgment, pricing power slowly shifts toward the skilled professional himself. The platform may still control distribution, but trust increasingly sits with the underlying expert. Speaking of plumbing, it reminds me of my recent blog on India’s financial plumbing.

Financial services may eventually evolve in a somewhat similar way. Payment apps can acquire users at an extraordinary scale because payments are high-frequency and habit-driven. But loans, investments, wealth products, and insurance are not impulse decisions in the same way. People pause longer before trusting someone with savings, credit, or long-duration financial decisions. That trust often sits with the underlying institution, the bank, insurer, AMC, or lender, rather than the distribution layer alone.

This does not mean platforms like Paytm cannot become extremely large businesses. In fact, they may become far larger than what most people currently imagine because distribution itself has become one of the most valuable assets in the digital economy. But it does suggest that the real battle ahead may not simply be about acquiring users or merchants. It may increasingly become a battle around trust, underwriting quality, governance, compliance, and long-term financial credibility.

And perhaps that is what makes Paytm such an interesting business. Over two and a half decades, the company has survived multiple pivots, telecom VAS, recharge app, wallet, demonetisation beneficiary, QR network, payments bank, lending distributor, and now a merchant-focused financial distribution platform with AI-led operating leverage. Whether one agrees with the vision or not, the business continues to adapt with every shift in the ecosystem.

As investors, we may like Paytm or dislike Paytm. We may agree with management or question it. But after studying the journey deeply, can you ignore it?

Thanks for reading!

SEBI RIA Disclosure: No holding, no recommendation

P.S. Know more about Zen Nivesh: Focus on Microcaps

[1] Zen Investing Club [ZNIC]: How to invest

[2] Zen Nivesh Advisory Service [ZNAS]: What to invest in

[3] Zen Nivesh Portfolio Advisory [ZNPA] What, How, When, & Where

[4] Zen Nivesh Waitlist WhatsApp Group

| A guest post by

|

Amazing read!

Let’s support each other and grow together so let’s subscribe each other if you are new on substack like me