RBI’s Dividend Deluge: Are You Ready?

Why a Historic Dividend May Quietly Reignite India’s Growth Engine

A record dividend transfer of ₹2.69 lakh crore or $32 billion from the Reserve Bank of India to the Government of India was just announced last week.. It marks a ~27% jump over last year’s ₹2.1 lakh crore payout - making it the highest-ever surplus transfer by the central bank.

Note:As per the RBI Act, once the Reserve Bank sets aside funds for bad loans, asset depreciation, employee benefits, and other essential expenses, the remaining surplus is handed over to the government.

The move, which exceeded the previous year's ₹2.1 lakh crore transfer by 27.4%, however, fell short of market expectations primarily due to the central bank's decision to strengthen its risk provisioning framework rather than maximize fiscal transfers

In a clear signal of increased caution, the RBI has raised its Contingent Risk Buffer (CRB) to 7.5%, the upper limit of its newly expanded range. This is a sharp increase from 6.5% in FY24 and 6% in FY23, indicating that the central bank sees elevated risks in both global and domestic environments. Let us understand it better.

But What Is the Contingency Risk Buffer, and Why the RBI Increased It?

Think of the Contingency Risk Buffer (CRB) as the RBI’s emergency fund - a financial cushion designed to protect the central bank from nasty surprises. Whether it's currency fluctuations, sudden losses in asset value, credit defaults, or a full-blown financial crisis, the CRB is there to ensure the RBI can continue doing its job without skipping a beat. It's like an insurance policy, but for the nation’s monetary stability.

This buffer is a core part of what’s called the Economic Capital Framework (ECF) - the RBI’s internal playbook for managing financial risks and deciding how much of its earnings it can safely transfer to the government.

However, on May 15, 2025, the RBI gave this framework a much-needed refresh. One of the key changes? It widened the CRB range. Earlier, the RBI kept this buffer between 5.5% and 6.5% of its balance sheet. Now, it has more room to manoeuvre - the range has been expanded to 4.5% to 7.5%.

This might seem technical, but it gives the RBI greater flexibility. When risks are rising - say, due to global uncertainty or financial stress - it can set aside more money. When things are calm, it can ease up. It’s a smarter, more dynamic approach to risk management.

This update also comes as part of a five-year review cycle built into the ECF - a process originally recommended by the Bimal Jalan Committee in 2019 to keep the RBI’s risk practices in step with the evolving economic landscape.

Here’s the part markets always watch closely: how much money the RBI gives to the government each year. That’s where the CRB calculation becomes crucial.

The RBI holds what’s called Available Realised Equity (ARE) - basically a mix of its capital, reserves, and provisions. If this pot of money exceeds the CRB requirement, the excess can be handed over to the government as a dividend.

But if the ARE falls short, the RBI focuses on rebuilding its buffers first, before transferring anything. So, when the RBI increases its CRB - like it just did - it’s signaling that safety comes first, even if it means lower payouts in the short term.

Bottomline is that the CRB is one of the most important (but often overlooked) tools in the RBI’s arsenal. By strengthening it now, the RBI is choosing long-term financial resilience over short-term fiscal cheer. It’s a prudent move in an increasingly uncertain world - and a reminder that sound central banking often means taking the cautious route, even when no one is watching.

But What’s Driving This Massive Surplus?

The Reserve Bank of India is poised to post a record surplus for FY25, and behind the headline number lies a story of smart manoeuvres, favourable macro conditions, and disciplined balance sheet management.

At the heart of this windfall is the RBI’s nimble handling of the foreign exchange market. Over the past year, it aggressively intervened to stabilise the rupee, selling nearly $371.6 billion in the forex market - more than twice the $153 billion it sold the year before. But this wasn’t just about market stability. It also proved to be a profitable trade. The central bank had accumulated dollars when the rupee was trading around ₹83–84 and later sold them at higher levels - between ₹84–87 - capturing meaningful gains from currency fluctuations. This classic “buy low, sell high” strategy, executed with precision and scale, delivered substantial returns.

At the same time, the RBI’s sizable forex reserves - now comfortably above $600 billion - are yielding stronger returns. With global interest rates, particularly in the US, holding steady at elevated levels, the interest income on these foreign assets, mainly US Treasuries, has jumped significantly. It's a quiet tailwind, akin to earning better returns on your fixed deposits when rates rise, but at a sovereign scale.

Back home, the central bank’s Open Market Operations (OMOs) also contributed steadily to its earnings. Its rupee asset base, particularly government securities, has grown to ₹15.6 trillion.

Source: Hindustan Times

While falling yields may have trimmed mark-to-market gains, the interest income on these bonds remained robust. Meanwhile, lending to banks through repo operations - under its open market operations framework - continued to generate stable and recurring revenue.

But it wasn’t just about what the RBI earned. It was also about what it didn’t spend. The central bank has become more efficient in recent years, thanks to greater digitisation and tighter cost controls. This operational discipline ensured that more of its earnings flowed directly to the bottom line.

Put together, these elements created the perfect conditions for a record surplus. The RBI stabilised the rupee, capitalised on global interest rate trends, managed a growing portfolio of domestic assets, and kept its own house in order.

It has to be said that in a year marked by global uncertainties, the central bank managed to walk a fine line between caution and opportunism.

So What Happens When This Liquidity Bomb Hits the System?

While the RBI’s dividend transfer to the central government is fundamentally a fiscal exercise, it carries important monetary implications. Initially, the transfer is a mere balance sheet adjustment between the RBI and the Centre. However, the real impact on banking system liquidity unfolds when the government begins spending this surplus. As funds are deployed toward salaries, subsidies, infrastructure projects, and welfare schemes, the money flows from the government’s account at the RBI into the broader financial system, landing in commercial bank accounts. This infusion increases deposit levels and adds to banking system liquidity, potentially flipping the system from a liquidity deficit to a surplus.

Moreover, a large one-time dividend reduces the government’s need to borrow from the market to meet its expenditure commitments. With a stronger cash position, the Centre can scale down its scheduled bond issuances, improving the demand-supply dynamics in the bond market. This often leads to softening yields, especially on longer-duration government securities. In turn, the combination of higher liquidity and lower borrowing pressure reinforces a dovish monetary environment, enhances credit availability, and can provide further tailwinds to rate-sensitive sectors across the economy.

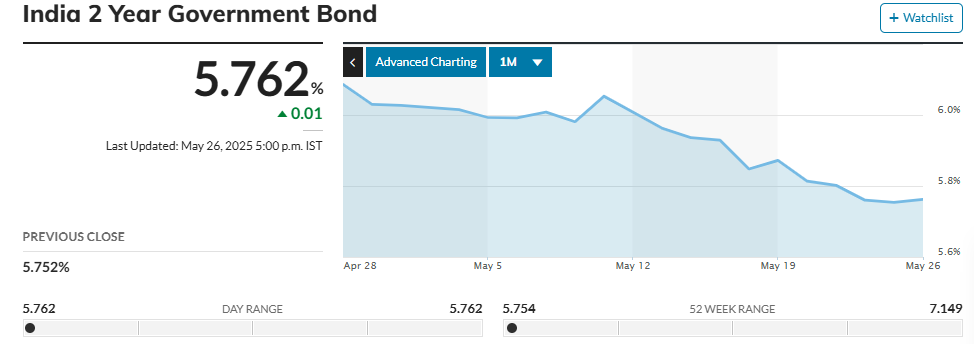

Essentially, with this move, banks will be in a better position to lend more, and bond yields - especially the 10-year ones - could fall even further, possibly below 6.20%.

Source: Market Watch 26.05.25

Further, the Short-term bond yields are falling more quickly than long-term ones, which is causing the yield curve to steepen. In simple terms, this means that investors expect interest rates to come down in the near future.

Source: Market Watch 26.05.25

The current macro-financial environment reflects a form of stealth monetary easing, where abundant surplus liquidity and declining bond yields are delivering the effects of a rate cut without any formal change to the policy repo rate.

Macro Implications: Quiet Stimulus, Loud Impact

While the ₹2.69 lakh crore dividend transfer from the RBI may have fallen short of the most optimistic projections, it still delivers a powerful fiscal boost at a critical juncture. At nearly 0.7% of GDP, the surplus offers much-needed breathing room to the government, especially as it grapples with rising defence allocations, higher welfare spends, and the looming risk of trade-related disruptions, including potential tariffs from the US.

The figure comfortably exceeds the ₹2.56 lakh crore pencilled in by Finance Minister Nirmala Sitharaman in her Budget for FY26, which had accounted for dividends from both the RBI and state-run financial institutions. The surplus, therefore, not only outperforms expectations - it recalibrates the government’s fiscal math in its favour.

Economists estimate that this windfall could help narrow the fiscal deficit by as much as 20 basis points, potentially bringing it down to 4.2% of GDP - a welcome development for bond markets and rating agencies alike.

Source: Business Line

Alternatively, it opens up fiscal headroom of around ₹70,000 crore, which could be deployed toward defence, infrastructure, welfare schemes, or even as a buffer against global shocks. In an environment marked by geopolitical strain and uncertain trade flows, this will hold the Government in good stead.

Moreover, the ongoing softening of bond yields and narrowing fiscal deficit combined with improving banking system liquidity, is setting the stage for a sustained dovish bias in monetary policy. With headline inflation easing to around 3.1% - below March’s 3.3% - and core inflation remaining contained, the RBI may not need to formally cut rates to support growth; the liquidity-infused environment itself could serve as a powerful accommodative tool.

But interestingly, RBI delivered a dovish-cut last month and experts are expecting at least 3 more rate cuts as inflation dips below the 4% target.

This means - India’s elevated real interest rates, relative macro stability, and potentially multiple rate cuts create fertile ground for renewed foreign capital inflows. Portfolio investors are already turning net buyers of Indian G-Secs and Debt Securities, attracted by the improving yield curve dynamics and favorable risk-reward setup. As global carry trades revive,

India’s bond markets - both sovereign and corporate - could witness stronger inflows, reinforcing the liquidity cycle and further anchoring yields. This feedback loop has the potential to not only ease borrowing costs domestically but also elevate India's standing as a preferred emerging market investment destination.

How to Play the Liquidity Cycle?

The unfolding liquidity cycle - driven by the anticipated record RBI dividend and easing yield environment - is poised to create ripple effects across multiple sectors.

PSU banks are likely to benefit on two fronts: treasury gains from falling bond yields and a revival in credit demand as borrowing costs ease.

For NBFCs and housing finance companies, declining funding costs could significantly improve net interest margins, especially in segments like affordable housing.

Simultaneously, as discussed above, enhanced fiscal headroom from the government’s windfall gain may spur public capital expenditure, directly benefiting capital goods, infrastructure, and EPC players through a stronger order pipeline. In the consumption space, improved rural cash flows and cheaper loans may catalyze demand recovery across discretionary segments such as two-wheelers, white goods, and FMCG.

From an asset-class based investment strategy standpoint, fixed income investors might explore long-duration and gilt funds, which tend to perform well in a falling interest rate regime.

Overall, the liquidity boost sets a constructive backdrop across both cyclical sectors and rate-sensitive assets, creating a favorable environment for selective bottom-up stock picking and duration-led bond positioning.

Also, there’s an update!

We are starting onboarding to our premium services soon. Join the waitlist now.

| A guest post by

|

EDWIN CASTRO CHARITY HOME changed I and my family’s lives for good. Thank you so much for the work you do! I love your charity because it’s efficient, dedicated, honest, and it’s spiritually motivated, but doesn’t force one set of beliefs upon the recipients of your assistance.' I will continue to tell the world about your good work.