Unicommerce eSolutions: A Deep Dive

Same | Change | Complexity | ZN Research Lab-54

Every major consumer innovation appears to follow a broadly similar pattern. In its early years, the new idea was often dismissed because people evaluated it through the lens of existing consumer behavior.

Questions that naturally arise:

“Why would anyone buy books without touching them?”

“Why would anyone order groceries that arrive in ten minutes?”

“Why would anyone pay using a phone?”

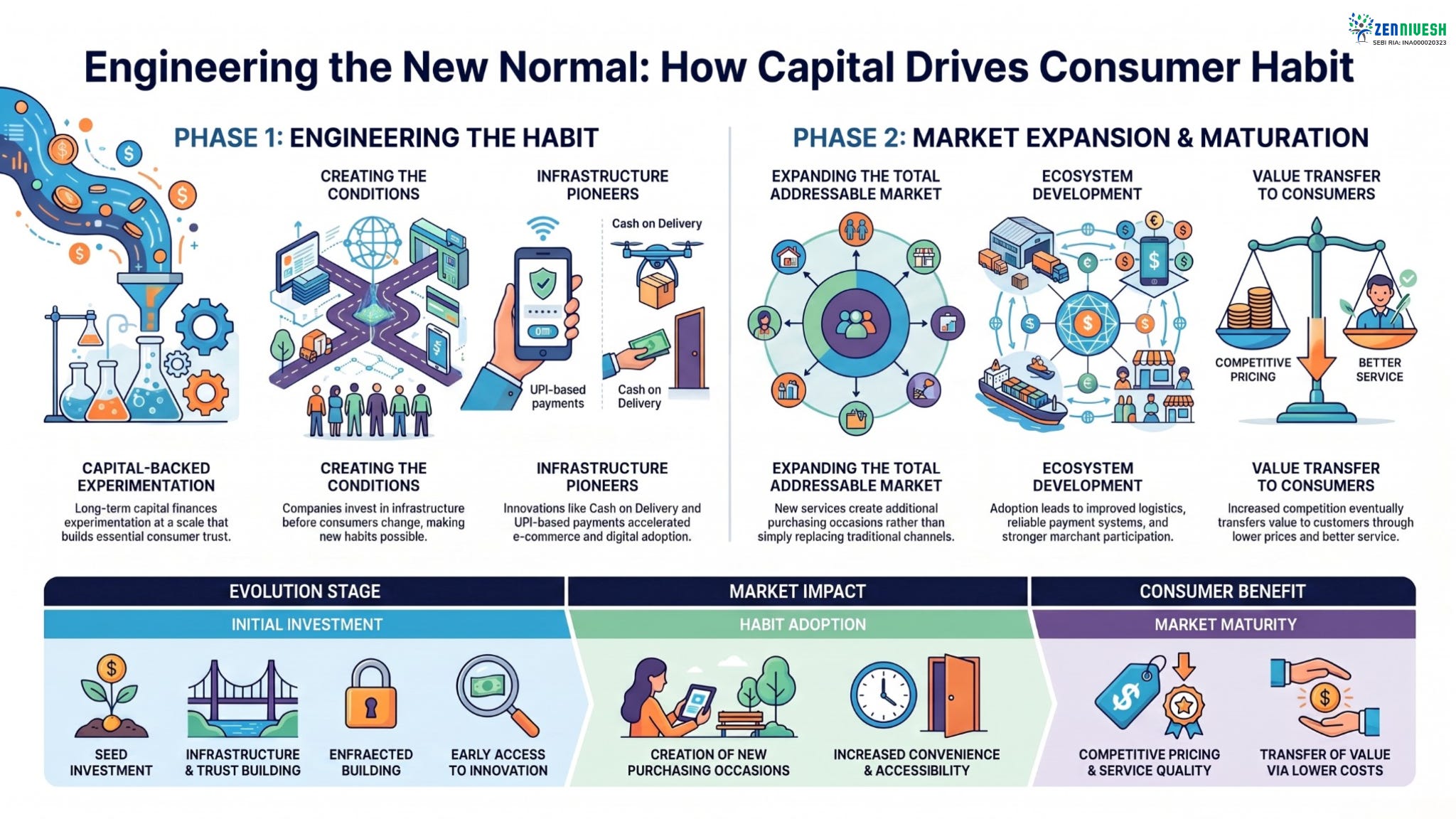

The assumption is that current habits are permanent. History suggests that this assumption is often incorrect. Consumer behavior evolves, although the pace and extent of that change are rarely obvious at the beginning. Venture capital has historically played an important role in enabling these behavioral shifts. It does much more than finance businesses; it finances experimentation at a scale that would otherwise be difficult to sustain. Amazon invested for years to build trust in online shopping. Companies like Flipkart & Snapdeal accelerated e-commerce adoption in India through innovations such as Cash on Delivery. Food delivery companies familiarised consumers with ordering prepared meals. UPI-based businesses accelerated the shift towards digital payments. Today, quick-commerce companies are investing heavily to make near-instant delivery part of everyday consumer behavior. In many cases, consumers do not change first. Companies, supported by long-term capital, invest in creating the conditions that encourage new habits to emerge.

As adoption increases, the supporting ecosystem also develops. Logistics networks improve, payment infrastructure becomes more reliable, technology advances, merchant participation expands, and customer trust strengthens. Services that initially appear niche or unnecessary gradually become part of everyday life. Looking back, the transition often appears inevitable, although it rarely feels that way while it is taking place.

At this stage, the market itself frequently expands. E-commerce did not simply shift purchases from offline to online channels; it increased the overall accessibility and frequency of retail transactions. Quick commerce is demonstrating similar characteristics by creating new purchasing occasions rather than merely replacing traditional grocery shopping. Greater convenience often leads consumers to buy differently, not just through a different channel. As a result, the total addressable market can become substantially larger than originally anticipated.

However, a larger market does not necessarily translate into superior economics for every participant. Once consumer behavior changes and the opportunity becomes evident, competition increases. More companies enter the market, pricing becomes more competitive, service quality improves, and convenience continues to rise. Consumers benefit significantly from this process. In many industries, a meaningful share of the value created is ultimately transferred to customers through lower prices, faster delivery, and better service.

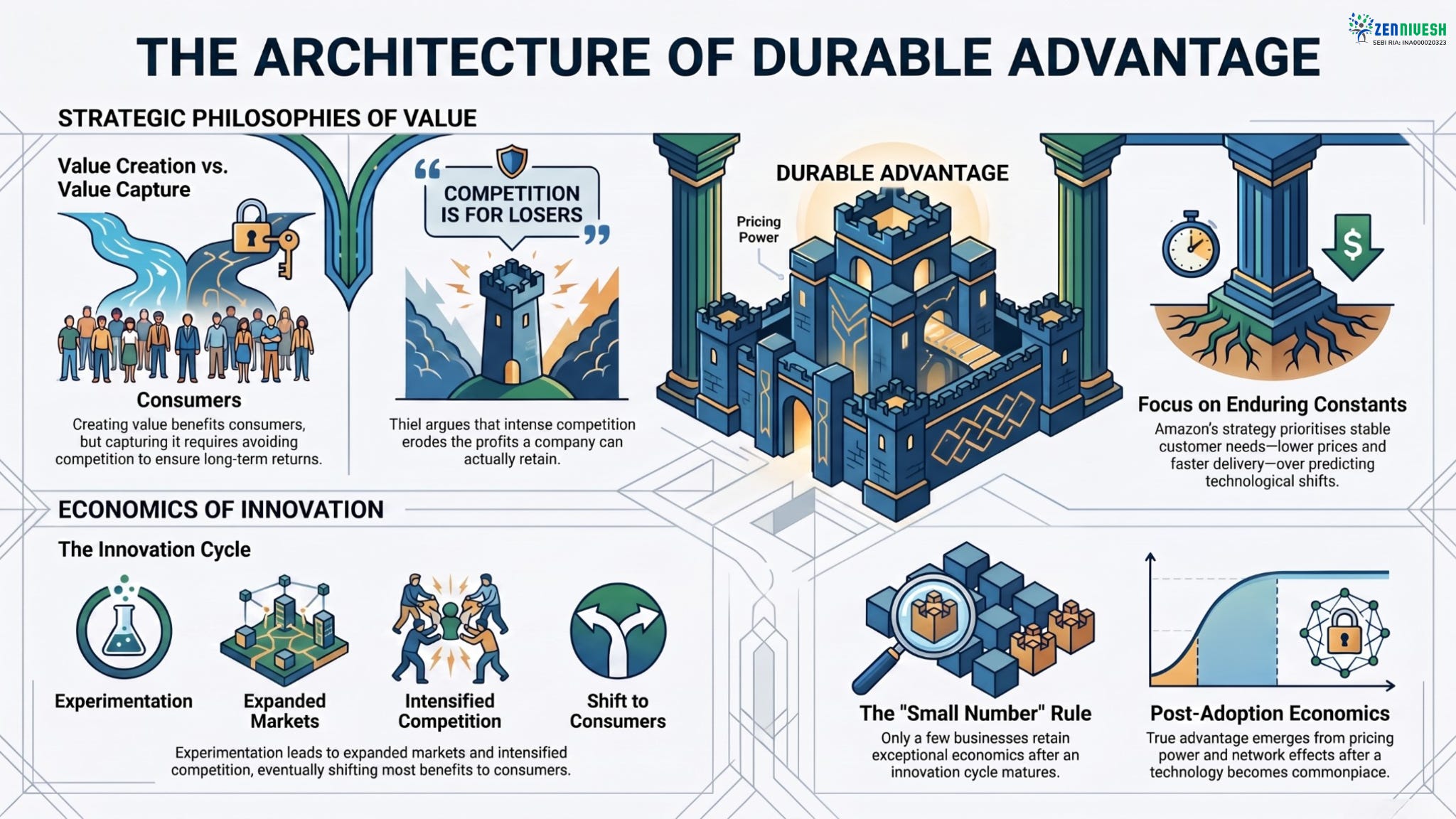

This distinction between creating value and capturing value is central to Peter Thiel's investment philosophy. A company may contribute significantly to the development of an industry while earning only modest economic returns. His observation that “competition is for losers” is best understood in this context. Competition generally produces better outcomes for consumers, but it often reduces long-term returns for businesses. The companies that generate exceptional shareholder returns are typically those that continue to retain a meaningful share of the value they create even after an industry matures.

Jeff Bezos approaches the same question from a different perspective. He has often remarked that people spend considerable time asking what will change over the next decade, while paying much less attention to what will remain unchanged. For Amazon, the enduring constants were straightforward: customers would continue to prefer lower prices, faster delivery, and wider selection. While technology evolves continuously, these fundamental customer preferences remain remarkably stable. Amazon’s long-term strategy was built around strengthening these constants rather than predicting every technological change.

From an investment perspective, this shifts the focus from technology itself to the economics that emerge after technology becomes widely adopted. New technologies frequently create substantial opportunities, but the more important question is which businesses will continue to retain pricing power, customer loyalty, network effects, cost advantages, or other durable competitive strengths once the innovation becomes commonplace.

The same broad pattern is likely to continue as new technologies emerge. Artificial intelligence, autonomous delivery, conversational commerce, robotics, and other future innovations will each undergo their own adoption cycles. Some ideas will fail, while others will reshape consumer behavior. Venture capital will continue funding experimentation, markets will expand as adoption increases, and competition will gradually intensify. Consumers are likely to receive a significant share of the benefits created by these innovations. Only a relatively small number of businesses will retain exceptional economics over the long term.

Therefore, for you and me, the primary question is not whether a new technology will succeed. A more useful question is whether the businesses that enable that technology will continue to capture an attractive share of the value they create once the market becomes competitive. This is where Peter Thiel’s distinction between value creation and value capture aligns closely with Jeff Bezos’ emphasis on building around customer needs that do not change. Together, they provide a useful framework for evaluating long-term businesses in industries shaped by continuous innovation.

Unicommerce is an interesting business to study through this framework because it is one step away from the consumer experience. You and I rarely think about what happens after clicking the “Buy Now” button. Yet that single click triggers a surprisingly complex chain of operational decisions. Inventory has to be checked across multiple warehouses and stores. The optimal fulfillment location has to be selected. Orders have to be synchronized across marketplaces, brand websites, offline stores, and increasingly quick-commerce channels. Courier partners have to be allocated. Returns, cancellations, and payment reconciliations have to be managed accurately. As digital commerce evolves, these workflows become increasingly complex.

Over the last decade, Indian commerce has gone through precisely this evolution. It began with marketplace-led selling. Brands gradually realized they could build direct relationships with consumers through their own websites. Omnichannel retail blurred the distinction between online and offline inventories. Quick commerce compressed delivery timelines from days to minutes. Today, artificial intelligence is beginning to automate decisions across the entire commerce workflow. With every phase, the operational complexity increased.

Rather than trying to predict which marketplace, retail format, or consumer brand would ultimately dominate, Unicommerce quietly focused on building the software infrastructure required to support all of them. The company did not attempt to create consumer demand. The heavy lifting of changing consumer behavior was largely undertaken by marketplaces, brands, and venture-funded businesses. Instead, Unicommerce positioned itself to benefit from the growing complexity that inevitably followed those behavioral shifts.

Its own journey closely mirrors the evolution of Indian e-commerce. It began with a multi-channel Order Management System that helped sellers manage inventory and orders across marketplaces. As brands increasingly started selling directly to consumers, the company expanded into Warehouse Management Systems. As online and offline retail converged, it built omnichannel retail capabilities. As financial leakages became more visible, it introduced reconciliation products. As B2B commerce, quick commerce, and logistics became increasingly important, the platform broadened further. More recently, the acquisitions of Shipway and ConvertWay extended the company’s presence into courier aggregation, shipping automation, and customer engagement, while artificial intelligence is now being embedded across multiple workflows. Seen over a decade rather than a few quarters, the company’s product roadmap has largely followed the increasing complexity of digital commerce rather than chasing short-term technology trends.

Against this backdrop, Unicommerce should be evaluated. The central investment question is not whether Indian e-commerce will continue to grow. That appears increasingly likely. The more important question is whether Unicommerce can continue to remain an indispensable layer of commerce infrastructure while retaining attractive economics as the ecosystem matures. In many ways, that is the same question Peter Thiel asks about value capture and the same question Jeff Bezos answers by focusing on what remains unchanged. The remainder of this piece attempts to evaluate Unicommerce through exactly that lens.

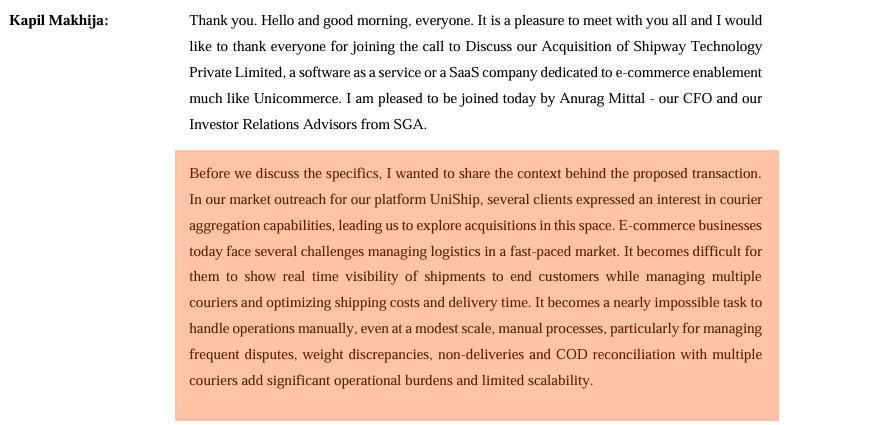

Unicommerce is best understood not as a conventional SaaS company, but as a commerce infrastructure company that has evolved with Indian e-commerce. It began in 2012 as a software layer for sellers managing orders and inventory across marketplaces. Its core platform, Uniware, is a cloud-native, multi-tenant SaaS platform with products across order management, warehouse management, omnichannel retail management, seller management, shipping, and reconciliation. The IPO was an offer for sale only, with no fresh capital coming into the company, so the listed journey began with an already profitable, cash-generating operating business rather than a capital-raising story.

A side note:

A new-age high-tech start-up doing a 100% OFS is a good thing. That means the company doesn’t need funds to operate. IPO was just an exit vehicle for early investors. Yes, valuation may not make sense. Fair point. So, wait for it to come to a sensible level. But do not believe in the unnecessary garbage thrown on social media. If you are buying an obscenely priced IPO, that’s your own problem, not anybody else’s.

Let’s get back to Unicommerce. The early journey of Unicommerce had two phases. The company was founded in 2012, was acquired by the AceVector/Snapdeal ecosystem in FY15–16, and Kapil Makhija joined around the same time. Promoters Kunal Bahl and Rohit Bansal brought Unicommerce into the AceVector ecosystem to make the marketplace business more efficient, but it soon became clear that it was solving a much larger problem: creating the technology backbone for brands and businesses in the digital era. Their own phrase is useful to retain:

“Unicommerce moved “from a product into a platform, and from a platform into the de facto operating system of Indian e-commerce.”

The company’s DNA can be explained through three operating principles: resilience, a tech-first mindset, and frugality/ROI discipline. The resilience was tested between 2017 and 2019, when competitors were pursuing more customized implementations, and Unicommerce chose to build a WMS platform instead. Sales were slower, but the company stayed with the architecture. When the pandemic accelerated e-commerce adoption, the platform’s stability became a driver of word-of-mouth growth. Same with omnichannel: the company built the product before the market was ready, saw limited traction for almost 18 months, and then saw adoption improve when Covid made omnichannel a practical necessity.

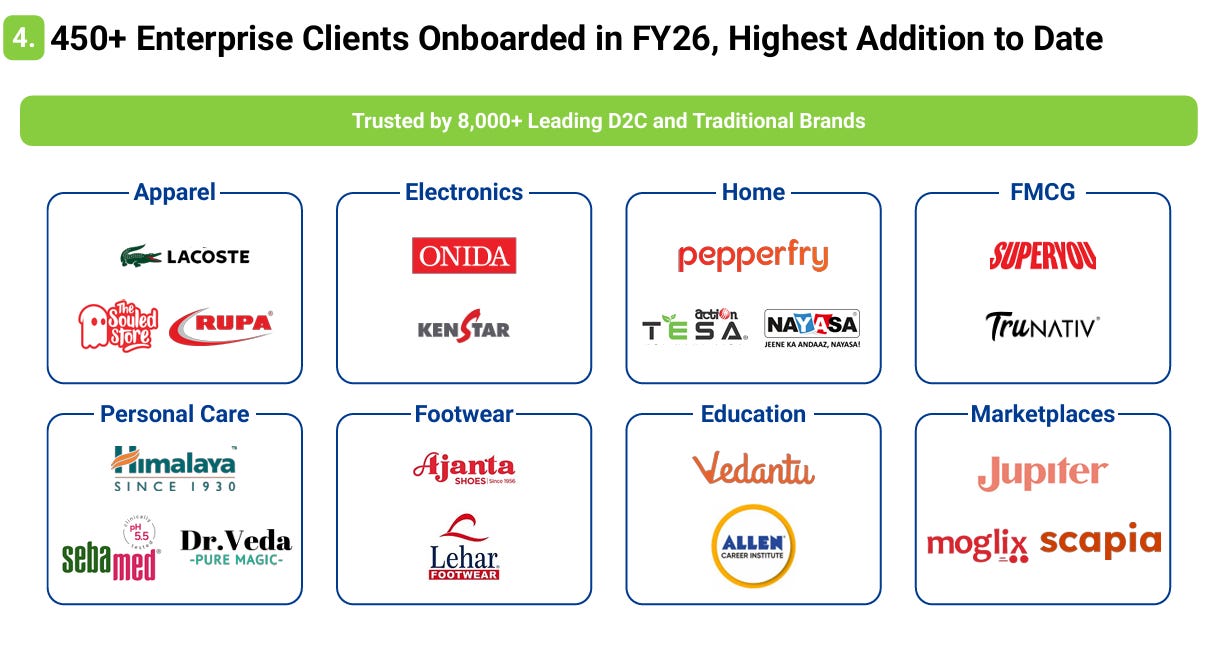

This is important to note because Unicommerce’s product evolution has generally kept pace with the complexity of its customers. The original multichannel order management system helped sellers manage orders and inventory across marketplaces. As brands began selling directly online after 2017, Unicommerce built an e-commerce-first WMS. As offline and online channels merged, it built Omni-RMS. As reconciliation leakages became visible, it launched UniReco. As B2B and quick commerce emerged, the platform added new workflows. By FY26, the company reported that 35–40% of enterprise clients were already using B2B and quick-commerce capabilities, and Uniware had onboarded 450+ enterprise clients during the year, the highest in its history.

The business model is attractive because the core Uniware engine is sticky, usage-linked, and high-margin. Enterprise clients pay minimum commitments based on bundled transaction volumes and then incur additional usage charges. This explains why transaction growth does not always translate linearly into revenue growth: new customers’ volumes can initially be absorbed inside minimum guarantees. Management has reiterated four growth levers for Uniware: market growth, new client additions, new products/cross-sell, and international expansion. It also clarified that transaction growth alone is not enough to infer revenue growth, because pricing and minimum guarantees matter.

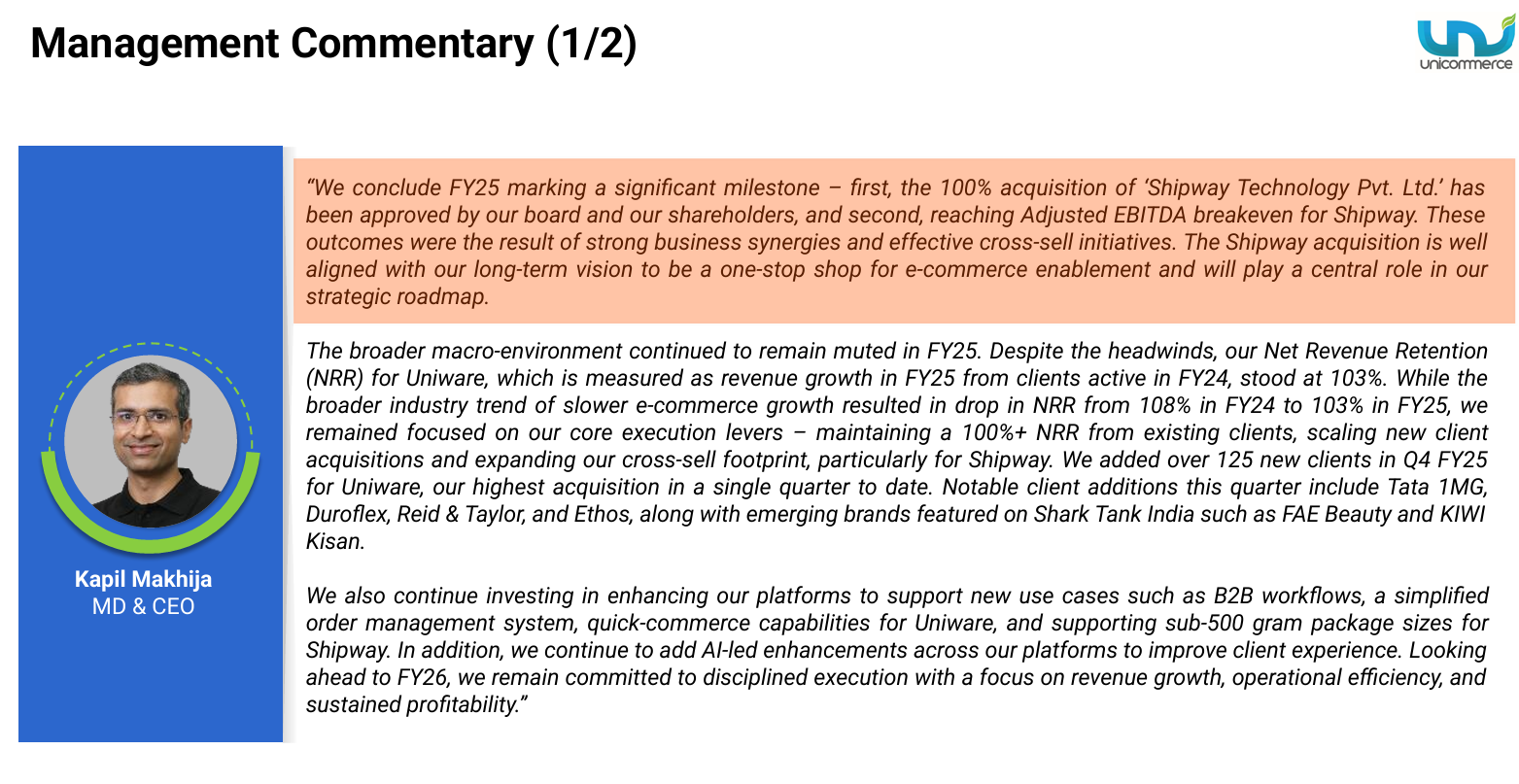

The first listed-year story was steady execution. FY25 revenue grew 30.1% YoY to ₹1,347.9 million, adjusted EBITDA grew 56.3% YoY to ₹283.9 million, PAT grew 34.3% YoY to ₹176.2 million, and cash flow from operations increased to ₹279.6 million. The company ended FY25 with Uniware annual transaction run-rate close to 1 billion order items, 12,330+ warehouse/store facilities, and 7,000+ clients across Uniware, Shipway and ConvertWay.

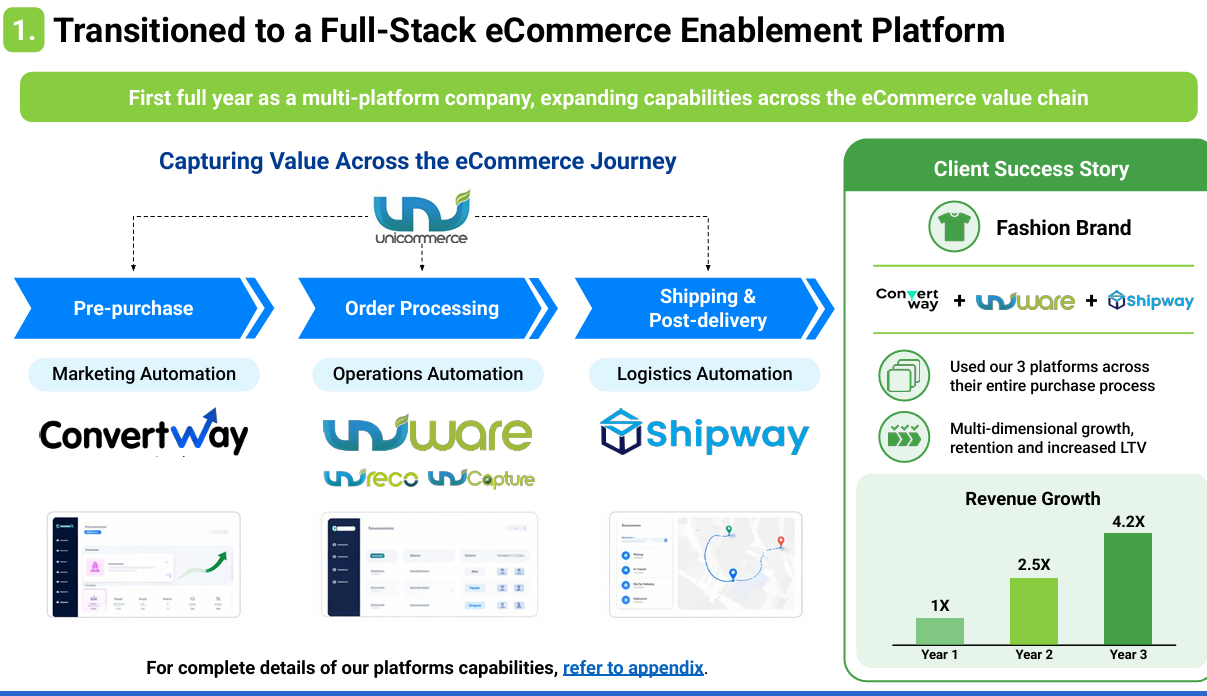

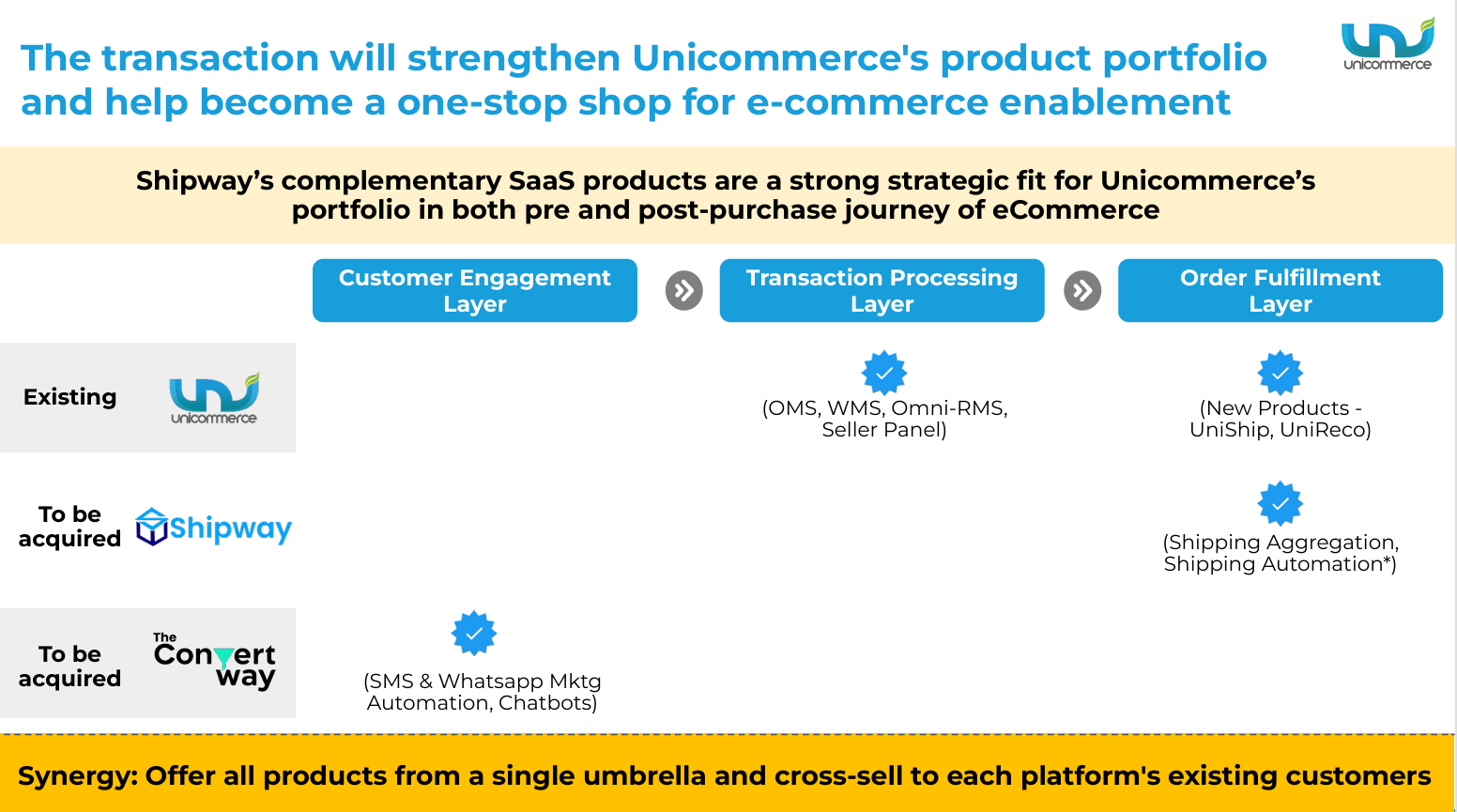

The most important strategic shift after listing was the Shipway acquisition. Publicly, this can look like a simple logistics adjacency. The deeper operating logic is clear. Unicommerce wanted to become a one-stop shop for e-commerce enablement across three layers: customer engagement, transaction processing, and order fulfillment. Uniware already sits in transaction processing. Shipway brought courier aggregation and shipping automation to the fulfillment process. ConvertWay introduced an entry point for customer engagement and marketing automation. Shipway served around 3,000 clients, had FY24 revenue of ₹425.6 million, a gross margin of approximately 20%, with courier aggregation contributing around 85% of revenue, and losses reduced from ₹42.8 million in FY23 to ₹22.3 million in FY24. Unicommerce agreed to acquire an initial ~43% stake for ₹684 million in cash, with the remaining stake to be acquired later through a non-cash merger/share-swap mechanism.

Unicommerce had already started building UniShip, but customers began asking for aggregation capabilities, which required a different product mindset and courier-partner relationships. Developing a competitive offering internally could take 24–30 months. Shipway gave Unicommerce speed, a frugal team, a decent product, cultural fit, and a visible path to profitability. These four acquisition filters are: the target must make sense for existing customers, have a good product/team, culturally fit Unicommerce’s frugal DNA, and either be profitable or have a clear path to profitability.

The integration was faster than expected. By Q4 FY25, management said Shipway reached adjusted EBITDA breakeven after a small adjusted EBITDA loss during the brief Q3 consolidation period. The levers were joint sales, cross-selling, direct-cost optimization through better partner rates, and indirect-cost optimization through shared corporate functions.

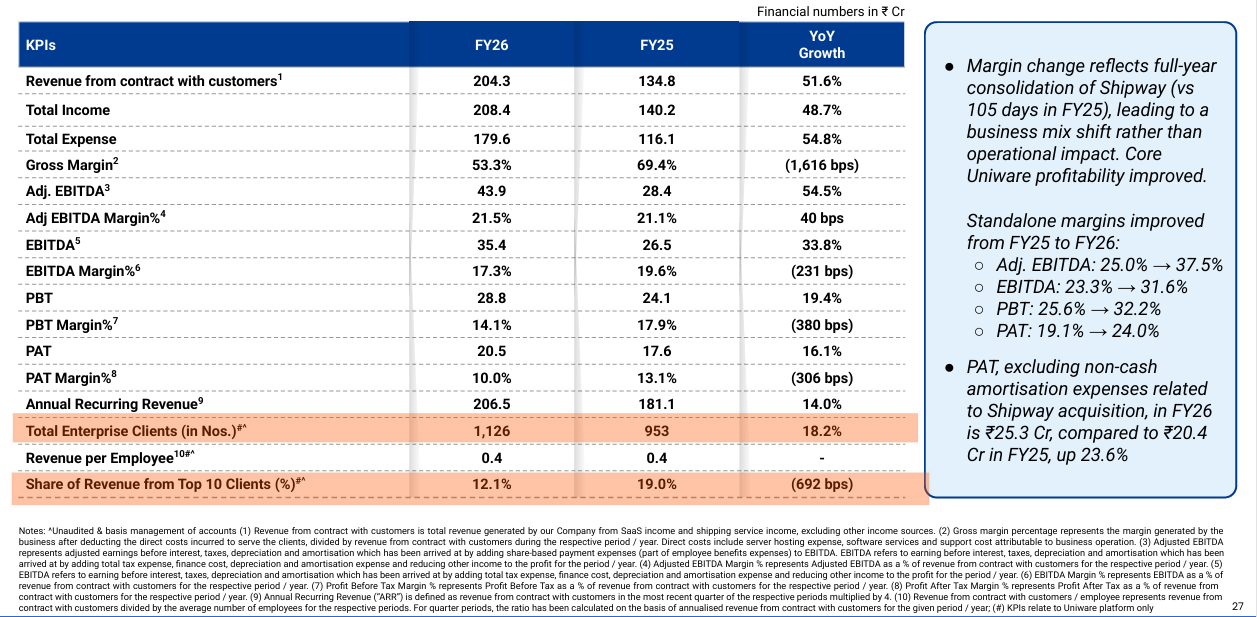

Still, the acquisition changes the analytical lens. Uniware is a high-gross-margin SaaS engine, while Shipway’s courier aggregation business has structurally lower gross margins. The business is now more complex: it is no longer enough to track only Uniware revenue, ARR, transaction run-rate, and NRR. We need to understand Uniware standalone growth, Shipway growth, ConvertWay adoption, cross-sell overlap, goodwill/amortisation, and reinvestment intensity. The company began moving away from transaction-related metrics in Q3 FY26, arguing that its product mix had diversified and that aggregate transaction rates had become less representative. That may be logically valid, but it reduces historical KPI continuity for us.

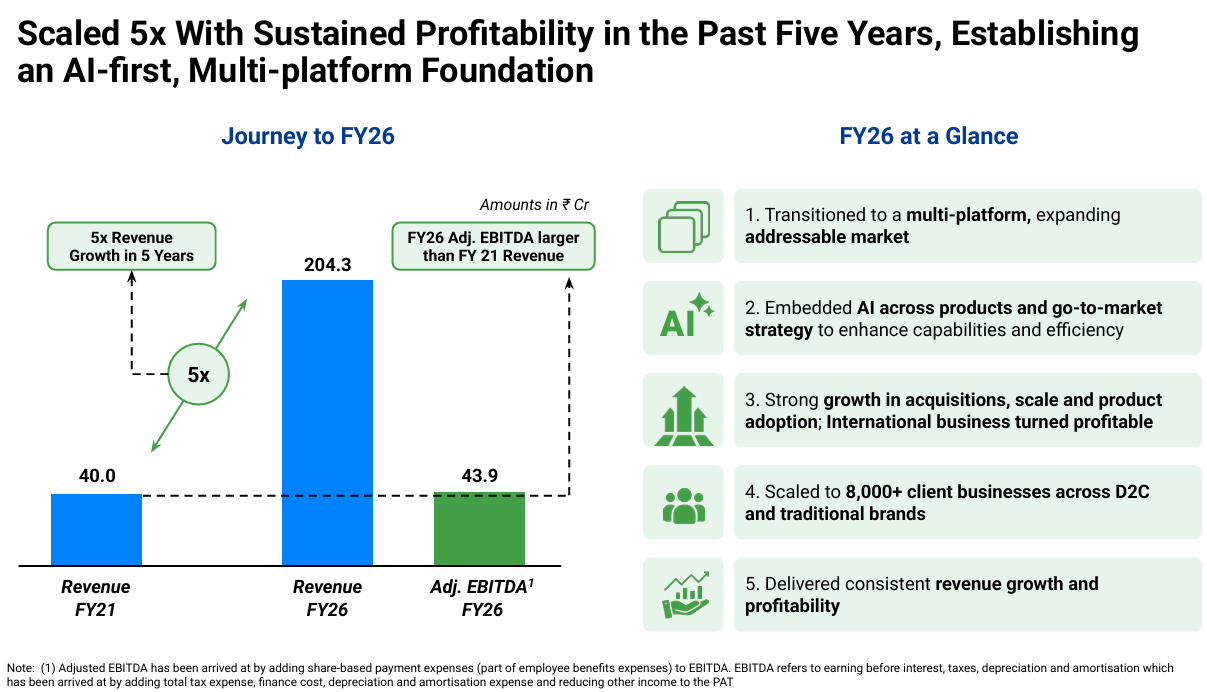

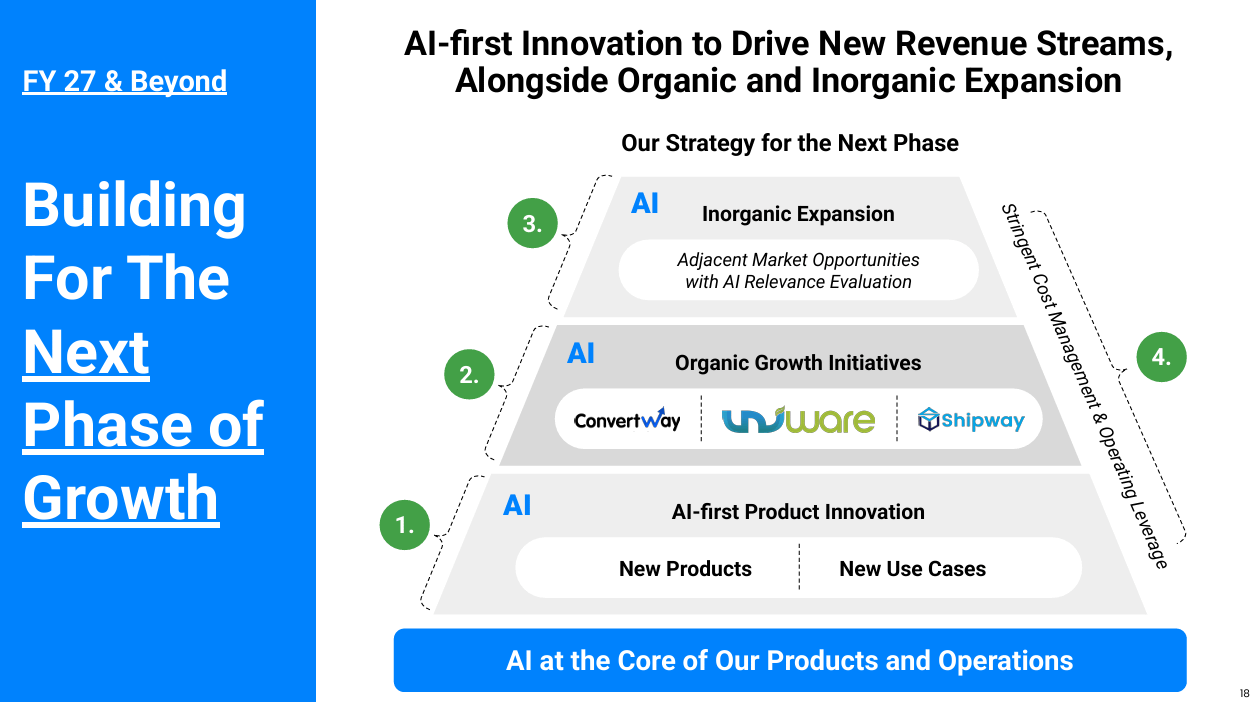

FY26 was the year Unicommerce formally repositioned itself from a Uniware-led SaaS company into a multi-platform e-commerce enablement company. It had repositioned itself as “AI-First eCommerce Enablement” and said it had completed its evolution into a multi-platform company with Uniware, Shipway and ConvertWay spanning transaction processing, logistics and customer engagement. It also said revenue had grown 5x over five years and FY26 adjusted EBITDA exceeded FY21 revenue, highlighting the operating leverage built in the business.

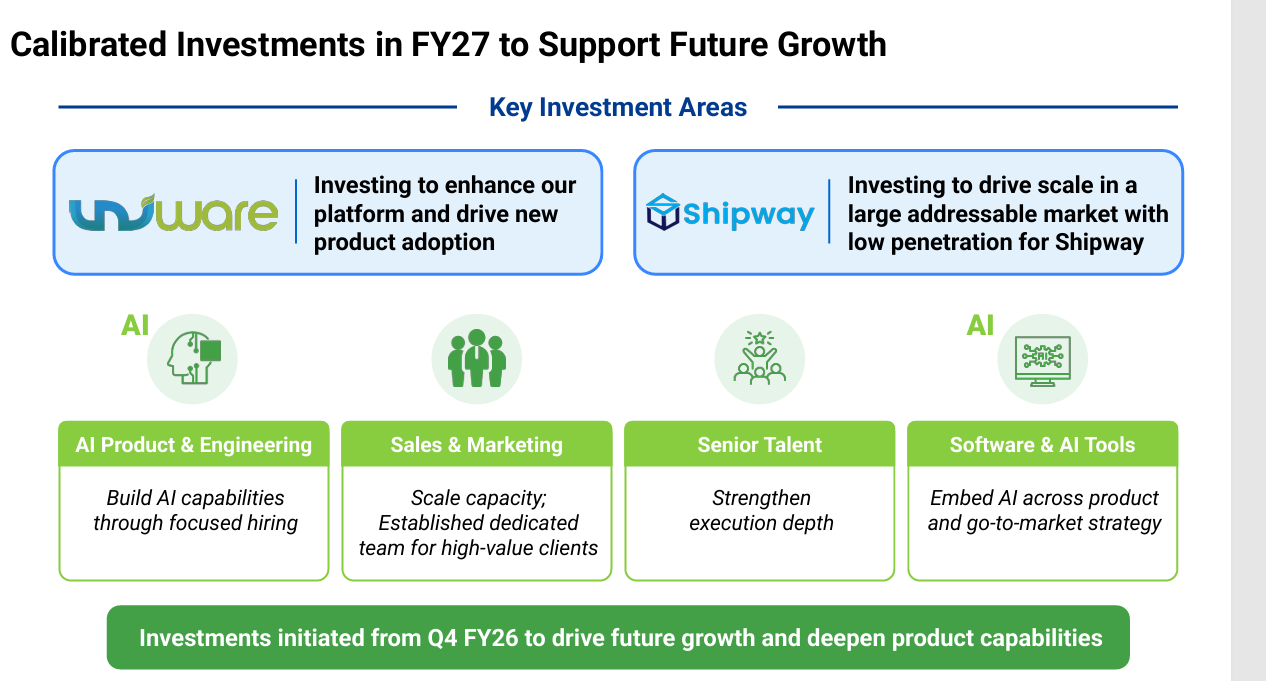

The FY26 numbers support this evolution. FY26 revenue stood at ₹204.3 crore, up 51.6% YoY; adjusted EBITDA was ₹43.9 crore, up 54.5%; PAT was ₹20.5 crore, up 16.1%; operating cash flow was ₹47 crore; and cash/bank balances increased to ₹81.3 crore. PAT growth lagged adjusted EBITDA because of Shipway-related non-cash amortization. Q4 FY26 growth was more muted because the company began investing in sales and marketing, AI-first product development and senior capacity. The important interpretation is that Unicommerce is now shifting from pure operating leverage to a phase of reinvestment for growth.

AI is not being positioned as a vague buzzword. The company has already launched UniBot AI for warehouse operations, ShipSense AI for logistics allocation, and Catalyst Voice Bot AI for customer engagement. Unicommerce has more than a decade of operational context across orders, inventory, warehouses, logistics, and customer workflows. AI enables it to convert that context into decision support and automation. In simple terms, Unicommerce may gradually move from being a system of record to becoming a system of decisions. For more context, you may read a short LinkedIn article I wrote a few weeks ago.

AI becomes powerful only when it wrestles continuously with your private intelligence.

AI becomes powerful here for Unicommerce because it is wrestling continuously with the private intelligence Unicommerce has built over a decade.

Competition appears less threatening in core Uniware than in Shipway. Unicommerce is significantly larger than the next player in core transaction processing, and the bigger opportunity is still converting businesses away from manual/Excel-led operations. The company processed around 25–30% of India’s dropship volumes through Uniware in FY25.

The future path has three parts. First, Uniware needs to return to consistent double-digit growth through enterprise additions, cross-sell, B2B/quick-commerce modules, UniReco, and international growth. Second, Shipway needs to become the largest growth engine by scaling courier aggregation, cargo, logistics automation, and ConvertWay while reinvesting profits for market share. Third, the company is open to selective acquisitions in white spaces, especially where customer demand, strategic fit, and cultural fit are clear.

Shipway/ConvertWay had achieved an annualized revenue run-rate of about ₹100 crore in Q3FY26, up from ₹71 crore in Q1 FY26, and that calibrated investments in AI, technology, sales, marketing, and brand building could temporarily take Shipway slightly below breakeven on an adjusted EBITDA basis.

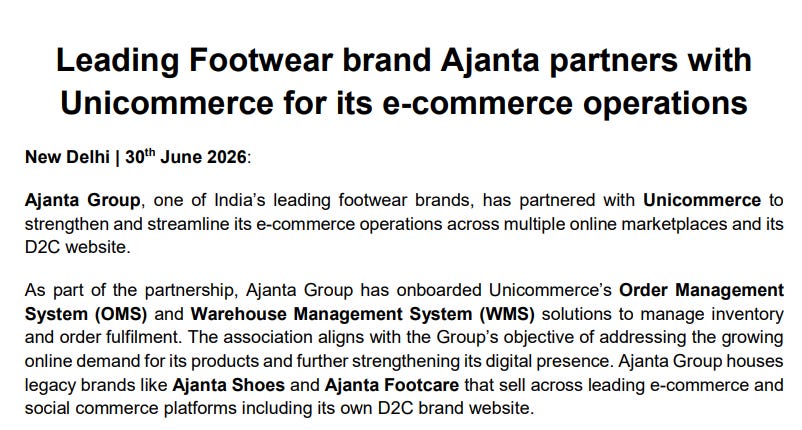

Before I summarize the key positives and risks and conclude my piece, I wanted to share something that caught my attention. I have pulled it from the notifications sent by Unicommerce to the stock exchange in June.

Does it ring a bell for you? It sure does for me. I am reminded of this masterpiece.

This particular point from the piece by Paul Graham is not only relevant to but visible in Unicommerce:

The unscalable things you have to do to get started are not merely a necessary evil, but change the company permanently for the better. If you have to be aggressive about user acquisition when you’re small, you’ll probably still be aggressive when you’re big. If you have to manufacture your own hardware, or use your software on users’ behalf, you’ll learn things you couldn’t have learned otherwise. And most importantly, if you have to work hard to delight users when you only have a handful of them, you’ll keep doing it when you have a lot.

Now let’s summarize.

The key positives are therefore clear: a founder-like professional CEO with deep tenure; a profitable, cash-generative core platform; strong operating leverage; a frugal and tech-first culture; widening product relevance; early acquisition integration success; and a potentially valuable AI layer built on proprietary operational context.

The key risks are equally clear: consolidated growth can mask Uniware’s organic growth; Shipway is a lower-margin, more competitive business; goodwill/amortization and acquisition integration require monitoring; discontinuation of transaction KPIs reduces comparability; and reinvestment in FY27 must translate into growth rather than merely higher costs.

For me, the central question is no longer whether Unicommerce is a good OMS/WMS company. The question is whether it can become the operating layer for Indian commerce across order processing, inventory, fulfillment, marketing automation and AI-led decisioning, while retaining the three cultural traits that built the business: resilience, tech-first thinking and frugality. If the company broadens its platform without losing discipline, the next few years could look very different from the last few. If it widens too fast, the very focus that created Uniware’s strength can get diluted.

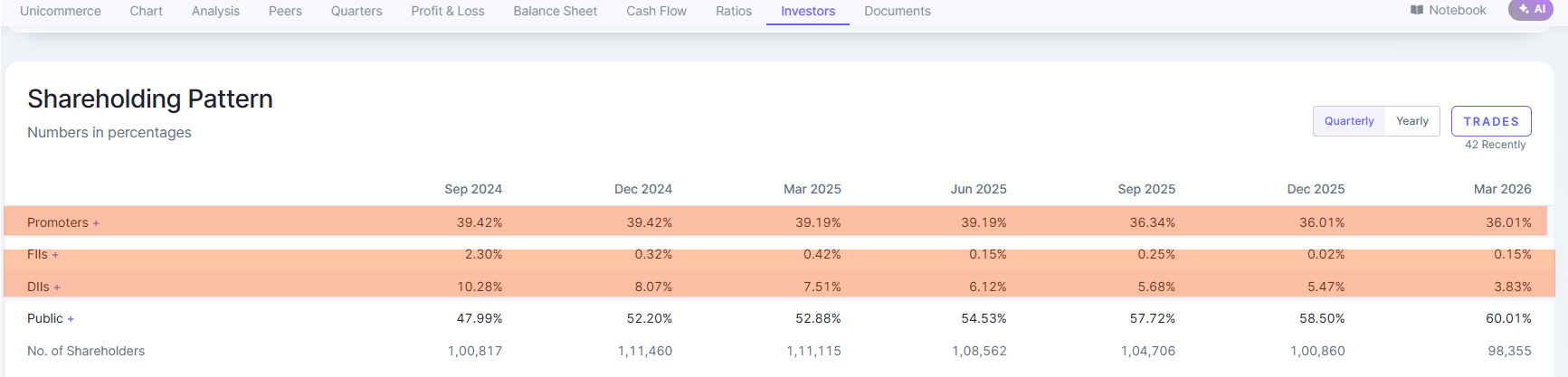

One topic I frequently come across in the media and on social media is promoter shareholding.

The question that almost always dominates the discussion is:

“Why are the promoters reducing their stake?”

For many investors, a promoter selling immediately becomes a red flag.

I think this is one of those situations where it helps to step back and look at how investing itself evolves. Time and again, markets have struggled to understand businesses that do not fit existing mental models.

When Infosys came to the public markets in the mid-1990s, we were not accustomed to companies with very few tangible assets creating enormous value.

When HDFC Bank was listed around the same period, the idea of a bank built around retail lending rather than corporate lending was still unfamiliar.

When Pantaloons expanded aggressively in the early 2000s, organized retail itself was viewed skeptically.

When Eicher Motors was selling roughly 50,000 Royal Enfield motorcycles in the late 2000s, very few people imagined that annual sales would eventually exceed 1.2 million motorcycles in the next decade and a half.

More recently, as quick commerce began gaining traction around 2023, many questioned whether consumers would ever routinely order groceries for delivery within 10 minutes.

In hindsight, these businesses appear obvious. At the time, they looked unfamiliar because investors were evaluating them through frameworks developed for an earlier generation of businesses.

I believe new-age technology businesses require a similar shift in thinking.

Unlike traditional manufacturing or family-owned businesses, promoter shareholding in many technology companies reflects years of venture capital funding, private equity investments, employee stock ownership plans, and public market listings. The promoter group is often only one part of a much broader ownership structure. If these long-term financial investors had not provided patient capital during the formative years of these businesses, many of them might never have reached the scale they enjoy today.

Therefore, for businesses such as Unicommerce, the more relevant question, at least in my view, is not simply whether promoters are selling. The more useful questions are: when did early FII/DII begin reducing their holdings, how much have they already exited, how concentrated were their original positions, and at what stage does the ownership structure begin to rise again? That is where my attention tends to be.

This thought process eventually led us to develop what we call the Fundamental Patterns of Zen Nivesh.

Just as technical analysts look for recurring chart patterns, we at Zen Nivesh try to identify recurring business patterns. Every pattern begins as a hypothesis. Some eventually prove useful, while others are discarded as we study more companies.

One such pattern has emerged repeatedly across several new-age technology businesses.

Step 1: Listing at an exceptionally high valuation, often valued at 15-30x sales rather than earnings.

Step 2: Podcasts, media coverage, and influencer discussions remain elevated for an extended period.

Step 3: DII/FII participate pre-IPO and at the IPO.

Step 4: Promoters and early financial investors sell meaningful stakes at the IPO.

Step 5: Promoter and DII/FII shareholding gradually declines post IPO.

Step 6: The company undertakes a meaningful acquisition funded through cash, equity, or a combination of both.

Step 7: Reported financial statements temporarily become more difficult to interpret because acquisition accounting and integration costs obscure the underlying operating performance.

Step 8: Operational synergies gradually begin appearing in the numbers.

Step 9: The business enters a new phase of earnings growth.

Step 10: Earnings growth is eventually recognized by the market and reflected in the share price.

This is not a rule. It is simply a pattern that we continue to observe, test, and refine. Looking back, new-age tech businesses such as Zomato, CarTrade Tech, RateGain Travel Tech, and Nykaa have exhibited several elements of this progression, although each has followed its own unique path. Viewed through this framework, Unicommerce appears to be somewhere around Step 7 today.

The acquisition of Shipway has made the reported financial statements more complex. Amortization of acquired intangibles, lower-margin courier aggregation revenues, integration costs, and changes in reported KPIs have made the business more difficult to analyze than it was before. The important question now is not whether these complexities exist; they clearly do. The important question is whether the underlying operating synergies begin showing up over the next few quarters in the form of stronger cross-selling, higher customer lifetime value, better operating leverage, and sustained earnings growth.

And while the business prepares for that stabilization and resumption of growth phase, the market may remain uncertain. It can therefore push the price to a level where the valuation becomes ridiculously cheap.

Step 8 is generally when valuation hits rock bottom. And often, not always, it captures almost all the risks and uncertainty. How close are we to step 8 in Unicommerce? I don’t know. Bottoms are always clearer after the rise. :)

Don’t Predict, Prepare!

Thanks for reading.

SEBI Disclosure: No Holding, No Recommendation

P.S. Know more about Zen Nivesh and our origin story here.

| A guest post by

|

Brilliant write-up.

👍👍👍👍👍👍👍👍

❤️🩹❤️🩹❤️🩹❤️🩹❤️🩹❤️🩹❤️🩹❤️🩹

🙏🙏🙏🙏🙏🙏🙏🙏