Suyog Telematics: A Deep Dive!

Can This Telecom Underdog Win The Race? | Research Lab | Issue#19

In the Bollywood classic, Jo Jeeta Wahi Sikandar, the wealthy, polished students of Rajput dominate every inter-school cycle race. Yet, in the end, it’s Sanju—the underdog from Model School—who defeats them with grit, resilience, and belief.

In the Indian telecom infra space, a giant like Indus Towers dominates. But in one corner stands a lesser-known player: Suyog Telematics. A company building towers in slums, small cells on flyovers, and fiber for BSNL.

The question is: can this underdog surprise everyone?

I don’t know.

But I know about two young, smart, and curious investors, Ayushi & Bhavana. Even in this age of AI and smartphones, they exhibit a few old-school traits. They took a printout of all the annual reports (FY14 to FY25), a few sections of the DRHP (2013), and the transcripts of the last four quarters' result conference calls.

Both of them sat in a cafe flipping through annual reports year by year, pausing to digest management commentary, numbers, and context. And in the process, making sense of Suyog as an underdog.

I secretly listened to their discussion, which lasted a couple of hours.

Oh boy, these girls never run out of things to say.

I am whispering their discussion in your ears, with a promise that you won’t tell them or anyone else what I am just about to do. Let’s get started.

Introduction

Bhavana: Do you remember Jo Jeeta Wohi Sikandar? That final cycling race where Sanju, the underdog with no fancy gear, takes on the rich kids?

Ayushi: Of course. Everyone thought he’d collapse halfway. But he kept grinding, lap after lap, and suddenly the crowd realized — he’s still in it, overtaking riders one by one.

Bhavana: That’s exactly how I see Suyog Telematics. Not the flashiest, not the biggest tower company. But an underdog with grit, clever strategy, and stamina.

Ayushi: Perfect analogy. Let’s pedal through their journey. We’ll start from the IPO baby years and watch how this little-known Mumbai player grew into a national infra provider.

Part I The Early Climb (FY14 to FY18)

FY14 IPO Baby Steps

Ayushi: FY14 is where the story really begins, the IPO year. They were listed on the SME platform of BSE in January 2014.

At that point, their asset base was small: 79 towers in Maharashtra & Uttarakhand, 359 poles in Mumbai, and ~150 km of optic fiber cable around Mumbai.

Their DNA was EPC (engineering, procurement, construction). They’d already installed 10,000+ rooftop towers for BSNL as contractors. That is like training on borrowed bikes before owning one.

Bhavana: So they were transitioning from “builder” to “owner and landlord.”

Ayushi: Exactly. And they had a knack for unusual locations: MSRDC flyovers, MMRDA skywalks, Bandra-Worli Sea Link. Places where coverage was bad, but permissions were hard. That’s their version of Sanju sneaking into the racing line others ignored.

FY15 Consolidating the Base

Bhavana: What about FY15?

Ayushi: Not a dramatic leap, but important.

They focused on strengthening their Mumbai/Maharashtra presence.

Revenue grew modestly, but cash flow was stable thanks to the IPO proceeds.

Management commentary emphasized the moat of government tie-ups, their ability to secure prime locations that rivals found tough.

Bhavana: So still local champions, but laying bricks patiently. Like Sanju doing practice laps.

FY16 First Signs of Muscle

Ayushi: FY16 shows them flexing slightly.

Clientele broadened: not just BSNL/MTNL, but also private operators started appearing.

They started describing sites as fiber-ready. That’s 2016, years before 5G, but they were already preparing for a future where every tower needs fiber backhaul.

Bhavana: Like fitting lighter wheels on your cycle before a race you know is coming.

Ayushi: Exactly. Financials were still modest, but importantly, profitable. No debt trap, no reckless expansion.

FY17 The Jio Effect

Bhavana: I guess FY17 was the big external trigger?

Ayushi: Yes. Reliance Jio launched commercially in September 2016, changing the telecom industry. Suddenly, every operator needed denser networks.

Suyog, with its rooftops and poles in Mumbai, was in the right place.

Tenancy additions picked up.

The annual report sounded more confident, highlighting tenancy growth and network readiness.

Bhavana: Like Sanju finally getting a proper racing cycle, his years of practice suddenly paid off.

FY18 From Local to National

Ayushi: FY18 is when they start using the phrase “pan-India presence.”

Expansion beyond Maharashtra accelerated.

Tenancies crossed 2,000 for the first time.

Revenue curve steepened; the trajectory looked more like a slope than a flat line.

Bhavana: So by FY18, they’d proven the model: own towers, lease to multiple telcos, stick to niches.

Ayushi: Yes. The underdog had stamina and strategy. It wasn’t about having the most towers; it was about owning hard-to-get, high-demand sites.

Timeline (1995 to FY18)

Ayushi sketches a quick timeline on a napkin.

1995: Suyog founded.

2008: Got IP-1 license.

2013: Became public company.

2014: SME IPO.

2014–18: Slowly expanded, client list widened, fiber-ready talk began.

Bhavana: Like Sanju training quietly before the big race.

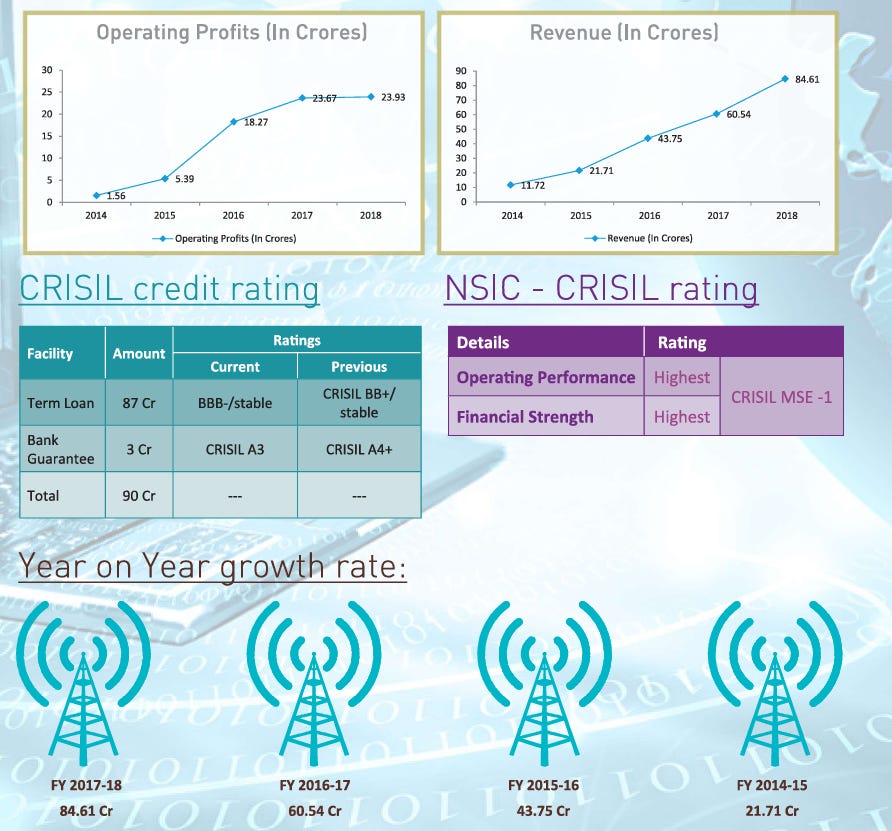

Source: FY18 Annual Report

Ayushi: If you look at a revenue chart from FY14–18, the line is modest but rising. What matters is tenancy growth and foothold in government sites.

Bhavana: The crowd still isn’t watching closely, but Sanju is in the peloton, biding his time.

Cliffhanger

Bhavana: So by FY18, Suyog is ready. The training wheels are off, the bike is tuned, and the external tailwind (Jio rollout) has begun.

Ayushi: Exactly. The next act, FY19–FY25, is where the underdog starts overtaking riders, moving from obscurity to NSE listing, Delhi expansion, and BSNL rollouts.

Part II The Scale-Up (FY19 to FY25)

FY19 From Mumbai to Bharat

Ayushi: FY19 AR feels like the first time Suyog says, “We’re not just Mumbai anymore.”

Began pushing beyond Maharashtra.

Tenancies crossed ~2,500.

Revenue is rising steadily.

Management’s language shifted from local stronghold → national aspirations.

Bhavana: Like Sanju no longer just racing on the colony road but entering state-level races.

FY20 The Industry Storm

Ayushi: FY20 was rough. The industry was in turmoil, AGR dues, Vodafone struggling, telco consolidation after Jio’s entry.

Revenue ~₹122 Cr.

Net Profit ~₹33 Cr.

Tenancy growth slowed, operators were cautious.

Bhavana: So, headwinds.

Ayushi: Yes, but key point: Suyog stayed profitable. Many infra players tripped; they kept pedalling.

Bhavana: Sanju riding through rain, still upright.

FY21 Recovery

Ayushi: FY21 AR shows recovery signs:

Revenue: ₹134.5 Cr.

PAT: ₹24.5 Cr.

Tenancies > 4,000.

Bhavana: Resilience. Not glamorous, but crucial, staying alive when others fall.

FY22 The Hockey Stick

Ayushi: FY22 is the hockey stick moment.

Revenue: ₹126 Cr.

PAT: ₹41 Cr.

EBITDA ~₹87 Cr (69% margin).

Tenancies > 5,500.

Bhavana: That’s a big jump in profitability on stagnant revenue.

Ayushi: Trigger = Jio + Airtel still expanding, plus BSNL beginning to stir.

Bhavana: Like Sanju suddenly finding his rhythm, overtaking riders who underestimated him.

FY23 Fiber and Small Cells Enter the Frame

Ayushi: FY23 marks diversification.

Revenue: ₹144 Cr.

PAT: ₹46 Cr.

Fiber rollout >3,000 km.

Small cell tenancies >2,500.

Bhavana: Why does this matter?

Ayushi: Because 5G = fiber + small cells. Towers alone won’t cut it. Suyog anticipated this.

Bhavana: So the chai tapri added snacks and cold drinks, not just tea. Nice!

FY24 Graduation

Ayushi: FY24 is their graduation year.

Revenue: ~₹167 Cr.

PAT: ~₹63 Cr.

EBITDA margins ~70%.

Tenancies: ~6,500.

And most importantly: Listed on NSE Main Board (20 Aug 2024).

Bhavana: From SME IPO in 2014 → NSE main board in 2024. A decade-long climb.

Ayushi: Shivshankar Lature even said in an interview, “Booked till 2040.” Long-term visibility of orders.

Bhavana: Imagine Sanju finally on the official race track with the elite.

FY25 Inflection Point

Ayushi: FY25 AR + concalls = inflection point.

Revenue: ₹193 Cr.

PAT: ~₹41 Cr.

EBITDA: ₹110 Cr (57% margin: hit by an ESOP charge of ₹27.5 Cr)

Tower base: ~5,700+.

Tenancies: ~7,100+.

Fiber: 6,000+ km.

Dividend: ₹1.80/share.

Bhavana: Big numbers for an underdog.

Ayushi: And two strategic moves:

Lotus Tele Infra acquisition (Delhi-NCR): 95% stake, 120 towers with Airtel & Jio tenancy, ₹13.5 Cr cost. Management expects ~50% tenancy boost by adding Vodafone & BSNL.

BSNL expansion: ~2,500+ towers in FY25, similar pipeline for FY26.

Bhavana: So they’re no longer confined to Maharashtra. They’re national.

Ayushi: Correct. And management guidance was bold:

+5,000 tenancies in FY25.

+5,000 in FY26.

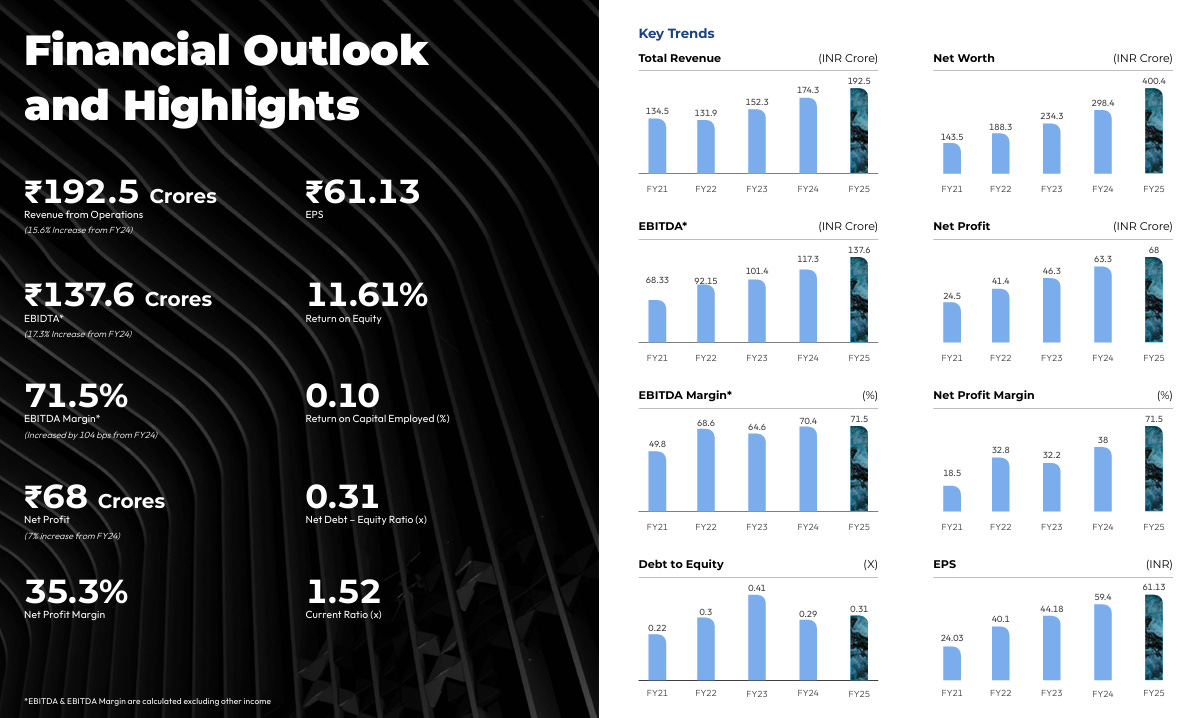

Source: FY25 Annual Report

Ayushi: Look at this chart (from FY25 AR).

Revenue: ₹134.5 Cr → ₹400.4 Cr.

PAT: ₹24.5 Cr → ₹68 Cr.

EBITDA: ₹68.3 Cr → ₹137.6 Cr.

(She slides over the plotted graphs: revenue, PAT, EBITDA, all climbing steeply.)

Bhavana: That’s Sanju overtaking, lap after lap, until suddenly he’s at the front.

Promoter Interviews Add Colour

Ayushi: Around FY25, Shivshankar Lature gave interviews that reveal confidence:

“We are in profit & have a good order book.”

“High profits, good order book, 6G readiness.”

“Booked till 2040.”

“₹200+ Cr investment in MP (telecom & ropeways).”

Bhavana: Ropeways?

Ayushi: Yes, his other venture (Suyog Gurbaxani Funicular Ropeways) turned profitable in 2023. Shows his comfort with capital-intensive, long-gestation infra.

Bhavana: The man plays long games.

Cliffhanger End to Part II

Bhavana: So by FY25, Suyog is:

National footprint.

High margins.

Clear order pipeline.

Promoter betting confidently.

Ayushi: The underdog is no longer just “in the race.” He’s leading a pack.

Bhavana: Next question: Can he hold the lead? Risks, industry shifts, promoter style, 5G → 6G.

Ayushi: That’s Part III: The thematic deep dive.

Part III The Bigger Picture

1. Business Model Like Renting Out Your Roof

Ayushi: Imagine you have a big rooftop in Mumbai. Airtel comes and says, “Can we put our antenna here? We’ll pay rent monthly, increase it every year, and if we leave early, we’ll pay a penalty.”

That’s Suyog’s business model, multiplied across 5,800+ towers, poles, and rooftops.

Bhavana: So Suyog is basically a landlord for antennas?

Ayushi: Exactly. And the beauty is in the contracts:

Long tenures (7–10 years).

Annual escalations (~2.5%).

Exit penalties if tenants walk away early.

Advance billing, Suyog gets paid before delivering services.

Bhavana: Like having tenants who not only pay rent on day one but also commit for a decade.

2. Revenue Components: The Chai Tapri Menu

Ayushi: Think of Suyog’s revenues like items on a tea stall menu:

Tower rentals (chai cups) is the core.

Loading charges (extra biscuits) are like more antennas = more rent.

Small cells (cutting chai glasses) are compact but profitable for dense urban zones.

Fiber leasing (bottled water) is critical for 5G backhaul.

Utilities reimbursement (milk costs) — electricity/diesel charges passed through.

Bhavana: And each extra customer (operator) makes the stall more profitable, while costs barely rise. That’s why EBITDA margins stay above 70%.

3. Promoter Lens: The Rider Behind the Cycle

Ayushi: Let’s zoom in on Shivshankar G. Lature, the man pedalling.

Background: Civil engineer, founded Suyog in 1995 with his brother.

First innings: Installed 10,000+ BSNL rooftop towers (EPC work).

Second innings: Got IP-1 license in 2008 → became an owner of towers/fiber.

Third innings: Listed in 2014 (SME), migrated to main board in 2017, NSE listing in 2024.

Bhavana: Steady progression. Contractor → owner → listed company.

Ayushi: And his public comments show consistency:

“We are in profit & have a good order book.”

“Booked till 2040.”

“₹200+ Cr investment in MP telecom & ropeways.”

He also runs Suyog Gurbaxani Funicular Ropeways, which turned profitable in 2023. Ropeways are capital-heavy, long-gestation infra. Same DNA as towers.

Bhavana: So he’s not chasing quick wins. He’s comfortable with decade-long plays.

4. Industry Insights: The Track Ahead

Ayushi: The Indian telecom infra industry is a monster race track.

India = world’s biggest data consumer.

5G rollouts: By late 2024, >4.6 lakh 5G sites were active.

Fiberization gap: India needs 15–20 lakh km more fiber in 3–4 years.

Towers: India has ~7.5 lakh towers; the industry needs ~12 lakh for 5G/6G.

Bhavana: So demand is guaranteed.

Ayushi: Exactly. And IP-1 players like Suyog are crucial because telcos prefer leasing over owning infra.

Global parallels:

American Tower, Crown Castle (US).

China Tower (China).

All scaled on the same model, recurring rental, multiple tenants, high margins. India is catching up.

5. Market Position: Underdog’s Moat

Ayushi: Suyog isn’t Indus Towers of India (4 lakh towers) or ATC of the USA (75,000). But its moat is location and speed.

Government sites: flyovers, depots, sea-links, slums. Hard for rivals to replicate.

First mover in small cells: already >4,000 tenancies.

Lean ops: in-house O&M, builds a tower in 20–30 days once a service order is given.

Bhavana: So they’re not winning by being the biggest, but by being fastest and cleverest.

6. Risks & Headwinds: The Potholes

Ayushi: Every rider faces potholes. For Suyog, they are:

Customer concentration: Jio, Airtel, VIL, BSNL = >95% of revenue.

Receivables: Vodafone’s payments are often delayed.

Capex intensity: ₹450–500 Cr annually. The Balance sheet must support.

Fiber monetization lag: Heavy investment now, revenues kick in post-FY27.

Regulation: RoW delays, EMF compliance hurdles.

Tech risk: Satellite connectivity, but management insists it’s complementary (too costly for the India mass market).

Bhavana: So an investor must watch receivables, debt, and rollout execution.

7. Future Vision: Management’s Guidance

Ayushi: Q2FY25 concall gave crystal-clear guidance:

+5,000 tenancies in FY25.

+5,000 in FY26.

Total ~15,000 tenancies by FY26.

Capex plan: ₹450–500 Cr annually.

Fiber monetization: meaningful revenues from FY27 onward.

FTTH: 5 lakh home passes by FY29, ~15% of revenue.

Bhavana: Rare clarity for infra players.

8. Why This Story Resonates Jo Jeeta Callback

Ayushi: Remember Sanju in Jo Jeeta Wohi Sikandar?

He didn’t have the fancy cycle.

He had grit, smarts, and patience.

He stayed in the race, lap after lap, until he sprinted past the giants.

That’s Suyog:

Not the biggest towerco.

But moats in government sites, execution agility, smart expansion (Lotus in Delhi).

And now visible order book, profitability, and national footprint.

Bhavana: The underdog isn’t just in the race anymore. He’s leading the final lap.

9. What a New Investor Should Remember

Bhavana: If I were a first-time investor reading this café chat, I’d keep these in mind:

Recurring annuity-like revenues with long contracts.

Moats = location and speed.

Runway = 5G densification, fiberization, BSNL expansion.

Risks = receivables, capex, customer concentration.

Promoter = Infra veteran with patience.

Ayushi: Exactly. That’s all you need to understand the business, without any buy/sell recommendation.

Closing Scene — The Finish Line

Bhavana: So what’s the takeaway?

Ayushi: That sometimes, in investing, the underdogs win. They don’t need flash or scale from day one. They just need to keep pedalling, build moats others can’t, and sprint when the industry tailwind blows.

Bhavana: Jo Jeeta Wohi Sikandar. And in the world of telecom infra, Suyog Telematics is Sanju on the cycle — underestimated, but steadily winning laps. But can this telecom underdog win the race?

Thanks for reading!

P.S. In the original post, there was no mention of ESOP dilution and QIP mishap, which may have led to a more favourable view on the business. However, we have corrected it by sharing the impact of the large ESOP dilution in this post. Apologies for the inconvenience.

| A guest post by

|

But yes credit for culling out a lot of intricate details. We had big international companies like American Tower come to India and exit..So it seems local frugal operators can only survive...

Well written..but yes a tough sector with many pot holes ..