Wealth First Portfolio Managers: A Deep Dive

3-Decades | From Fixed Income To AMC | ZN Research Lab-53

I wish to share a personal story here. Trust me. I am not making this up. When the shares of Wealth First Portfolio Managers got listed in 2017, a person I respect immensely told me that he owned shares of Wealth First and casually asked for my opinion on the business. I requested him to send me the latest annual report. He immediately did. Like I generally do with unknown businesses, I started with a cursory reading, instead of a deep dive. Within a few minutes, one thing became obvious. Almost the entire business appeared to revolve around trading and distribution of fixed-income securities. At that point, my understanding of investing was fairly straightforward. Businesses that build products, software, or brands usually enjoy long growth runways. But what about businesses dependent on trading income? I wasn’t sure. My immediate reaction was something along these lines.

“I don’t think I can take a long-term view on this business.”

And I moved on. I don’t remember how long the gentleman continued holding the shares. Life moved on. Thousands of companies appeared on my screen. Many disappeared. Wealth First disappeared from my memory. Until one day in January 2025. I was randomly browsing companies on Screener when Wealth First appeared again.

Its share price had increased roughly 50 times from its SME listing price. I literally paused. “Wow. What a miss.”

That increased my curiosity. So, I read almost everything publicly available on Wealth First. The DRHP. Last five years’ Annual Reports. Investor presentations. Two conference call transcripts. Regulatory filings. And multiple external sources directed by my diligent intern, ChatGPT. What started as an attempt to understand a missed investment slowly turned into a motivation to understand the business model. And as I read it, another mental framework slowly emerged.

The 3Ts Framework

Why do only a handful of people or businesses eventually succeed despite thousands of equally hardworking competitors? Over time, I realized that most enduring success stories are built on three simple forces.

Time. Trust. Tailwind. The Three Ts.

Let me explain. Take cricket as an example. India has produced thousands of talented cricketers. Almost all of them invested enormous time into mastering the game. Only a fraction of them managed to build trust. Trust of teammates. Trust of selectors. Trust of fans. Trust that when the team needed them, they would deliver. But something extraordinary happened in 2008. The Indian Premier League was born. That single event changed Indian cricket forever. Take the example of Ravindra Jadeja. He came from a modest family near a village in Rajkot, Gujarat. He had already put in years of hard work. He had already earned respect within cricketing circles. Then came the IPL. In the very first season, Shane Warne famously nicknamed him “Rockstar.” That one season didn’t merely change Jadeja’s life. It changed Indian cricket itself. Suddenly, thousands of young cricketers who had never dreamt of making a living from cricket began believing that a career was actually possible. The tailwind had arrived. Time and trust were always largely within Jadeja’s control. The IPL wasn’t. That was the tailwind. And once the tailwind arrived, those who had patiently survived long enough suddenly looked like overnight successes.

Take Bollywood as another example. Naseeruddin Shah and Om Puri are widely regarded as two of the finest actors. They devoted decades to their craft and earned immense respect from critics, filmmakers, and fellow actors. Yet most mainstream moviegoers, both in their own generation and ours, never experienced much of their finest work because it largely belonged to parallel cinema rather than to mainstream commercial films. They were admired, but they never became mass superstars like Rajesh Khanna, Rishi Kapoor or Amitabh Bachchan. Something similar could easily have happened to Pankaj Tripathi and Nawazuddin Siddiqui. They also spent years honing their craft and earning directors’ trust long before audiences truly knew them. Then came the OTT revolution. Suddenly, storytelling changed. The demand for strong character actors exploded, and the world finally caught up with the talent they had quietly built over decades. Their hard work hadn’t suddenly improved overnight. The tailwind had finally arrived. Time and trust were always largely in their hands. The tailwind wasn’t. And once it arrived, years of patient preparation suddenly looked like an overnight success.

In many ways, success is often nothing more than being prepared when the world finally begins rewarding what you’ve been quietly building for years. As I read Wealth First’s journey, I realized that the company had unknowingly followed exactly this path. It spent decades building Time. Then it quietly accumulated Trust. And finally, over the last decade, especially post-COVID-19, the Indian stock market has provided the Tailwind.

To understand why the business looks the way it does today, we first need to go back to 1992. Not to the stock market. But to a small office in Ahmedabad.

Phase I- Building Time [1992-2002]

If someone had met Mr. Ashish Shah in the late 1980s, they probably wouldn’t have guessed he would one day build one of India’s largest listed independent wealth management firms.

He wasn’t a finance graduate, or a chartered accountant, or a stockbroker. He was a mechanical engineer from LD College of Engineering in Ahmedabad. After graduation, he joined HPCL, one of the most sought-after employers of that era. Out of nearly 20,000 applicants, only 40 engineers were selected, and he was one of them. Over the next eight years, he worked across petrol pumps, airports, sales, marketing, and operations. Looking back, he often credits HPCL not for teaching him finance, but for teaching him discipline, systems, execution and customer-centricity, qualities that would later become deeply embedded in Wealth First’s culture.

Then came 1991. India liberalized its economy. For millions of Indians, liberalization was a policy reform. For Mr. Shah, it became permission to become an entrepreneur. In 1992, he resigned from HPCL, returned to Ahmedabad, and started Dalal & Shah Fiscal Services from a tiny 12 × 10 office with just three team members. Those three early colleagues are still associated with him today, a small detail that says a lot about the kind of organization he would eventually build.

Most entrepreneurs in financial services at that time were chasing the rapidly expanding equity markets. Ashish Shah deliberately chose a very different path. He chose fixed income. At first glance, that sounds like a conservative business decision. I think it was a strategic one. He explains why. In India, almost 85–90% of household financial wealth historically sat in relatively safe instruments: fixed deposits, bonds, provident funds, government savings schemes, and other fixed-income products. Yet very few advisors specialized in helping clients navigate this world. Everybody wanted to sell excitement. Very few wanted to specialize in safety.

That became Wealth First’s first niche. Instead of becoming another stock market intermediary, the firm became a specialist in:

Tax-free bonds

RBI Relief Bonds

Government securities

Money-market instruments

Corporate fixed deposits

Treasury solutions

Inter-corporate deposits

Its clients reflected that positioning. Rather than serving retail investors from day one, the firm primarily worked with:

Corporate treasuries

Cooperative banks

Pension funds

Provident fund trusts

Gratuity trusts

Institutions

High-net-worth individuals

Unlike equity investors, fixed-income investors have almost no tolerance for mistakes. When someone entrusts you with pension money or treasury capital, preserving capital matters more than maximizing returns. That environment naturally shapes behaviour. It forces discipline. It rewards process over excitement. It punishes unnecessary risk.

Looking back today, I think many of Wealth First’s later cultural traits: simplicity, independence, long-term thinking, and its obsession with “doing the right thing,” can be traced back to these formative years in fixed income rather than equity.

By the mid-1990s, another structural change was unfolding. India’s mutual fund industry was still in its infancy. Private-sector and global fund houses were entering the market, open-ended schemes were gaining acceptance, and the idea of professionally managed equity portfolios was beginning to reach affluent investors. While continuing to expand its fixed-income franchise, the company quietly began studying this new asset class.

Mr. Shah recalls being one of the earliest believers. He was writing cheques of ₹1.5 crore and ₹2 crore into a mutual fund when its total assets under management were only around ₹20–50 crore nationwide. Decades later, he was invited by that same fund house to cut the cake at its 30th-anniversary celebration because he had been among its earliest distributors in Gujarat.

That story reveals something subtle but important. Even in the 1990s, Wealth First wasn’t simply distributing products. It was trying to identify long-duration structural trends before they became obvious. The first decade, therefore, wasn’t really about becoming a wealth manager. It was about patiently accumulating the first T. Time.

Phase II- From Treasury Manager to Wealth Manager [2002-2016]

Every enduring business eventually reaches a point where its founder realizes that yesterday’s success formula won’t create tomorrow’s company. For Wealth First, that realization came somewhere around the turn of the millennium. By then, Dalal & Shah had spent almost ten years building credibility in treasury management and fixed-income products. The firm had earned the trust of institutions, cooperative banks, provident funds, corporate treasuries, and affluent individuals. It had become one of the better-known names in western India for fixed-income solutions. From the outside, everything looked comfortable. From the inside, Mr. Shah was beginning to notice something else. The business itself was changing. Because India was changing.

Economic liberalization had now been underway for almost a decade. Indian companies were becoming larger. Private sector employment was expanding rapidly. Professional managers were beginning to earn meaningful salaries. The equity culture was slowly entering middle-class households. Mutual funds were becoming increasingly accepted. Financial assets were slowly replacing traditional savings. None of this happened overnight. But together, these small changes created a completely different customer. Earlier, Wealth First primarily dealt with organizations. Now, a new customer was emerging. Corporate executives. Professionals. Business owners. Doctors. Lawyers. Entrepreneurs. People who had accumulated wealth but had no one trustworthy to manage it. One of the CFOs whose treasury Wealth First managed casually asked Mr.Shah once.

“Why don’t you manage my personal money as well?”

That single question may have changed the company's future. Until then, Wealth First managed institutions. Now it started thinking about families.

The difference is enormous. Institutions have balance sheets. Families have dreams. Institutions chase yields. Families chase financial security. Institutions think quarterly. Families think generationally. That required a completely different organization. At that point, Wealth First discovers its real business. From treasury relationships to family relationships to lifetime relationships. The products merely changed along the journey. The relationship became the business.

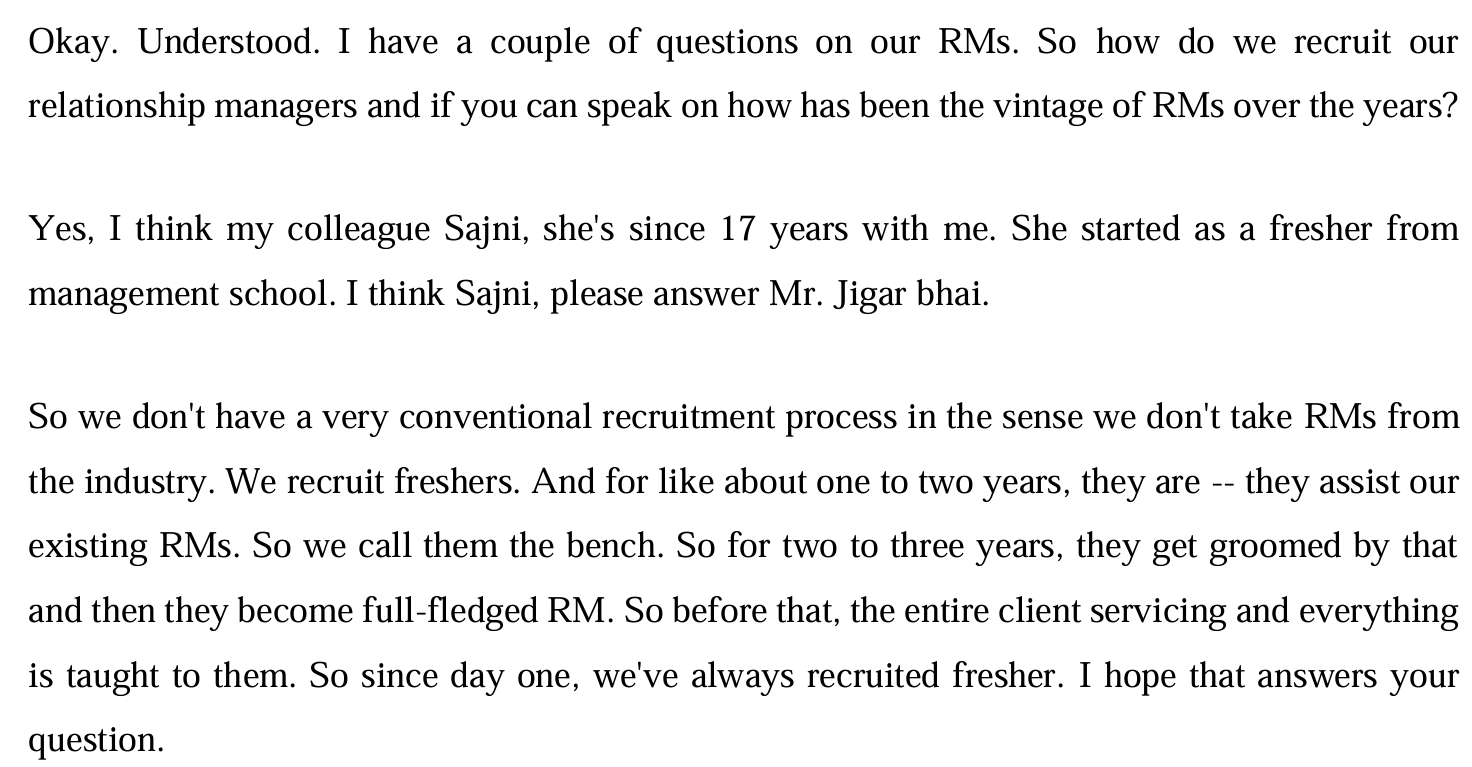

Around 2002, Wealth First made what appears to have been an unusually bold decision for that era. It started building a dedicated Relationship Manager (RM) model. Today, every wealth management firm has RMs. Twenty-five years ago, that wasn’t the norm. Mr. Shah notes that by 2002, Wealth First already had eight Relationship Managers in Ahmedabad, which he describes as almost unheard of at the time.

This decision fundamentally changed the company’s operating model. Instead of becoming product specialists, employees became relationship specialists. But Wealth First built RMs differently. Almost every wealth management company recruits experienced Relationship Managers from competitors. Wealth First chose the harder route.

They almost never hire experienced RMs. Instead, they recruit fresh graduates. Those graduates spend roughly two to three years assisting senior RMs. During that period, they learn a lot. Documentation. Operations. Client servicing. Culture. Communication. Processes. Asset allocation. And most importantly, regulation and compliance. Only after spending years within the organization are they allowed to manage client relationships independently.

This may be one of the company’s strongest moats. Because they aren’t merely hiring employees. They’re manufacturing a culture. The RM’s primary responsibility is not selecting investments. The RM’s job is to understand families, cash flows, and financial goals; maintain discipline; ensure asset allocation remains appropriate; and, most importantly, help clients stay invested. This creates enormous operating leverage. One RM can therefore manage far more families than would otherwise be possible.

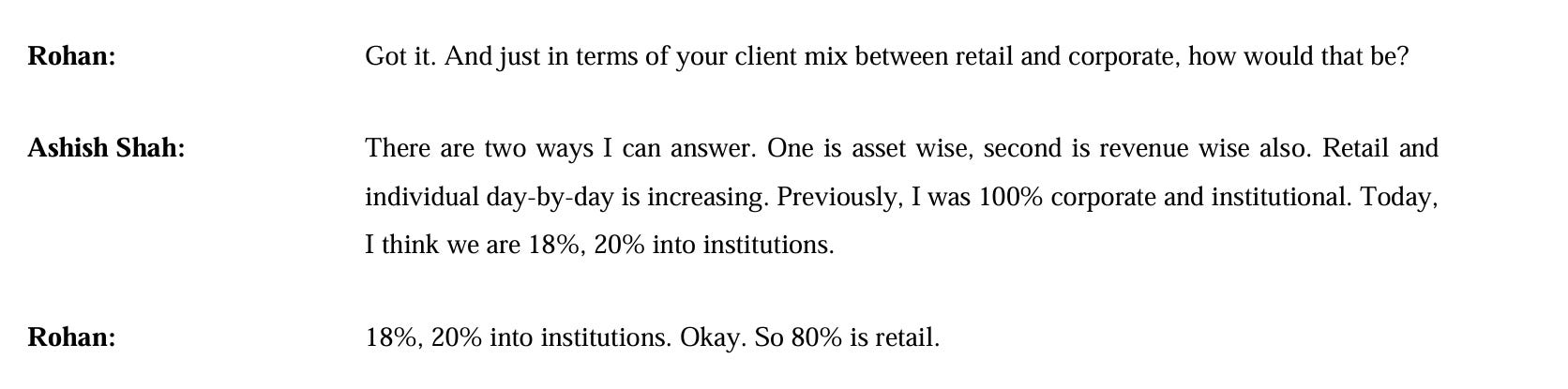

Another transformation was quietly taking place. The company slowly changed its customer mix. Initially, almost the entire business came from institutions. Corporate treasuries. Trusts. Banks. Over time, individual investors became increasingly important. Mr. Shah explains why. The very executives whose corporate money Wealth First managed had themselves become wealthy. If they trusted Wealth First with hundreds of crores of corporate treasury, why wouldn’t they trust it with their own personal wealth? Slowly, the center of gravity shifted. By FY25, roughly 80% of Assets Under Advice belonged to individuals, while only about 20% came from institutions.

This transition wasn’t accidental. It took almost two decades. Normally, companies articulate their philosophy after becoming successful. Wealth First appears to have developed a philosophy, and while still small, has shown remarkable consistency. Long before the words became marketing slogans, the behavior already existed. Certain beliefs keep appearing repeatedly.

Simplicity: As portfolios become larger, they should become simpler. Not more complicated.

No Leverage: The company refuses to encourage leveraged investing. No Margin Trading Facility. No derivatives-led wealth creation. No unnecessary complexity. Mr. Shah explicitly states that if wealth management’s objective is to preserve and grow wealth, adding leverage is fundamentally inconsistent with that objective.

Asset allocation: It is the “dharma and karma” of the Relationship Manager.

Education before investment: Perhaps the most fascinating aspect of their philosophy. Mr. Shah repeatedly says that Wealth First tries to educate clients before accepting the first cheque. Initially, I thought this was simply good customer service. Now I think it is actually customer selection. Because once expectations are aligned, clients panic much less during market corrections. Even during difficult markets, their net inflows often remained positive. The education happened long before the correction arrived.

Word-of-mouth: Wealth firms and high-push marketing normally go hand in hand as an industry norm. Wealth First instead focuses on investment awareness programs, corporate seminars, and knowledge sessions. No product selling. Only education. This creates an acquisition engine that becomes stronger with time. Today, management openly says that referrals remain their single largest source of new clients.

The SME IPO

By 2016, Wealth First had spent nearly twenty-five years quietly building its reputation. It was no longer a small treasury advisory firm. It had evolved into an increasingly sophisticated wealth management platform. The SME IPO wasn’t merely about raising capital. I think it served three equally important objectives.

First, to strengthen credibility. In financial services, trust is everything. A listed company automatically signals greater transparency.

Second, to create permanent capital. The proceeds were primarily intended for working capital requirements associated with fixed-income operations. The company still maintained meaningful bond inventories to facilitate client transactions and liquidity.

Third, perhaps the most understated objective. Institutionalisation. Listing forces a founder-led business to slowly become a professionally governed organization. Quarterly disclosures. Annual reports. Independent directors. Shareholders. Governance. In hindsight, this decision probably prepared Wealth First for everything that followed over the next decade.

Between 2002 and 2016, Wealth First wasn’t building a distribution business. It was quietly building an operating system. An operating system centered around relationship managers, education, trust, asset allocation, process, simplicity, and long-term behavior. These would eventually become the foundations upon which every future business. Mutual funds, insurance, PMS, and eventually Lakshya AMC would be built. At the time, almost nobody outside the company would have recognized what was happening. But the first two Ts were now firmly in place. Time. And increasingly, Trust. The third T, the biggest one, was about to arrive. Now we reach the phase where, in my opinion, the story of Wealth First really begins. Until now, the company had spent almost twenty-five years building Time and Trust. From here onwards, India itself begins contributing to the Tailwind.

Phase III- Tailwind When India Changes Faster than Wealth First [2016-FY26]

We often assume that multibaggers become multibaggers because the company suddenly discovers something extraordinary. More often than not, the company remains largely the same. It is the world around it that changes. I was reminded of the story of the Eddystone Lighthouse, something I had written about while studying Max India. The lighthouse didn’t become stronger because someone rebuilt it every year. The lighthouse remained where it was. The sea changed. The shipping routes changed. Trade increased. Ships became larger. Eventually, the value of that lighthouse increased dramatically. The lighthouse did not change overnight, but the world around it did. I think Wealth First is a similar story. Between 1992 and 2016, Wealth First had patiently built credibility. Then, almost quietly, India entered one of the greatest financial transformations in its history. The biggest tailwind probably wasn’t the stock market. It was financialization. For decades, Indian households largely preferred fixed deposits, gold, and real estate. Gradually, that started changing. Mutual funds became mainstream.

Covid crash was like a shot in the arm for the Indian financial industry. Demat accounts exploded. SIPs entered middle-class households. Financial awareness increased. Professional wealth management slowly became acceptable. Exactly the kind of business Wealth First had been patiently preparing for since 1992, it suddenly found itself operating in a much larger market. Asset allocation. Estate planning. Long-term relationships. This played directly into Wealth First’s strengths. Wealth First embraced technological advancement. Digital execution. Demat transactions. Online reporting. Centralized research. Automated processes. I recently wrote about another listed business that is benefiting from this tailwind.

DAM Capital Advisors: A deep Dive

For a long time, scientists believed that the human brain was largely developed by early childhood. That what we became was decided early, and the rest was just time passing. It turns out that assumption was incomplete. When researchers began using MRI scans to study the brain over time, they discovered that one of its most critical regions, the Prefron…

Let’s come back to Wealth First. Technology, rather than replacing relationship managers, made them significantly more productive. The result was operating leverage. The company could serve more families without a proportional increase in manpower. Wealth First knew that trust itself had become an asset. Clients who trusted them for bonds now trusted them for mutual funds. Clients who trusted them for mutual funds trusted them for complete wealth management. Eventually, management realized something profound. If clients trust us with their financial lives, why stop at wealth management? That thinking eventually led to a few large new initiatives.

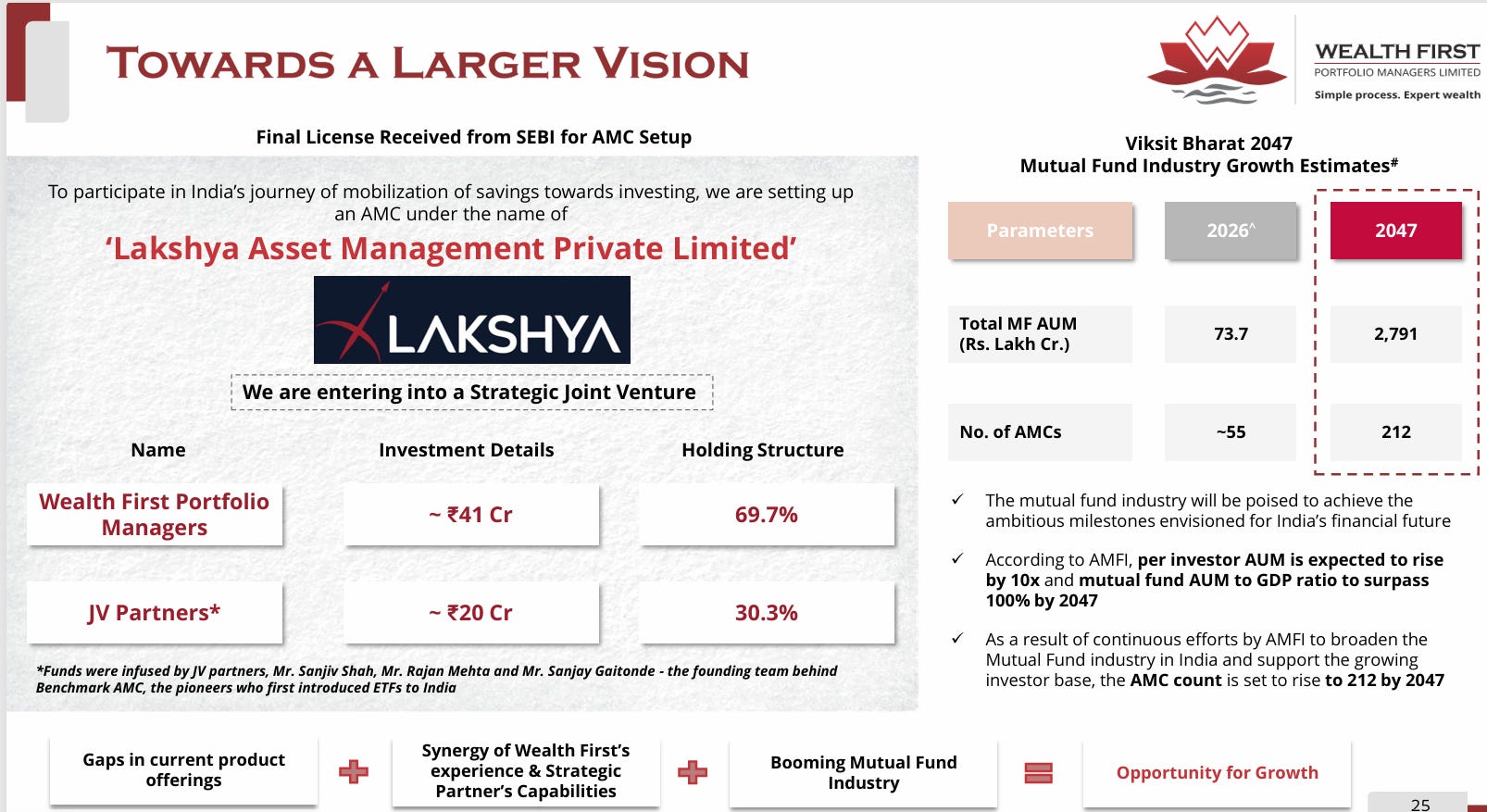

Lakshya AMC

The biggest milestone of FY26 was the launch of Lakshya Asset Management. Wealth First received SEBI’s final approval within just 14 months of applying, reflecting the seriousness and preparation behind the initiative. More importantly, it marked the company’s transition from merely distributing financial products to manufacturing them, laying the foundation for its next phase of long-term growth.

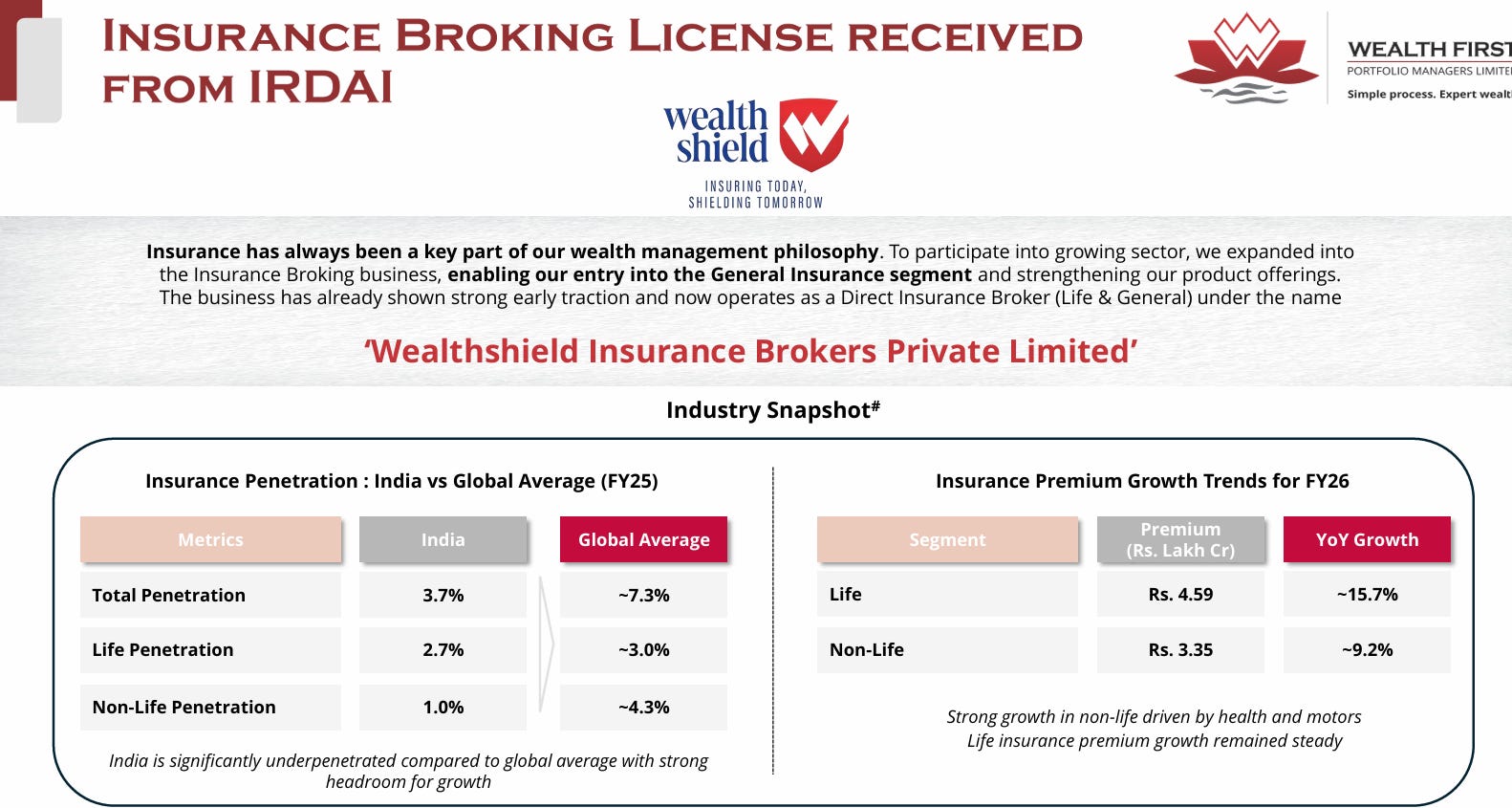

WealthShield Insurance

FY26 also marked Wealth First’s formal entry into insurance through the launch of WealthShield Insurance Brokers. Rather than treating insurance as a standalone business, management is building it on two complementary engines: cross-selling life, health, and motor insurance to its existing wealth management clients while simultaneously creating a dedicated B2B distribution network. The objective is simple: deepen client relationships and increase wallet share without moving outside the company’s core competence.

NRI PMS

The company also launched an index-based Portfolio Management Service (PMS) for NRIs in the US and Canada. Instead of creating another stock-picking product, Wealth First chose a simple, index-oriented solution to address a specific gap faced by overseas Indian investors. It reflects the company’s broader philosophy of solving niche problems with simple products rather than competing in crowded segments.

Potential acquisitions of aging IFAs and MFDs

Management also hinted at evaluating acquisitions of aging Independent Financial Advisors (IFAs) and Mutual Fund Distributors (MFDs) who have built strong client relationships over decades but lack succession. More than acquiring assets, the strategy appears to be aimed at earning trust, allowing Wealth First to expand its client base through culturally aligned firms that share its long-term, relationship-driven approach.

Notice something. None of these businesses is a random diversification. Each one of them sits adjacent to the trust Wealth First had already built. If someone had looked at Wealth First in 2017, they might have concluded that it was simply a company distributing fixed-income products. Today, I think that description would completely miss the point. Wealth First is no longer just a wealth manager. Nor is it merely a distributor. It is gradually becoming a financial relationship powerhouse, using the trust earned over three decades to solve a wider set of financial problems for the same client. That, in my opinion, is the real transformation. The philosophy hasn’t changed. The products have. The opportunity has. India has. And with that, the first three Ts now stand complete.

Time. Trust. Tailwind. But are those three enough? History suggests they are not. There is still one final T you and I must evaluate. Let me come to that.

Imagine meeting Warren Buffett for the first time in the year 1995. He had already spent decades investing. He had already earned enormous trust. He had perhaps benefited from one of the greatest economic tailwinds in history, the rise of post-war America.

Time? Exceptional. Trust? Unmatched. Tailwind? Extraordinary.

And yet over the last twenty-five years, how many times have investors declared that Buffett had “lost his touch”? Every prolonged period of underperformance has produced fresh headlines. Nothing fundamental about Buffett’s character changed. What changed was the fourth T. Track record. We don’t merely judge businesses by who they are. We judge them by what they have done lately. That is simply human nature. Which brings me back to Wealth First.

Wealth First has already demonstrated an impressive track record in building a wealth management business. But today, the company is asking investors to believe in something much larger. An AMC. An insurance broking platform. Index-based PMS. Potential inorganic acquisitions. New product innovation. These businesses have not yet earned their own long-term track records. They have vision, leadership, capital, and intent. But investing ultimately rewards execution. The fourth T can only be built with time. No presentation or conference call can create it. Only years of consistent execution can. And that is exactly where Wealth First stands today.

When Wealth First listed on the SME platform, it was incredibly hard, almost impossible, to envisage where it would be in FY26. And I believe it is equally hard to envisage it for the next 5 years. Today, the stock is roughly 40% below its all-time high of December 2024 and trades at around 27 times trailing earnings. Valuation is no longer the simple story. Execution is. If I look at the business purely through the lens of the first three Ts, my conclusion is fairly straightforward.

Time? Passed with distinction. Three decades of patient institution building.

Trust? Again, passed with distinction. Thousands of families, recurring revenues, referral-led growth, and a culture that consistently puts clients before products.

Tailwind? Same distinction. India’s financialization journey is probably still in its early innings.

But now comes the difficult part. The businesses that will determine Wealth First’s next decade, Lakshya AMC, WealthShield Insurance, PMS, future acquisitions, and new product innovation have not yet built their own long-term track records. That is where the next chapter begins. The interesting thing about investing is that markets rarely pay you for what you have already built. They pay you for what you are capable of building next. Perhaps that is why Wealth First feels so different today than it did when I first looked at it years ago. Whether Wealth First becomes another remarkable long-term compounder or merely remains a well-managed wealth management company will, in my opinion, depend far less on the first three Ts than on the fourth. Track Record. Only time will write that chapter. Until then, I think Wealth First deserves neither blind optimism nor casual dismissal. It deserves patient observation. Because the most important part of its story may still be ahead of it. Hence, it rightfully deserves its place in my watchlist. Do you think this 4T Framework works across all fields? Let me know in the comments. Thanks for reading.

P.S. Know more about Zen Nivesh and our origin story here.

| A guest post by

|

Hi Ankit bhai, you made this look incredibly easy but the hard work behind it is clear. Thank you for the jargon free article.

It was a great article sir, But the point to note is market have still not considered the acquisition, moreover, the strategy of inorganic acquisitions, helps to build AUM going ahead and they also indicated to double by 2029-30 , implying 17% CAGR, what I liked about the AMC business of theirs is their legacy partners are coming together and when such pedigree comes , T- time , T- trust gets an extra edge, the third T is i am keen to watch is Tailwind , overall there is tailwind in the industry but better mutual funds are hardly there, so time for test and observation.