Solara Active Pharma Sciences: The Reset

ZN Playbook #5 | Research Lab #24

Every once in a while, markets hand you a setup that looks linear, but if you tilt your head a little, the payoff is convex.

In investing, convexity is about owning outcomes where the downside is protected but the upside can be disproportionately large. Most investors chase linearly growing earnings; however, looking for inflection points where the business model itself tilts -that’s where the money is.

And that’s why turnarounds and special situations are fascinating. They often come dressed in accounting losses, corporate restructurings, demergers and business shift.. But hidden beneath, you can sometimes find a high-quality core business waiting for the fog to clear.

At Zen Nivesh, this is the kind of setup we love to study and discuss in our Zen Investing Club.

Our regular readers would be aware that we’ve covered 4 pillars of the ZN Playbook here:

A. Yard Investing

B. High Convexity & Restructuring/Turnaround

C. Special Situations

D. Deep Value

We’ll soon be launching our advisory service. To stay updated and be among the first to know when we go live, you can join the waitlist here:

This is what we do at Zen Nivesh - whether it be on Substack or our Zen Investing Club Platform.

Think of it as a lab where ideas with asymmetric potential are dissected, challenged, and sharpened.

And yes, sometimes the membership can unlock as much value for your investing journey as the stock itself!

We are running a Festive Season Offer where you will get our Zen Investing Club annual Membership for only Rs. 7500 (Instead of Rs. 12000). Get a glimpse of our club here:

Use code: FESTIV

This offer is valid till October 23, 2025 only!

So. Back to the blog. The company I’m going to cover this week is Solara Active Pharma Sciences Ltd.

Why We’re Looking at Solara Active

In Rajasthan’s desert, you’ll find the khejri tree.

to the people of Thar Desert! A nature's wonder indeed! #StateSymbols . #rajasthan #rajasthantourism #")

It doesn’t look impressive at first sight. Short, thorny, often half-dry. But it’s called the “kalpavriksha of the desert” because it survives where almost nothing else can. Its roots go deep to find water, its leaves feed cattle, its pods are eaten by people, and even in droughts, it keeps giving.

The khejri teaches a simple lesson: survival is often more important than speed.

Trees that grow fast in good years may fall when the rains stop, but the khejri endures, and over time, its value compounds for the entire ecosystem.

Investing in beaten down and ignored stocks feels the same. The easy pick is the tall, green tree with shade and fruit already visible. But the more interesting and sometimes rewarding pick is often the scarred tree that has proven it can survive a drought. If it can endure the bad times, it usually thrives when conditions turn.

Solara Active Pharma is our khejri tree today. It faced its drought years - overdependence on ibuprofen, pricing collapse, high debt. The company looked dry on the outside. But the roots remained strong: global approvals, trusted customers, manufacturing capacity, and above all, a promoter who has a track record of rebuilding.

The reset Solara has taken - cutting costs, pruning weak products, reducing debt, and now preparing a demerger - is like a tree redirecting water to its strongest roots. If it succeeds, growth will come back stronger, and the market will revalue it not as a dried-up shrub, but as a resilient compounding tree.

The Promoter’s Journey - Arun Kumar Pillai

If Solara is the khejri tree, then Arun Kumar is the farmer who has planted and replanted orchards in difficult terrain. His career in pharma is a study in resilience and reinvention.

In 1990, he founded Strides Pharma, a small formulations company out of Bangalore, and built it into a global generics powerhouse. At a time when Indian pharma was still finding its feet in regulated markets, Arun pushed Strides into complex generics and oncology. The risks were large, but so were the payoffs - which materialized when Arun sold Strides’ injectables arm, Agila Specialties, to Mylan for $1.65 billion in 2013-14.

Source: Mint

It was one of the landmark pharma deals of the decade and created massive shareholder wealth. That single move showed Arun’s style: he’s not afraid to cash in value when the timing is right, even if it means parting with what looks like the crown jewel.

Then came SeQuent Scientific, where he took a neglected platform and turned it into India’s largest animal health company. Again, he scaled it rapidly and eventually sold control to Carlyle.

Source: Mint

It was another example of his playbook — build, scale, exit when value is unlocked, and move on to the next frontier.

Not many know but Solara’s story really begins decades earlier with Shasun Chemicals, a Chennai-based API maker best known for ibuprofen. Shasun built scale and credibility in the bulk drug space., eventually merging with Strides Arcolab in 2015 to form Strides Shasun.

In 2017, Arun Kumar carved out the API businesses of Strides and SeQuent into a standalone entity.

The logic was simple: APIs are the foundation of pharma, and being a pure-play API company would give Solara scale and focus. The first few years went well, but soon storms hit. Solara leaned too much on ibuprofen, a commodity API. Prices collapsed, new competition arrived, and debt swelled.

Many promoters would have doubled down or masked the problem with accounting. Arun did the opposite — he pressed reset. In FY25, Solara raised fresh equity via rights issue, cut debt, exited low-margin contracts, and began preparing a demerger of its CRAMS and polymer business. In other words, he pruned the dried branches to protect the living core.

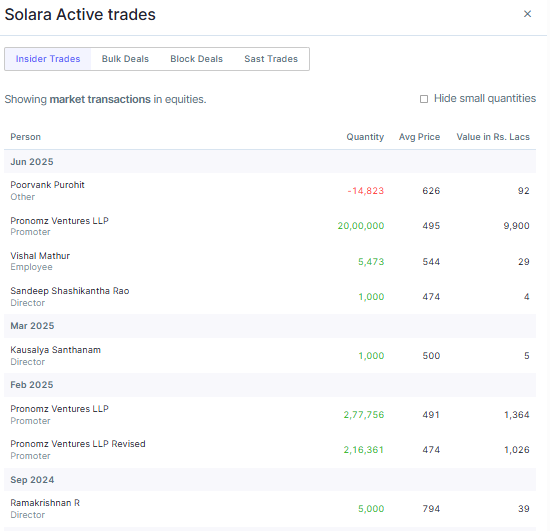

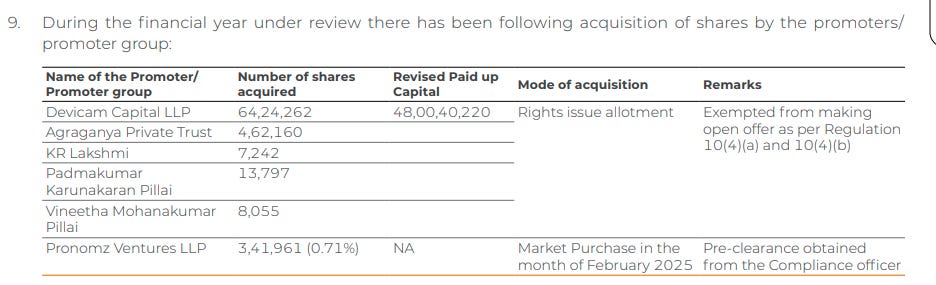

Importantly, Arun has kept skin in the game. As of June 30, 2025, the promoter group holds 42% of Solara’s shares. That meaningful ownership ensures his interests are tied with ours — he wins only if shareholders win.

Interestingly the promoter group has been buying heavily from the open market!

Anyhow. It’s not a flawless track record. Investors who rode with him through every cycle know the volatility.

But it’s also a story of boldness: of a promoter unafraid to take risks, unafraid to admit mistakes, and determined to create value in new forms.

That’s why promoter pedigree matters here. With Arun, you’re not betting on a smooth ride. You’re betting on someone who has repeatedly shown he can guide a company through drought years, just like the khejri tree survives in the desert.

The Business of Solara Active

Every village has that one shop everyone depends on. It doesn’t sell finished products with shiny packaging; instead, it sells the raw ingredients. You buy rice, flour, spices — and turn them into meals at home. The shop is indispensable to the community. Isn’t it?

In global pharma, Solara Active Pharma is that shop. It doesn’t sell branded pills or capsules you see in pharmacies. Instead, it makes APIs - Active Pharmaceutical Ingredients, the raw material that every medicine is built on. And it is one of the largest API players in India.

Source: Annual Report FY25

Catalogue APIs - A Library of Molecules

Solara runs what’s called a catalogue API business. Think of it like a library or a seed company. Instead of a single product, it maintains a catalogue of 60+ APIs (with an additional 10 under active development) across multiple therapeutic areas — pain management, CNS (central nervous system), anti-infectives, anti-malarials, and more.

When a global pharma company wants to make a generic drug, it can “pick” the right API from Solara’s catalog. This is not one-off or custom work; it’s steady, repeat business. Once a customer is linked to Solara’s catalog, they often stick for years.

Why 95+ DMFs Matter?

Here’s where Solara’s strength shows: it has filed 95+ Drug Master Files (DMFs) with the US FDA.

Source: Q3FY25 Investor Conference Call Transcript

A DMF is like the secret recipe of an API. It details how Solara makes that molecule, how it controls quality, and how it meets regulatory standards. Pharma companies in the US or Europe can simply reference Solara’s DMF when filing for approval of their finished drug.

This creates two advantages:

Stickiness - Once a customer builds their drug approval around Solara’s DMF, switching suppliers is costly and time-consuming.

Credibility - Having 95+ DMFs shows Solara isn’t a small shop; it’s a serious global supplier trusted by regulators and pharma giants alike.

The Shift Beyond Ibuprofen

For years, ibuprofen was Solara’s calling card. At one point, it made up ~50% of revenues. But when competition intensified and prices collapsed, ibuprofen became a burden.

Today, Solara has consciously reduced its dependence. Ibuprofen (plain + derivatives) now contributes closer to 30% of revenues, and management is focusing more on specialty APIs and ibuprofen derivatives where margins are healthier.

Source: Q1FY26 Investor Conference Call Transcript

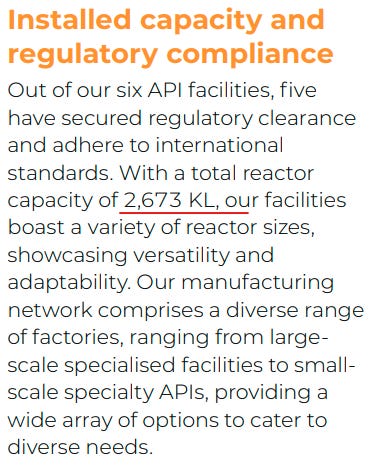

Manufacturing & R&D Backbone

Behind the catalogue are six manufacturing sites in India, five of which carry approvals from regulators like the USFDA and EU GMP. Combined, they offer 2,600+ KL reactor capacity,

Source: Annual Report FY25

currently running at ~60 - 65% utilization - leaving plenty of headroom for growth without heavy new capex.

Source: Q1FY26 Investor Conference Call Transcript

Supporting this is Solara’s R&D hub in Chennai, with 60+ scientists constantly refining processes and developing new APIs. This is where new catalog entries come from — niche chemistries, complex APIs, and polymers that can drive future growth.

Source: Annual Report FY25

What Went Wrong?

In its early years, Solara was the market’s darling. The timing couldn’t have been better. Covid had turned APIs into a matter of national security. Countries wanted local, reliable sources of pharma raw materials, and India was positioned as the natural alternative to China.

Source: Researchgate

Solara seemed born for the moment.

And they had the capacity. With >5,000 MTPA of ibuprofen capacity, Solara operated one of the largest single-location ibuprofen facilities in the world. Demand was roaring, prices were firm, and the company was scaling aggressively.

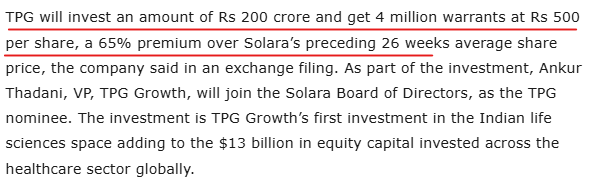

The promoters, along with private equity giant TPG in 2019 came together to back this growth.

Source: Times of India

Together they infused about ₹460 crore through warrants (Promoter Group at about Rs. 400/Share and TPG at about Rs. 500/Share),

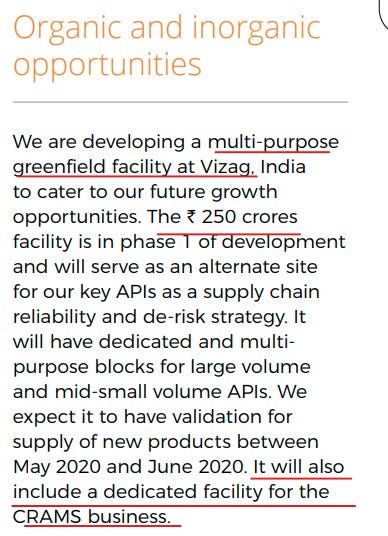

and Solara embarked on a heavy capex cycle. A massive new multi-purpose greenfield facility in Vizag (3,600 MTPA) was announced. The idea was clear: ibuprofen would be the growth engine, and Solara would ride the global wave. And mind you - other Indian API peers were also expanding.

Source: Annual Report FY20

A merger with the promoter entity Aurore was announced, with an intention to add more API products and a CRAMS pipeline to Solara’s basket.

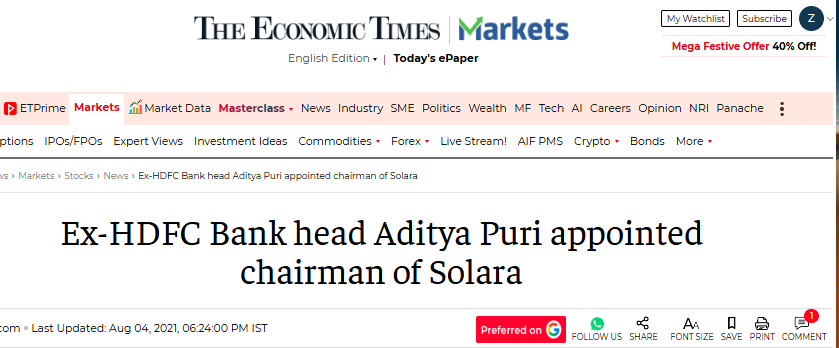

To crown it all, Aditya Puri, the legendary former HDFC Bank CEO, was appointed Chairman, lending credibility and vision.

Everything pointed to a company poised for greatness.

And in 2021, the financials peaked. Revenues, margins, and valuations all reached their highs. Investors believed Solara was becoming a global API powerhouse.

But just as the new capacities and the merger came online, the tide turned. Post-Covid, demand for ibuprofen collapsed.

Source: Chemanalyst

Supply, on the other hand, had exploded — not just from Solara but from every competitor that had expanded.

Source: BizzBuzz

Source: Indiapharmapost

Prices fell off a cliff.

To keep its new plants running, Solara was forced to sell into less-regulated markets, where prices are lower and working capital requirements are much higher. Oversupply also led to dumping in global markets. The problem? Solara’s cost structure had been built for regulated markets — higher compliance, higher costs — which made competing in unregulated markets painful.

Things went downhill fast. Margins evaporated.

Debt piled up.

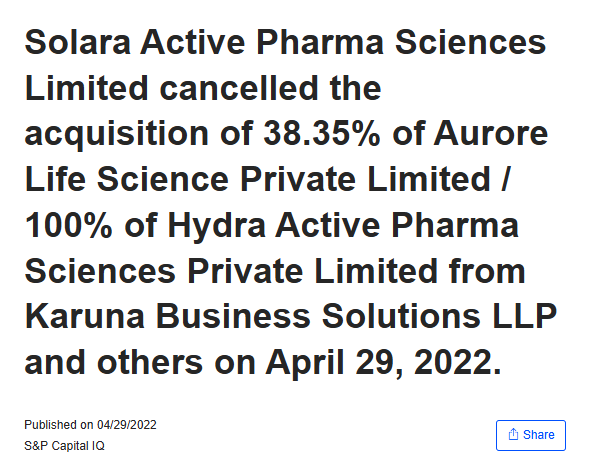

Aurore merger called off.

Source: Marketscreener

Investors lost faith. Solara’s stock was punished, down heavily from its highs.

What was once pitched as a niche API champion looked like just another commodity pharma player caught in a storm.

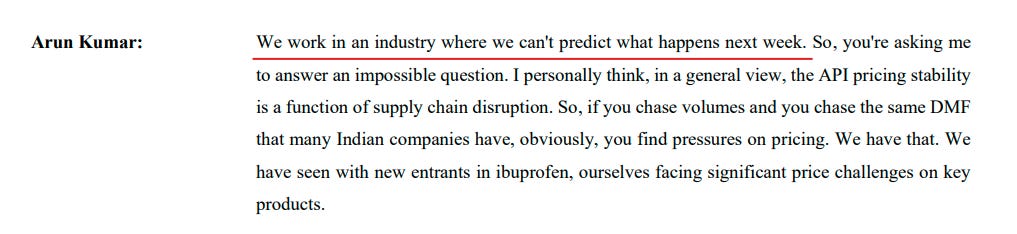

Fooled by Randomness.

In Arun’s own words - It’s the nature of the industry unfortunately: (Oct 24 Transcript)

The Course Correction & What’s Happening Now?

Every turnaround story has a moment of honesty. For Solara, that moment came when Arun Kumar returned to the investor call in 2024 and admitted that the company had gotten it wrong.

Source: Q3FY24 Investor Conference Call Transcript

The ibuprofen bet, which once looked like a crown jewel, had become a weight dragging the company down.

Admitting failure is rare in Indian corporate culture, but it was also the beginning of Solara’s reset. The company stopped chasing revenue for the sake of scale.

The reset meant withdrawing the unregulated market, even if it meant lower sales in the short term. From now on, Solara would only supply regulated customers - the ones in the US, Europe, and Japan - who may order less, but pay better and stay longer.

Nevertheless, it’s worth noting that Japan is one of the toughest pharmaceutical markets in the world - in many ways more stringent than even the United States. Regulatory approvals there demand absolute precision, consistency, and patient safety, with very little margin for error. The fact that Solara has been able to establish a presence in Japan is significant. It shows that the company’s processes and quality systems can withstand scrutiny at the highest global standard.

Cleaning the balance sheet was the next step.

In 2025, Solara launched a rights issue — essentially asking existing shareholders, including the promoter, to put in fresh money. Promoters participated in the issue, signaling his skin in the game. The proceeds went straight into reducing debt.

Source: Annual Report FY2025

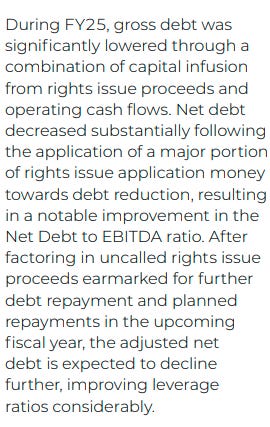

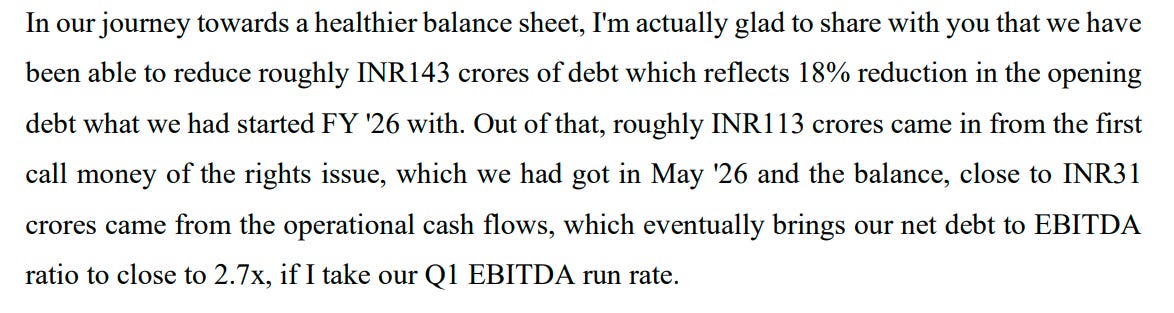

Borrowings, which had ballooned to nearly ₹1,000 crore at their peak, fell to around ₹800 crore by March 2025. By the first quarter of FY26, debt had been cut further by another ₹144 crore (113cr Rights Issue Proceeds and 31 Cr. from OCF). For a company once choked by leverage, this was a big relief.

Source: Q1FY26 Investor Conference Call Transcript

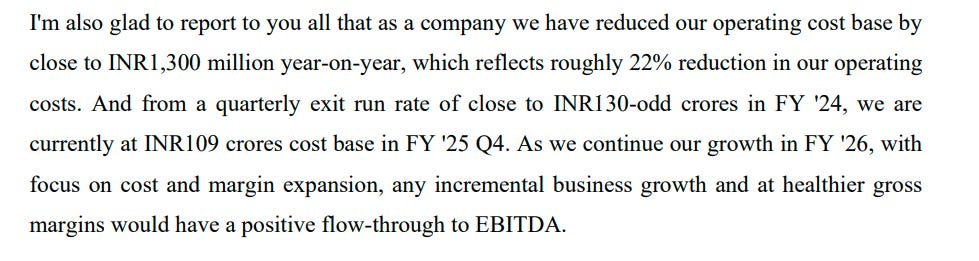

At the same time, Solara trimmed its operating costs. Think of it like a household tightening its belt after a rough year - cutting discretionary spending, negotiating better rates, and making do with less.

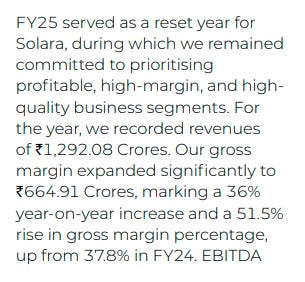

Solara shaved off about ₹130 crore in costs, a 22% drop, by streamlining operations and improving procurement. That cost discipline, combined with better pricing from regulated markets, is what allowed gross margins to recover.

Source: Q4FY25 Investor Concall Transcript

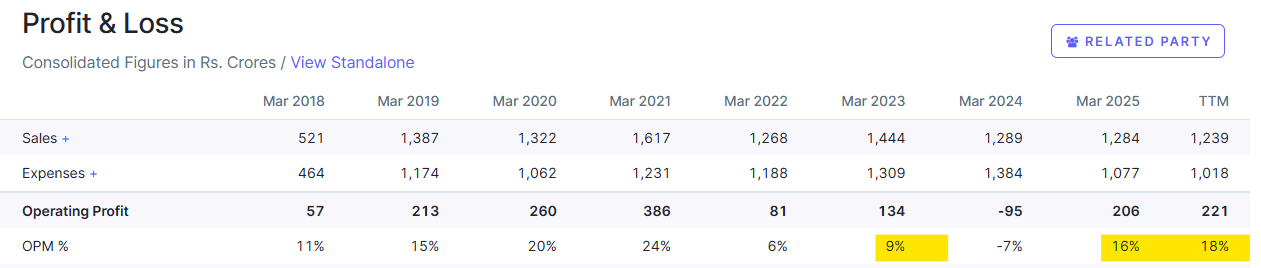

After sinking to just 37.8% in FY24, gross margins rebounded to 51.5% in FY25 and touched 54% in Q1 FY26.

Source: Annual Report FY2025

Source: Q1FY26 Investor Conference Call Transcript

After a prolonged period of musical chairs, the leadership was refreshed too. Arun, who had always been a hands-on promoter, stepped back into a non-executive role.

A professional management team took charge - Sandeep Rao, a veteran from Biocon and Mylan, became CEO, and Sarat Kumar from BioCina became CFO.

Source: Annual Report FY2025

Governance was strengthened further with experienced board members like Manish Gupta (Jagsonpal Pharma) joining as independent directors.

Source: Annual Report FY2025

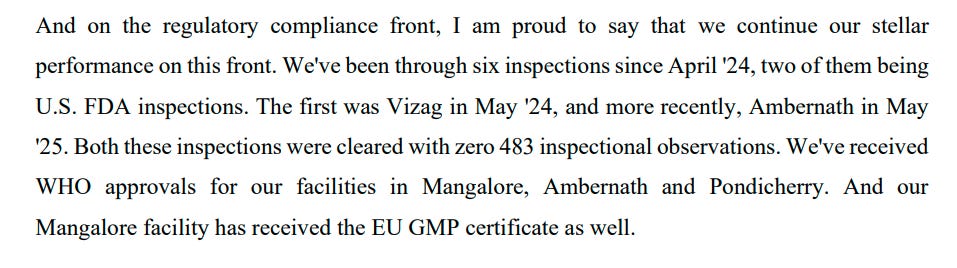

Regulatory credibility, long Solara’s hidden strength, was also reaffirmed. In pharma manufacturing, a single bad inspection from the US FDA can set a company back years. Solara’s sites at Vizag and Ambernath went through rigorous inspections and emerged with “zero 483s” - meaning no critical observations. That gave Solara the license to sell into the world’s toughest markets again, which in turn reinforced customer trust.

Source: Q4Fy25 Investor Concall Transcript

The impact of these course corrections is now visible in the numbers.

EBITDA, which measures operating profit before financing costs, swung from a loss of 7% in FY24 to a positive 16.5% margin in FY25.

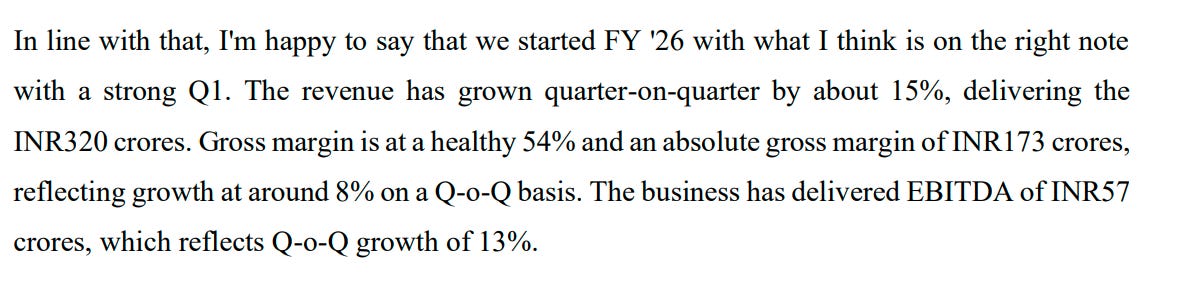

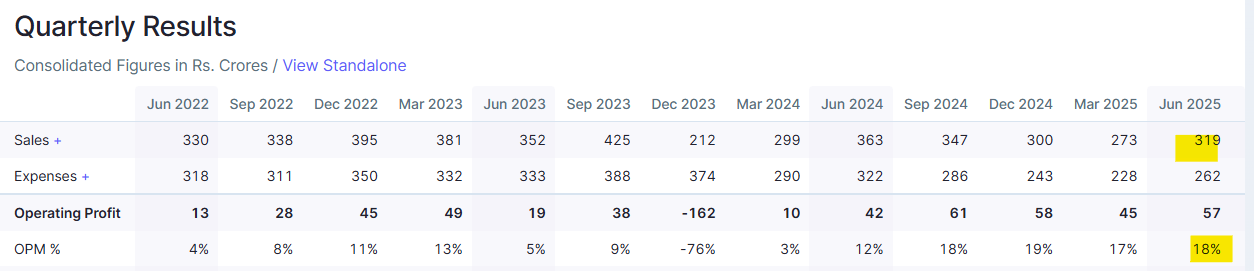

In Q1 FY26, EBITDA margins climbed further to 18%, the best in twelve quarters. Revenue in the same quarter was ₹320 crore, but what mattered more was that Solara delivered its highest net profit in three years.

Debt, once the company’s Achilles heel, is now trending towards a net debt-to-EBITDA ratio of under 1.5x, something unthinkable two years ago.

On the business side, ibuprofen is still important, but its dominance has been cut. Once half of Solara’s revenue, it now contributes closer to 30%.

Within that, plain vanilla ibuprofen - a commoditised product prone to price wars - makes up about 21%, while more complex derivatives and salts contribute 9%.

Source: Q1FY26 Investor Conference Call Transcript

These derivatives are harder to make, fetch better prices, and are less prone to dumping. Solara’s decision to tilt towards these higher-value forms is a subtle but crucial change.

Beyond ibuprofen, Solara is finding niches where competition is scarce. Its polymer APIs are one example. Few global players can make pharma-grade polymers, but Solara has developed expertise here and already supplies nearly every US generic company filing for polymer-based drugs. This scarcity creates pricing power, a rare commodity in the API world.

Then there is CRAMS - Contract Research and Manufacturing Services. To explain it simply: the catalogue API business is like running a grocery store. You stock common items like ibuprofen or gabapentin and sell them repeatedly. CRAMS, by contrast, is like running a custom kitchen. Customers - often big pharma companies - bring their recipes, and you cook for them under strict quality rules.

These contracts are sticky and pay better, but they take time to win because customers want proof of capability and reliability. That’s why CRAMS is often compared to a bamboo tree - years of invisible root-building, then sudden visible growth once the roots are strong.

Solara is laying those roots now.

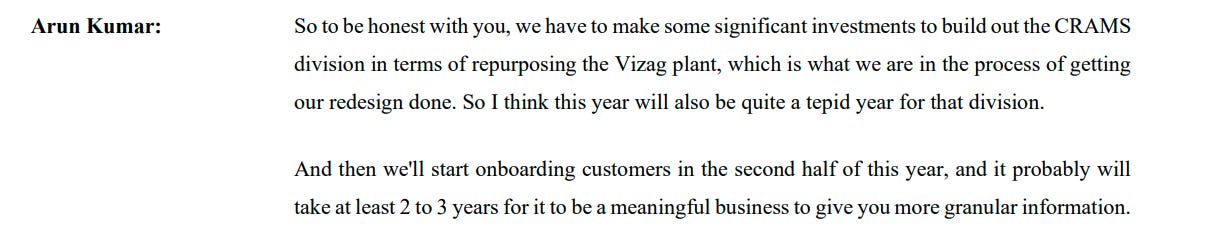

Vizag is now being converted into a multipurpose facility that can handle complex chemistries for innovator pharma companies. The retrofitting into a multipurpose and high-potency API (HPAPI) facility for CRAMS and other specialty molecules is expected to complete in FY26, with the plant gradually coming back online in the second half of the year.

Source: Q1FY26 Investor Conference Call Transcript

By management’s guidance, Vizag will contribute modestly from FY26 itself, but the real ramp-up will take 2 - 3 years - the time needed to win customer trust, qualify processes, and lock in sticky contracts.

For the moment, CRAMS is small — about ₹100 odd crore in revenue - but management believes it can grow four to five times over the next few years as customers diversify away from Europe and Taiwan.

Sources: Q1FY26 /Q3Fy25 Investor Concall Transcripts

The geopolitics help here: with Europe too costly and Taiwan overshadowed by China tensions, global pharma wants to de-risk by sourcing from India. Solara wants to be ready when that shift accelerates.

So where does that leave us today? Solara is no longer the broken yard it was in FY23. It’s not showroom-perfect either. It is, instead, in the messy middle — a business that has pruned its dead branches, is nurturing new shoots, and is waiting for the bamboo to grow. Margins are back above 50%, debt is falling, leadership is steadier, and optionality exists in polymers and CRAMS.

The Demerger - When 2 + 2 > 4

Now, in investing, one of the oldest lessons is that the whole is not always greater than the sum of its parts. Sometimes, the opposite is true: two businesses tied together can drag each other down, but once separated, each can thrive on its own. Analysts call this “conglomerate discount.” Investors simply call it confusion: when one division is fast-growing and another is struggling, the market struggles to price them fairly, and both end up undervalued.

That is exactly the case with Solara today.

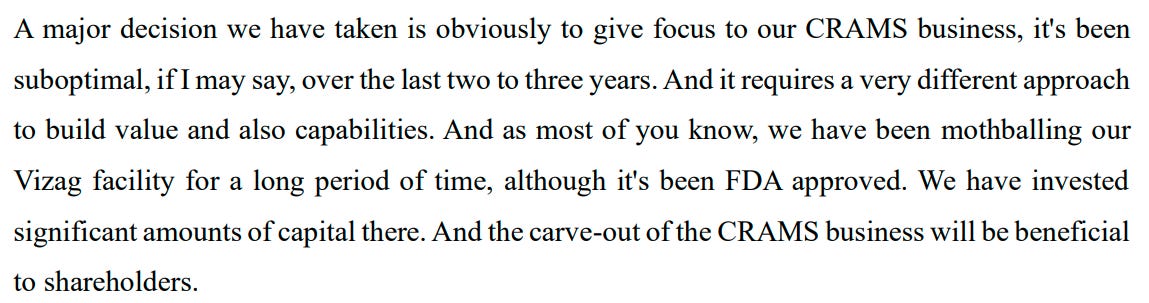

For years, Solara has run two very different businesses under one roof. The first is the catalogue API business, a steady but competitive segment where gross margins hover in the 53 - 55% range — and only if the company resists selling more plain vanilla ibuprofen.

The second is the CRAMS and polymer segment, a higher-end play where gross margins can reach 65%, with EBITDA margins in the 25 - 30% band. The challenge is that CRAMS has been running sub-optimally for the past two to three years. It has different research demands, different customer cycles, and different economics compared to the catalogue API business. Lumping them together blurred the picture and slowed progress.

And generally, as it is the case with CRAMS - the gestation period is very high which can suppress the ROCE of the business.

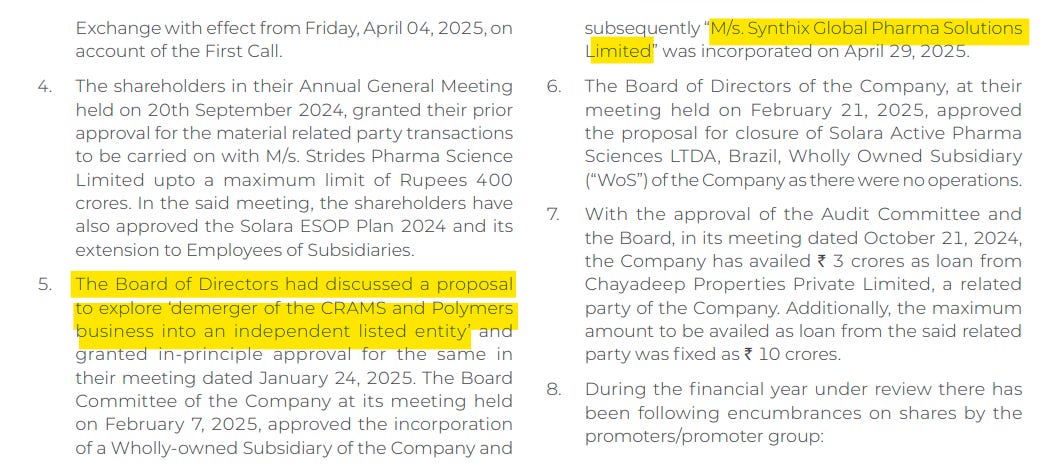

In April 2025, Solara’s board took the bold step of separating them. A new entity, Synthix Global Pharma Solutions Ltd, was incorporated to house the CRAMS and polymer operations.

Source: Annual Report FY2025

Vizag - the mothballed facility now being retrofitted for CRAMS — will be moved into Synthix. So will about ₹200 crore of debt, which immediately lightens the balance sheet of the parent Solara.

Source: Q1FY26 Investor Conference Call Transcript

What remains in Solara is a cleaner, sharper catalogue API company with lower leverage, steadier margins, and simpler capital allocation.

The rationale is clear: give each business the independence and focus it deserves. The catalogue business can concentrate on widening its molecule library, expanding into regulated markets like Japan, and improving realizations per KL. CRAMS and polymers, meanwhile, will have the space to invest heavily in scientists, customer development, and high-potency chemistries without being held back by the cash flow cycles of ibuprofen and other bulk APIs.

This separation is not just cosmetic. It addresses real inefficiencies:

Optimized costs: CRAMS requires different R&D intensity and customer engagement. With its own management, it can spend where it matters without dragging API economics.

Improved efficiency: Vizag will no longer sit underutilized; it will become the flagship asset of Synthix.

Better asset turns: Pushing assets and debt into Synthix means the remaining Solara can generate better returns on capital with its lighter balance sheet.

Valuation clarity: Investors can now value a high-margin CRAMS play separately from a catalogue API player. Instead of one blended multiple, each can be judged on its own merits.

Management framed it simply on the call: the demergerwill be beneficial to shareholders

Source: Q3Fy25 Investor Concall Transcripts

For investors, this is a classic special situation setup. The API business will get rerated closer to its pure-play peers once it is no longer weighed down by CRAMS losses and Vizag under-recoveries. CRAMS, though still small today (~₹100 crore revenue), will be treated as an early-stage growth story with higher margin potential and optionality.

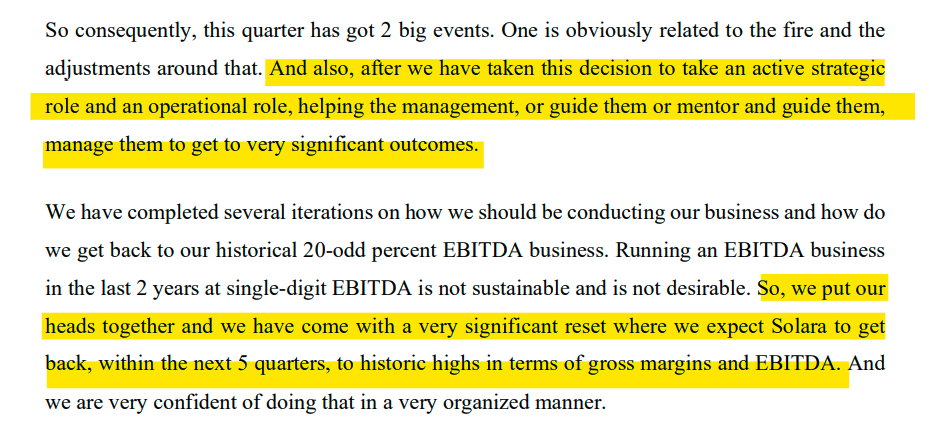

It is, in short, a chance for 2 + 2 to become more than 4. Will the math work, it remains to be seen as the promoter himself has said:

The Risks - Where Things Could Go Wrong

Every turnaround and special situation comes with risks. With Solara, they aren’t hidden - management themselves have spoken about them on calls. As investors, acknowledging these risks is just as important as spotting the upside.

The first and most obvious risk is Vizag. The plant has been mothballed, retrofitted, and repositioned as the centerpiece of the CRAMS strategy. But timelines in pharma are notoriously slippery. Even though management expects Vizag to restart in the second half of FY26, customer qualification and revenue traction could take longer. If commercialization is delayed, the margin recovery story may not flow as quickly as the market expects.

The second risk is CRAMS execution. Customers are cautious, qualification periods are long, and competition from larger Indian CDMOs is real. Today, CRAMS contributes barely ₹100 crore in revenues. If it doesn’t cross the ₹200 - 300 crore threshold in the next few years, it will remain sub-scale, weighing on returns instead of enhancing them.

The third risk is product traction in high-margin APIs. Solara has made smart moves into ibuprofen derivatives, polymers, and even early work in peptides and oligonucleotides. But these bets need commercial traction. If they fail to gain customer acceptance, sales per KL won’t rise, and the catalogue business will remain hostage to commodity APIs.

Then there is the lingering ibuprofen volatility. Even though Solara has cut exposure from 50% of revenues to ~30%, plain ibuprofen still makes up a fifth of the topline. This market remains oversupplied globally, with Chinese capacity keeping prices low. If pricing weakens further, it could dent quarterly numbers and investor sentiment, even if the long-term strategy is sound.

Lastly, one cannot ignore regulatory risk. Pharma is binary when it comes to inspections: a clean audit earns you trust and markets, while a single adverse finding can lock a facility out for months. Solara’s track record has improved recently, with zero-483 outcomes at Vizag and Ambernath, but in this industry, the next inspection is always around the corner.

In short, Solara is not without its potholes. The reset has steadied the car, but the road ahead will still have bumps. Investors must size positions accordingly, and remember that while convexity offers upside, execution risk remains the toll you pay on this journey.

Valuation & Investor Takeaways

Valuing a company like Solara is not about putting the perfect price tag on it today, but about asking: what is the base case if nothing extraordinary happens, and what is the upside if even part of the optionality plays out?

The Base Case - Catalogue APIs (Core Solara)

The management has guided for gross margins in the 53 - 55% range and EBITDA margins in the high teens to ~20% as a steady-state outcome. At present, Solara is running at about 60 - 65% utilization across its 2,600+ KL capacity. Without major new capex, this can support revenues of roughly ₹2,500 crore over time. With current FY26 revenue guidance at ~₹1,400 - 1,500 crore, that means the company is still operating at a conservative baseline.

If we assume Solara reaches ₹2,000 crore revenue in 3 - 4 years, with 18 - 20% EBITDA margins, that’s about ₹360 - 400 crore of EBITDA. Even if we apply a modest 10x EV/EBITDA multiple (in line with Indian API peers, and below global CDMO valuations), that suggests an enterprise value of ₹3,600 - 4,000 crore. Deducting today’s net debt of ~₹500 crore (headed toward <₹300 crore in two years as finance costs fall), equity value would still leave upside from current levels.

This is the conservative base: a steady catalogue API player, debt-light, with margins restored. No heroics required.

The Optionality - CRAMS & Polymers (Synthix)

CRAMS today is barely ₹100 crore revenue, but with ~25 - 30% EBITDA margins when projects scale. Management has said that Vizag, once retrofitted, can become a ₹400 - 500 crore business in 3 - 4 years. Let’s not assume the best. Even if Synthix gets to ₹300 crore revenue by FY29, at 25% margins, that’s ₹75 crore EBITDA. Apply a conservative 12x multiple (below global CDMO comps, which trade 15 - 20x), and you get ~₹900 crore of value.

Polymers are smaller but strategic. Since there are few global competitors, scarcity gives pricing power. Even if this segment adds ₹100 crore of incremental high-margin revenue, it could lift realizations per KL significantly.

But again, let’s keep it as an “upside kicker,” not the core assumption.

Balance Sheet Relief - Finance Costs

The rights issue, operational cash flow, and debt push-down to Synthix together are shrinking Solara’s borrowings. Finance costs, which were ~₹85 crore in FY25, are expected to fall by ~200 bps in FY26 and halve over the next two years.

Source: Q4Fy25 Investor Concall Transcript

That alone can add ~₹40 - 50 crore to annual profit without changing operations.

Lower leverage also reduces risk perception, which helps valuation multiples.

Putting It Together

Catalogue APIs alone (base): ₹3,600 - 4,000 crore EV in 3 - 4 years.

CRAMS + Polymers optionality: another ~₹900 - 1,000 crore EV conservatively.

Total: ₹4,500 - 5,000 crore combined. Subtracting the net debt, Market Value comes out about 4000-4500 Crores.

Against today’s market cap (well below the current ~ 2728 Crores Market Cap), the room for rerating is visible.

Some comparison:

Investor Takeaways

For investors, Solara is now three things at once:

A Turnaround: Margins have swung from negative to 18%, debt is falling, finance costs are easing.

A Yard Play: The business still looks messy to many, but the fundamentals are cleaner than the market perception. That gap is where mispricing hides.

A Special Situation: The demerger of CRAMS and polymers into Synthix is a genuine value-unlock event - the kind of setup where 2 + 2 can become more than 4.

However, the risks are real: Vizag delays, CRAMS scaling slower than expected, or ibuprofen volatility returning. But the downside is cushioned by the reset. The upside, if even part of the optionality clicks, can be disproportionate.

Disclaimer: Zen Nivesh - No Holding, Shivam/Writer - No Holding. No Recommendation to Buy/Sell.

And if you’ve found value in our research and investment playbook, and are keen on subscribing to our upcoming Micro-cap (₹3,000 Cr market cap and below) Stock Advisory, you can join the waitlist here. Waitlist members will be the first to receive updates when we launch.

We are running a Festive Season Offer where you will get our Zen Investing Club annual Membership for only Rs. 7500 (Instead of Rs. 12000). Get a glimpse of our club here:

Use code: FESTIV

This offer is valid till October 23, 2025 only! Join Now!

| A guest post by

|

I am pharma graduate so I have a decent idea how things work and i tend to have a high allocation in pharmaceutical and healthcare sector as well for this reason i understand how things work and move

This business seems intresting enough to go for my self and check out all the things I went and researched and gave a 7% allocation in my portfolio if the quarterly results of next 2-3-4 quarters are good then I will put more on into it .... But thanks though for the well researched and well written content

And a good management with good ethics and skin in the game can turn a good struggling business around

Too good