From Darling to Discarded: A Decade of Repco

ZN Playbook-Deep Value | Where time & patience is your moat | Research Lab #23

This blog is the 4th and the last edition of our 4-part ZN Research Playbook series.

Find the 1st, 2nd, and 3rd edition here:

Kalyani Cast-Tech Ltd. - Small Box, Big Optionality

Starting this week, I’m opening up our research playbook - one style at a time. Over the next four Fridays, we’ll unpack, with case studies from our watchlist and portfolios, the four engines that will drive our Micro-cap focused (< Rs. 3000cr Market Cap) Stock Advisory very soon (Yes, we are finally launching):

NITCO: Etched In Stone Stitched In Time

This blog is the 2nd edition of our 4-part Research Playbook series.

We’ve opened up our research playbook - one style at a time.

Turnarounds / High-Convexity - improving ROE/ROCE flywheels.

Special Situations - corporate actions, mispricings, and catalysts.

High Growth / Industry Tailwinds (Yard Investing) - riding secular shifts, not headlines.

Deep Value - company trading at a discount, with patience as a moat.

In four Fridays, we’ve unpacked case studies from our watchlist and portfolios, the four engines that will drive our Micro-cap focused (< INR 3000cr Market Cap) Stock Advisory very soon (Yes, we are finally launching). Join the waitlist before you get lost in the Deep Value story of today’s INR 2,200 Cr microcap business.

What is Deep Value?

Deep Value is a style of value investing that focuses on buying stocks that are extremely cheap relative to their intrinsic worth, often because they are neglected, distressed, or operating in unpopular industries.

As investors, we can determine the cheapness based on its earnings, book value, sales, its assets, or cash flows.

The extreme cheapness of the stock itself is your trigger. You are not necessarily looking for a clear trigger or catalyst here. As the trigger or catalyst becomes clear, the cheapness will start going away. That is why you start buying in a highly uncertain environment, but your risk or downside is protected due to the extreme cheapness of the stock.

Word of caution: a very thin line separates deep value and value traps.

So, we at Zen Nivesh will never suggest that you have a portfolio of stocks entirely on this theme.

With the theme introduction out of the way, let’s get started.

For a deep dive on a deep value stock, it is fair to start with some observations on valuation.

A decade ago, Repco Home Finance used to trade at 6 times sales, 5.5 times book, and 35 times earnings.

Today, it trades at 1.3 times sales, 0.7 times book, and 5 times earnings.

The share price is down more than 50% from September 2016 to September 2025.

During the same period:

Sales have grown by a 10% CAGR. [From ₹693 crore in FY15 to ₹1716 crore in FY25]

Profits have grown by a 14% CAGR. [ From ₹125 crore to ₹461 crore]

Average ROE in the last decade has been 15%.

I am reminded of the Security Analysis book by Benjamin Graham, the father of value investing. It is not fashionable to quote Buffett, Munger, or Graham these days. Call me old-school. So, be it.

The quote by the Roman poet Horace appears at the beginning of Benjamin Graham’s book Security Analysis.

“Many shall be restored that now are fallen, and many shall fall that now are in honor”.

It illustrates the concept of regression to the mean, suggesting that the best-performing companies will eventually perform less well, and the worst-performing companies will improve over time.

I learned this concept in my teenage days, way before I joined the stock market, courtesy of my uncle (ताऊजी). He used to say this in Hindi.

सराहो मत, सराहो मत, निन्दने पड़ेंगे।

निन्दो मत, निन्दो मत, सराहने पड़ेंगे।

Translating in English if you do not understand Hindi:

Do not praise, do not praise, else you will have to criticize.

Do not criticize, do not criticize, else you will have to praise.

Repco has gone from “praise” to “criticism”

But what happened? And Why? Why praise to criticism to irrelevance?

I will have to take a short detour to make you understand this.

Have you watched the movie, 50 First Dates?

I watched it during my college days, a few years before I started investing. Little did I know then that this romantic comedy movie would help me better understand markets and industry cycles.

Fifty First Dates (2004) is a romantic comedy about Henry Roth (Adam Sandler), a marine veterinarian in Hawaii, who falls in love with Lucy Whitmore (Drew Barrymore), a woman suffering from short-term memory loss due to a car accident. Lucy forgets everything that happens each day once she goes to sleep, so Henry must make her fall in love with him again every morning.

The stock market is not very different from Drew Barrymore’s character Lucy in the movie. Just that, instead of one day, the market’s memory lasts only one cycle at a time. And as there is no Henry who will remind her in the next cycle about the previous cycle, she just picks up new boyfriends every cycle.

Ok, if you don’t watch Hollywood movies, you should picture this:

The blog is not on movies but on a microcap stock, so let’s come back to the main theme.

The learning from these movie references is very simple.

The market’s memory lasts only one cycle at a time. In every new cycle, it forgets the past winners and focuses on the new ones.

In the NBFC space, for that matter:

2013–2017: Housing finance companies were the darlings of Dalal Street.

2017-2021: Gold finance and affordable housing finance made the headlines

2021–2023: Microfinance companies were the market’s sweethearts.

2023–2025: Gold finance NBFCs have stolen the limelight again.

We can find parallels in other non-financial sectors as well, where the market favoured one and ignored the other completely. But I hope you get the larger point.

Winners of the last cycle fade into irrelevance, only to be rediscovered when the wheel turns again. Repco is one such forgotten story.

Back in 2013, IPO headlines in the Economic Times read:

“Repco Home IPO: A good bet for the long term”.

Source: Economic Times

Brokerages issued a Subscribe Call to the IPO

Source: Business Standard

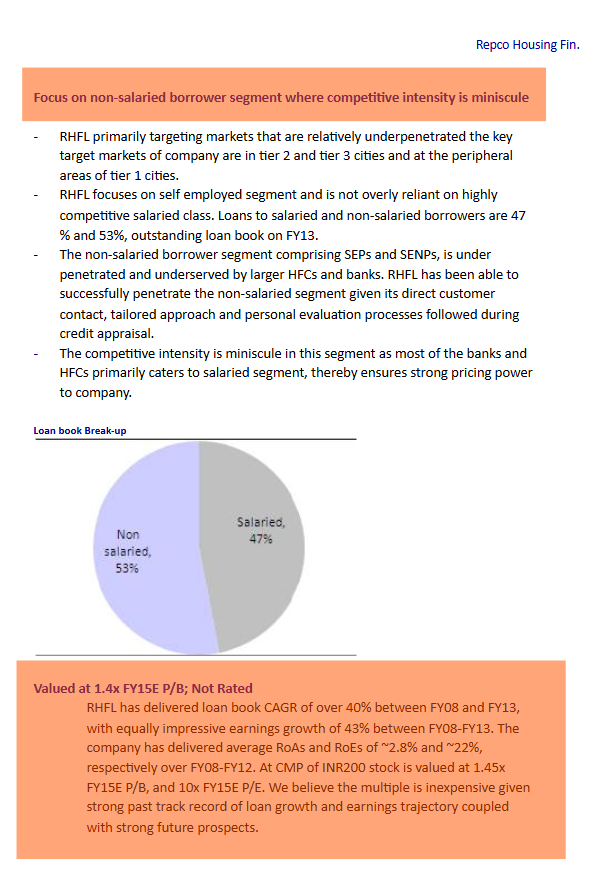

Motilal Oswal’s 2013 Report was super bullish on growth and valuation comfort.

Source: Motilal Oswal

Value Pickr Forum had a lot of senior and respected investors rooting for this stock

Source: ValuePickr

And all of them were right.

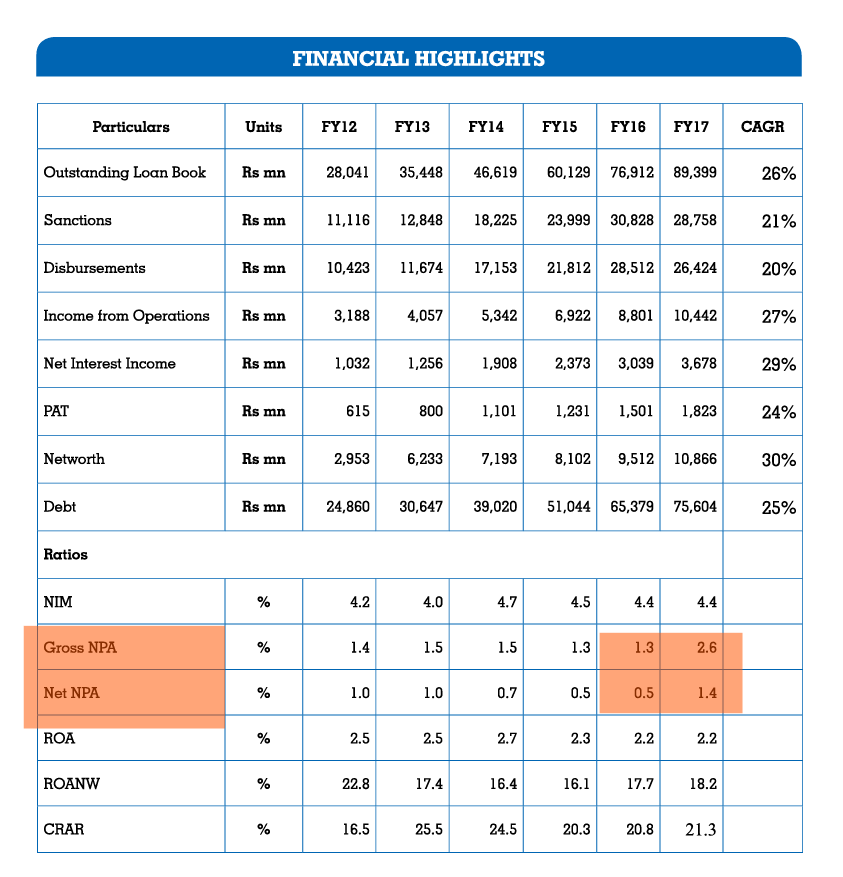

The business and the stock really did wonders in that period from 2013 to 2017.

AUM grew from ₹3545 crore to ₹8940 crore. 26% CAGR

Income from operations grew from ₹405 crore to ₹1044 crore. 27% CAGR.

PAT grew from ₹80 crore to ₹182 crore. 23%CAGR.

Stock also became a five-bagger in the same period.

From ₹172 to ₹892. 51% CAGR.

Fast forward to today, and the tone is very different. Repco barely gets a mention.

The market’s perception of Repco has moved from “darling” to “discarded.”

If there were valid reasons for Repco to do well from 2013 to 2017, there were valid reasons for it not to do well from 2017 to 2022.

This is my 3rd blog on a financial business. And for the third time, I will repeat what I have said in my previous two blogs on financial businesses.

Lending is a strange business. Unlike any other business, here, the money leaves the company when a sale is made. And that’s the easy part. The tough part is to bring it back on time and with sufficient profit.

Whenever a lending transaction takes place, one guy walks away with money, and the other walks away with a promise. A promise that the money, which has been lent, will be utilized wisely and returned with interest to the lender appropriately.

But does that always happen?

No!

That’s why we need bankers or lenders who can distinguish between the good and the bad borrower and lend wisely. And this is hard. And that is why we have very few names in India whom investors can trust for their ability to lend wisely.

Sharing the blog links below

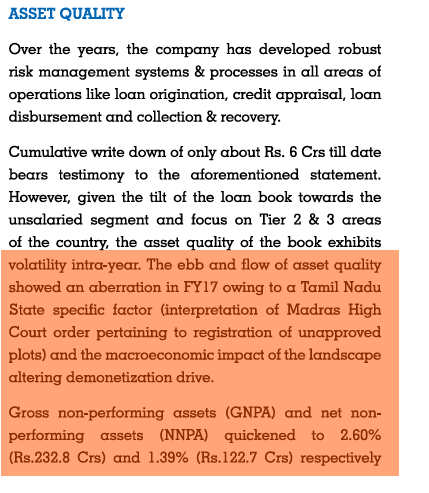

And there were cracks in the wall of Repco’s lending if you simply observed the headline numbers. You need not be a forensic expert to have figured that out.

Source: FY17 Annual Report

Source: FY17 Annual Report

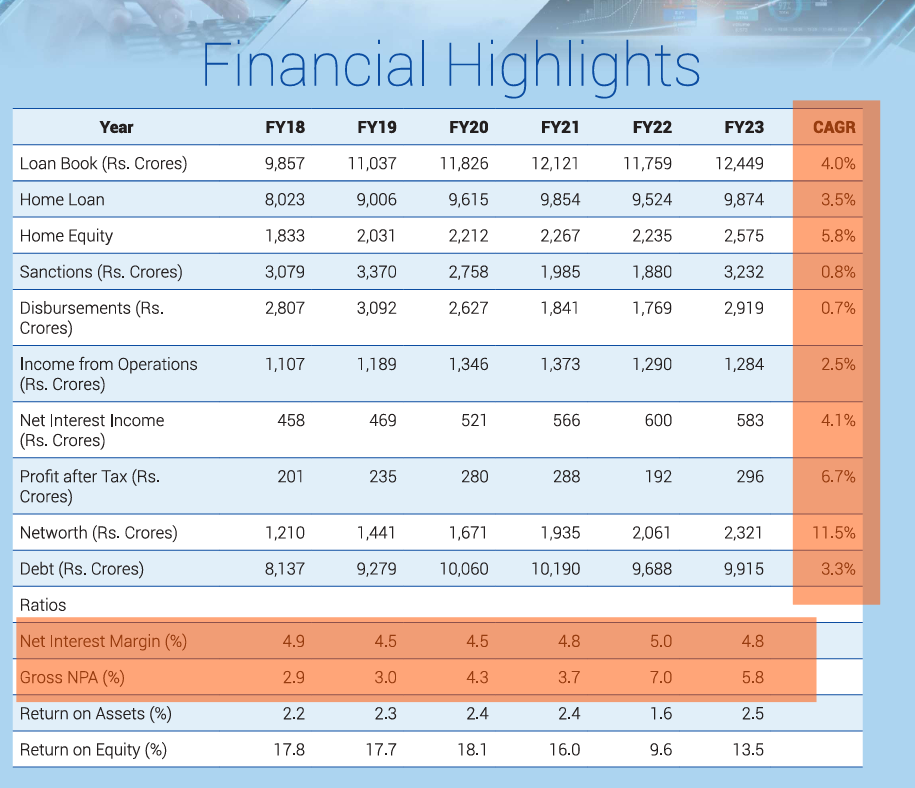

A fast-moving Mercedes hit a lorry in 2017. And could barely move for the next 5-6 years.

Source: FY23 Annual Report

I am seeing this pattern repeating in so many financial businesses:

Grow fast during an upcycle.

Ignore the importance of asset quality.

Ignore the importance of asset-liability mismatch.

When the cycle turns, you have a deep hole in your pocket.

Miss a good part of the next upcycle, repairing your house, and putting things in order.

After all, businesses are run by humans like you and me.

We are all selfish, greedy, envious, FOMO-driven humans.

Image Source: Shutterstock

But Repco was never like this if you see its humble beginning.

The Origin Story of Repco

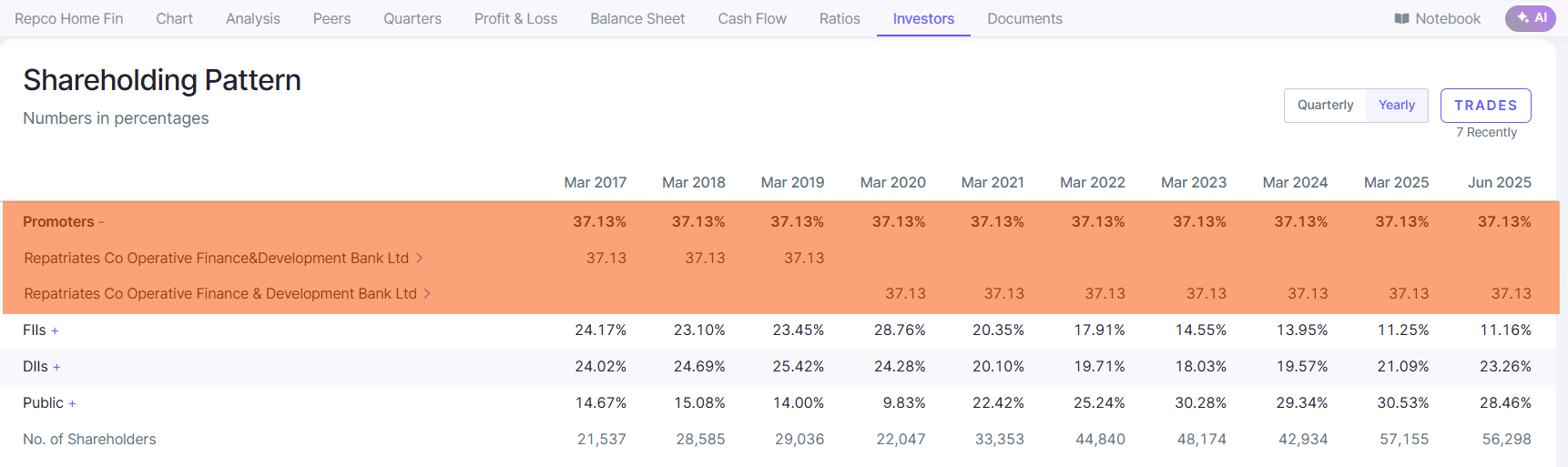

Until my wise friend brought this to my notice, I was not aware that Repco is actually a close cousin of Public Sector Unit (PSU) or Public Sector Bank (PSB).

Let me explain.

For the uninitiated, a PSU/PSB must be majority-owned by the government (at least 51% of paid-up capital).

In the case of Repco, it’s a little complicated. Let me break it down for you.

Check out the promoter shareholding:

Source: Screener

Repatriates Cooperative Finance and Development Bank Ltd. (REPCO Bank) is a private sector scheduled cooperative bank in India. It was registered in 1969, originally to serve repatriates under the Madras Cooperative Societies Act.

Its share capital is held by multiple stakeholders, including the Government of India, the Government of Tamil Nadu, the Government of Andhra Pradesh, the Government of Telangana, and others.

For instance, as of March 2025, the share capital of the bank is distributed:

GoI: ₹76.32 crore

Govt of Tamil Nadu: ₹7.13 crore

Govt of Andhra Pradesh: ₹1.05 crore

The Govt of Telangana, Kerala, Karnataka, and “Repatriates & Other A-class shareholders” make up the rest.

Thus, Repco Bank is effectively a cooperative bank with significant government shareholding (especially GoI and some state governments).

Because Repco Home Finance is promoted by Repco Bank and Repco Bank is partially government-owned, the government (GoI, Tamil Nadu) exerts indirect influence over Repco Home through its ownership stakes in Repco Bank.

Hence, a close cousin of a PSU and not a PSU.

But a natural question that should come to your mind is why a close cousin of a PSU was growing fanatically in the last upcycle between 2013 and 2017.

This leads me to another important chapter in the history of Repco Home Finance. I will call it “Depending upon the Kindness of Strangers

Depending upon “The Kindness of Strangers”

Warren Buffett coined the phrase.

Prof. Sanjay Bakshi made it popular.

If a business could do that without recourse to outside capital markets – no dilution, no need for borrowing money, there’s preferably large positive free cash flow which is sufficient to fund all growth, then there is no need to depend on outside capital markets or, as what Buffett calls it, ‘depending upon the kindness of strangers. - Prof Sanjay Bakshi

Here comes a stranger to offer help to Repco when the world was reeling under the Global Financial Crisis of 2008.

Source: Reuters, Japan

And the stranger quietly leaves after helping himself a little too

Source: VCCricle

Carlyle didn’t just help himself, but also Repco. Check the data below.

Source: Company Annual Reports, ZN Research Lab

Yuval Noah Harari has explained “growth” beautifully in his book Sapiens.

Yet to understand modern economic history, you really need to understand just a single word. The word is growth. For better or worse, in sickness and in health, the modern economy has been growing like a hormone-soused teenager. It eats up everything it can find and puts on inches faster than you can count.

If the economy is a hormone-soused teenager, I would say, with no offence or disrespect, VC or PE guys are 100 such teenagers put together. No judgment. Just an observation. Turbo-charged high-growth in a short period of time is their DNA.

While you definitely get growth. Often it comes at a price.

2000: Repco Home Finance is formed

2008: Carlyle invests in Repco

2013: Repco got listed on the stock market with a strong track record of growth.

2014: Carlyle exits

At that time, both Repco and Repco’s public market investors had seen a great 7-8 years of stupendous growth. While the gross NPA and net NPA started rising quietly, it was not that alarming.

That’s the power of impatient capital sitting on high growth. A humble housing finance business, a close cousin of PSU, gets into a high-growth-chasing bandwagon and forgets its main task of credit discipline and asset quality. Rest is history.

This brings me to an often-ignored lesson in lending business.

Power of Patient Capital

HDFC Ltd

HDFC Bank

Bajaj Finance

Shriram Finance

L&T Finance

Sunderam Finance

Apart from being great lending institutions, the above lenders had the blessings of patient capital. To further persuade you, let me quote a personality you would agree with.

I have watched this video multiple times. I think it is a masterclass to understand the lending landscape.

If you don’t have time, you can watch the video from here for just 5 minutes.

The 18th minute to the 23rd minute.

Where Mr. Aseem Dhru talks about the importance of patient capital. He also explains why he avoided PE/VC money when he was starting SBFC.

So, the learning for me is that when impatient capital chases high growth with a short-term mindset, it has a lot of side effects. And owners and investors both are so addicted to the short-term high growth that they fail to see the other side of the story.

Ok. I have covered a lot of ground. And I have let my mind wander freely back and forth. :)

Before we come to the climax of this movie, let me just summarize the different chapters once for your convenience and clarity.

First, we covered the listing of Repco and the consensus bullishness around it.

Second, we covered the tremendous growth between FY13 and FY17

Third, we covered the fall from grace in the period FY17-FY22.

Fourth, we went back in time to understand the humble beginning of Repco.

Fifth, we saw the impact of Carlyle’s investment in Repco

Every Magic Trick Has Three Parts or Acts

Every great magic trick consists of three parts or acts. The first part is called “The Pledge”. The magician shows you something ordinary: a deck of cards, a bird or a man. He shows you this object. Perhaps he asks you to inspect it to see if it is indeed real, unaltered, normal. But of course... it probably isn’t. The second act is called “The Turn”. The magician takes the ordinary something and makes it do something extraordinary. Now you’re looking for the secret... but you won’t find it, because of course you’re not really looking. You don’t really want to know. You want to be fooled. But you wouldn’t clap yet. Because making something disappear isn’t enough; you have to bring it back. That’s why every magic trick has a third act, the hardest part, the part we call “The Prestige”.

Making Repco disappear or lose its relevance is not enough. If I have to really impress you, I will have to bring it back.

Here comes the third Act, the hardest part, the part we can call “The Prestige”

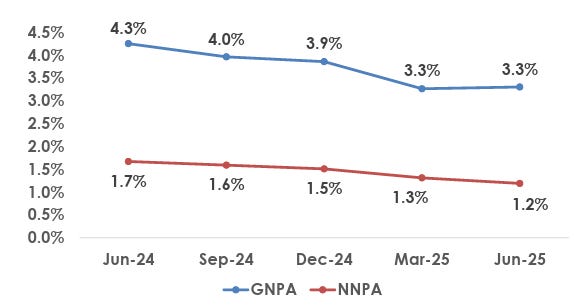

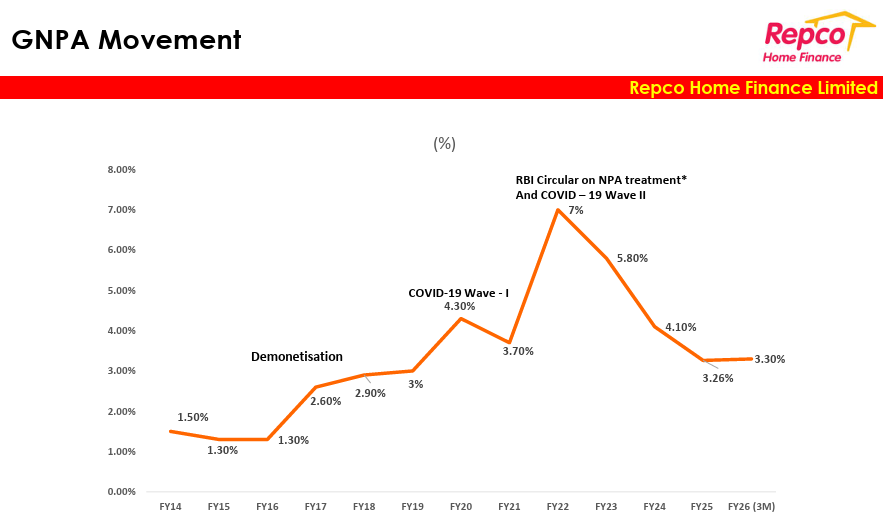

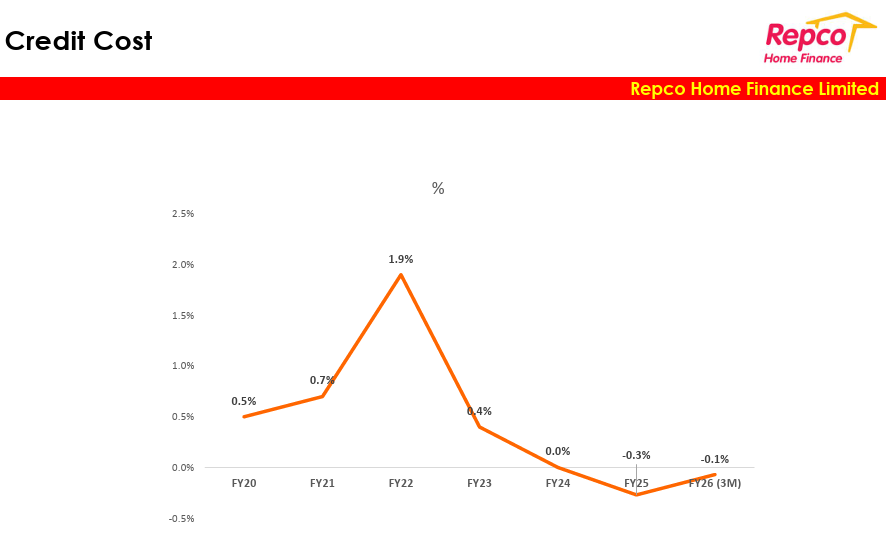

At the fag end of FY22, when all hell broke loose, and NPAs were at their peak for Repco, Mr. K. Swaminathan joined Repco as a heart surgeon to operate on a critical patient in an emergency.

A few critical operating procedures followed by him:

Improved collection efficiency and brought down NPAs under control

Focused on reducing Balance Transfer Out.

Verticalization: Disbursement and collection were separated as two different units with no overlap of resources. This brought discipline and accountability to both departments.

Decentralization: Empowering the feet on the ground.

While I would have liked Mr. K Swaminathan to stay longer, he resigned in FY25. A new management has taken over.

I know that pictures are worth a thousand words. So I will let them do the talking for the surgery done by Swaminathan and the recovery of Repco.

These are all from their Q1FY26 presentation.

While the management has been notorious for not being able to meet their guidance or projections in the past, a few forward-looking statements were made by the new management at the end of FY25.

FY26 Guidance:

AUM target: Rs. 16,200 cr (12% growth).

Disbursement target: Rs. 4,000 cr.

Maintain spread at ~3.2% and ROA at ~3.1%.

GNPA <2.5%, NNPA <1%, Stage-2 assets at 7–8% of book.

Cost-to-income to improve by 60–70bps.

Add 14 new branches; upgrade 12 satellite centers to branches.

Medium-term (FY28) Vision

AUM of Rs. 25,000 cr, driven by “accelerated disbursements and growth with quality and profitability.

Dividend Policy

Investor request for higher payout acknowledged; Board has increased payout ratio, will consider further based on investor sentiment.

Let’s not be too overoptimistic on the recovery, and also spend a considerable time on the risk side as well.

Risks in Repco’s Recovery

Geographical concentration. In the past, Tamil Nadu-centric issues created a big problem for the company. That risk is still there.

Relatively higher exposure to certain riskier borrower segments: The low-income self-employed category is inherently risky and demands credit prudence.

Changes in laws and regulations applicable to HFCs can create problems.

Inability to expand business to new regions and markets.

Inability to compete effectively: The new housing finance companies are more efficient and tech-savvy. They are way better than Repco on almost all counts. Period.

Frequent management and board changes: This MoneyLife article will scare you.

Closing Thoughts

There is no doubt that out of all the listed pure-play housing finance companies, Repco would probably rank last or second last.

But at 6 times earnings, 0.7 times book, and 1.3 times sales, the consensus is telling us that it is a worthless company. Disgraceful.

I don’t think Repco is a great company. But I don’t think it is worthless. And I definitely don’t think it is disgraceful.

Here’s a snippet from a 2015 blog.

Source: Jana Vembunarayanan Blog

I am not trying to criticize the blogger here. And to be fair with him, he has rightfully acknowledged the possibility of negative black swans, and he did not buy the stock. When Jana used to write, I used to read all his blogs and learned a great deal. Loads of respect for him. Thanks, Jana. I wish you would start writing again.

My point is very simple.

In 2015, investors were extrapolating a very high past growth rate far into the future.

In 2025, investors are extrapolating a very low past growth rate far into the future.

Time will tell if they are making the same mistake of 2015 in 2025.

सराहो मत, सराहो मत, निन्दने पड़ेंगे।

निन्दो मत, निन्दो मत, सराहने पड़ेंगे।

Translation:

Do not praise, do not praise, else you will have to criticize.

Do not criticize, do not criticize, else you will have to praise.

Thanks for reading.

The blog you just read was meant to give you a glimpse into how we think and write about businesses. Over the last few months, we’ve been tracking microcaps that fit our framework and playbook.

While not every idea works out this way, the real value lies in the process behind the thesis - disciplined, research-driven, and focused on long-term compounding.

👉 Want access to more of this research?

We’re opening the Zen Nivesh Stock Advisory shortly. Join the waitlist to receive the brochure (delivered in 10 days) and a sample report of a microcap business. Also, get the first access when we onboard our inaugural batch.

Disclaimer: This is research, not investment advice. Strictly consider for educational purposes only. Do your own diligence; markets carry risk.

| A guest post by

|

Your article was exceptionally well-written and highly engaging. You guys are doing a very hard work for engaging a common person to read. I didn’t feel like I was simply reading a stock analysis, but rather as if I were watching a story unfold, wondering what might happen next and reflecting on the company’s past journey. Truly a captivating way to present insights.

Great blog; agree best time to buy stock is when it is disgraced by street